Archived information

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Audit of Materiel Management: Optimizing Valuable Resources

Final Report

Foreign Affairs and International Trade Canada

Office of the Chief Audit Executive

July 28, 2011

Table of Contents

- Executive Summary

- 1. Background

- 2. Observations and Recommendations

- 2.1 Clarify the current governance structure to appropriately direct Materiel Management within the Department.

- 2.2 Improve planning to enable the Department to rationalize its actual spending on materiel and capitalize on opportunities for cost savings and cost avoidance across the life-cycle of materiel management.

- 2.3 Improve recording and reporting of materiel.

- 2.4 Strengthen materiel management policies and procedures to provide comprehensive guidance to the Department.

- 3. Conclusion

- Appendix A: About the Audit

- Appendix B: Management Action Plan

- Appendix C: Figures

Executive Summary

In accordance with its approved Risk-Based Audit Plan for 2010-2011, the Office of the Chief Audit Executive conducted an internal audit of Materiel Management at the Department of Foreign Affairs and International Trade (DFAIT).

Why is this important?

Materiel management is a critical aspect of DFAIT’s ability to carry out its mandate effectively. DFAIT operates on both the domestic and international fronts with over 170 Missions in 105 foreign countries. DFAIT supports the presence of its own employees as well as Canadian-Based Staff from other departments and jurisdictions. In 2009, the Department provided and maintained furnished accommodation in 1,795 staff quarters, 107 Official Residences and 230 Chancery Complexes. DFAIT also owns and operates a fleet of approximately 800 motor vehicles. Over $50 million in materiel is acquired by the Department annually.

The Department is accountable for the sound stewardship of the materiel entrusted to it. The expectation is that materiel will be managed by departments in a sustainable and financially responsible manner that supports the cost-effective and efficient delivery of government programs.

The global reach of the Department, the requirement to fulfill program objectives in a sustainable and financially responsible manner and the wide variety of demands for materiel to ensure that the operational and administrative needs of its staff and stakeholders are satisfied, underscores the importance of materiel management in DFAIT.

What did we examine?

The objective of this audit was to assess the adequacy of DFAIT’s materiel management framework in supporting effective and efficient operations. It addressed the fundamental question of whether DFAIT was positioned to demonstrate sound stewardship of its assets and to optimize the value of materiel.

The audit team examined the following key aspects:

- Authority and Accountability

- Life-cycle Management of Materiel

- Financial and Non-financial Information to support decision-making

- Policies and Procedures

What did we find?

Materiel Management at DFAIT is facing challenges which are made more pressing as the Department moves to become more financially sustainable.

More specifically, the audit found that to become more effective and efficient the Department should:

- Clarify the current governance structure to appropriately direct materiel management within the department.

The audit team found the dispersion of authorities and responsibilities for materiel management blurred the ability of the Chief Financial Officer to exercise his accountabilities, weakened opportunities to provide functional authority and lead to inconsistent and at times non-compliant practices.

- Improve planning to enable the Department to rationalize its actual spending on materiel and capitalize on opportunities for cost savings and cost avoidance across the life-cycle of materiel management.

The Department is unable to conduct adequate planning because information related to existence, location and condition of materiel is incomplete, inadequate and inconsistent. Departmental materiel management planning cannot be based on knowledge of existing holdings and their condition which is necessary to forecast future requirements for acquisitions, maintenance/repair and disposal. There isn’t a consistent approach to planning across the organization resulting in a lack of correlation between materiel management requirements and the budget in both the short and long term.

- Improve recording and reporting of materiel.

There is no single materiel management information system used in the Department to collect and generate complete and accurate data on materiel. Policies, directives and guidelines to support sound management of materiel are not sufficient and/or enforced. As a consequence, accurate corporate materiel inventory is not available.

Recognizing that this situation is not acceptable, the Materiel Management Renewal Project is currently underway. This project is designed to provide the technical platform to record the Department’s materiel. The implementation of this system is planned for early 2012. It is uncertain at this time, however, when this new system will provide assurance that DFAIT materiel is recorded and reported accurately.

Recording inventory of materiel is no small feat. A key decision for senior management will be whether to undertake a resource intensive exercise upon system readiness to ensure accurate inventory at the first possible opportunity versus an incremental approach to building inventory as new materiel is acquired.

The auditors noted some positive aspects of materiel management including:

- Fair and competitive acquisition processes using appropriate contracting mechanisms;

- Sound control over the inventory of vehicles, artwork and heritage items;

- Comprehensive guidance provided to Missions through a Materiel Management manual.

Key Recommendations

- The Department should strengthen its control framework for materiel management by clarifying authorities, roles, responsibilities and accountabilities.

- There should be clear requirements for materiel management planning in Headquarters and Missions, supported by standard processes, procedures, tools and clear communications. Alongside with planning, the Department should also capitalize on opportunities for savings identified in the audit.

- Senior management should ensure that recording and reporting of materiel is improved through the implementation and effective use of the technology solution of the Materiel Management Renewal Project. At the same time the Department should provide clearer policy and guidance.

Conclusion

Overall, the Department’s materiel management framework has weaknesses that require senior management attention to permit DFAIT to realize the full potential benefit from its materiel investments.

Statement of Assurance

In my professional judgment as Chief Audit Executive, sufficient and appropriate audit procedures have been conducted and evidence gathered to support a high level of assurance on the accuracy of the information in this report. The results are based on a comparison of the conditions, as they existed at the time, against pre-established audit criteria that were agreed upon with management. The results are applicable only to the processes examined. The evidence was gathered in compliance with Treasury Board Policy, Directives, and Standards on internal audit for the Government of Canada.

Original Signed by:

Yves Vaillancourt

Chief Audit Executive

1. Background

In accordance with its approved Risk-Based Audit Plan for 2010-2011, the Office of the Chief Audit Executive conducted an audit of Materiel Management at Headquarters and at Missions. This audit's field work was carried out from October 2010 to January 2011 and included on-site visits to three Missions as well as document review from an additional nine Missions.

The audit's objective was to assess the adequacy of DFAIT’s materiel management framework in supporting effective and efficient operations. This audit addressed key aspects of the materiel management control framework, including:

- Authority and Accountability;

- Life-cycle Management;

- Financial and Non-financial Information; and

- Policies and Procedures.

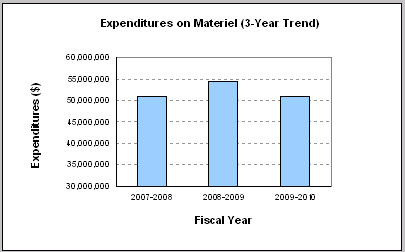

Materiel management is a critical aspect of DFAIT’s ability to carry out its mandate effectively. DFAIT operates on both the domestic and international fronts with over 170 Missions in 105 foreign countries. DFAIT supports the presence of its own employees as well as Canada-Based Staff from approximately thirty departments, agencies and jurisdictions. In 2009, the Department provided and maintained furnished accommodation in 1,795 staff quarters, 107 Official Residences and 230 Chancery Complexes. DFAIT also owns and operates a fleet of approximately 800 motor vehicles. In recent years, the Department has spent over $50 million annually in the acquisition of materiel and commodities, as noted in the figure below.

Figure 1: Materiel Expenditures FY 07/08 to FY 09/10

Figure 1 Text Alternative

| 2007-2008 | 2008-2009 | 2009-2010 |

|---|---|---|

| $51,109,197 | $54,514,993 | $50,893,693 |

The Department is accountable for the sound stewardship of the assets entrusted to it – promoting due diligence, ethical behaviour and sound management practices, thereby ensuring long-term sustainability and value for Canadian taxpayers. The wide variety of demands for materiel to ensure that the operational and administrative needs of staff and stakeholders are satisfied, underscores the importance of materiel management in DFAIT.

The Treasury Board Policy on the Management of Materiel defines materiel as “All moveable assets, excluding money and records, acquired by her Majesty in right of Canada”. The word materiel is used in this audit to enhance reader understanding that the scope of this audit is broad and includes more than items classified as capital assets.

The Treasury Board Guide to Management of Materiel defines materiel management as “all activities necessary to acquire, hold, use, and dispose of materiel, including the notion of achieving the greatest possible efficiency throughout the life cycle of materiel assets.”

In recent years, the Department has spent over $50 million annually in the acquisition of materiel and commodities, as noted in Figure 1.

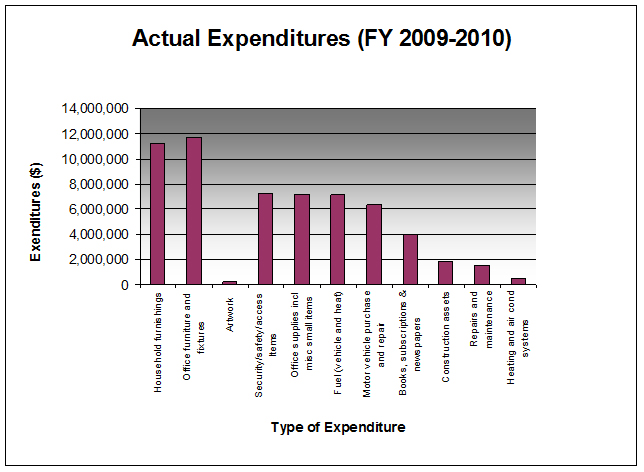

The main types of materiel acquired by DFAIT include office and household furniture, office supplies, security-related goods and vehicles. In FY 09/10 these purchases were broken down as shown in Figure 4.

The phases of life cycle management include: assessment and planning; acquisition; operating and maintenance; and, disposal.

2. Observations and Recommendations

2.1 Clarify the current governance structure to appropriately direct Materiel Management within the Department.

Materiel management authorities are not aligned with accountabilities.

The audit team expected to find functional authority for materiel management in the Department to be clearly assigned and exercised through the development and communication of policies, procedures, directives and guidelines. It was also expected that the functional authority would exercise control, oversight and reporting of materiel management activities including accurate and complete financial information.

The Department’s Materiel Management Manual for Missions states that the Assistant Deputy Minister (ADM) Corporate Services (the current ADM Corporate Finance and Operations) has departmental responsibility for materiel management. While the Manual is clear on the allocation of overall responsibility, it also identifies “delegated responsibility centres that develop policies and provide materiel services to Missions and Headquarters”.

Although the ADM Corporate Finance and Operations (otherwise referred to as the Chief Financial Officer) has been assigned overall responsibility for materiel management, in practice, many divisions in three separate Branches, along with each Mission exercise specific roles and responsibilities with respect to the acquisition, allocation, control, reporting and disposal of materiel. These roles and responsibilities are not aligned with accountability. The degree to which the Chief Financial Officer exercises functional authority (direction and oversight) over all of the participants and stakeholders in the management of materiel appears to be limited.

The materiel management function operates in a de-facto decentralized model and has established centres of expertise across the Department to provide materiel management services. As a consequence, materiel management authority is presently split among the Chief Financial Officer, the Assistant Deputy Minister of the International Platform Branch, the Assistant Deputy Minister of the Consular Services and Emergency Management Branch and Heads of Missions. These different groups operate with substantial autonomy.

Unlike the other centres of expertise, the Corporate Operations Bureau under the Chief Financial Officer has functional authority as well as transactional duties related to materiel management at Headquarters. The current delivery model for materiel management does not support the exercise of appropriate functional authority. Responsibilities for materiel management are shared between multiple centres of expertise and Missions. For many types of materiel (vehicles as an example) there are multiple groups responsible which could weaken accountability.

Under this delivery structure and given the degree of autonomy of the units involved, the audit team found that the Corporate Operations Bureau under the Chief Financial Officer (CFO) is not well positioned to carry out its responsibilities. The CFO cannot fully exercise his accountability in situations where sub-delegated authorities operate independently and without clear strategic direction and reporting relationships.

This structure poses risks related to effectiveness, efficiency and compliance. Without a strong accountability structure, fully enforced, there is a risk that materiel will not be managed properly and that the Department will not have the right information for decision making.

In addition, opportunities for economies of scale are reduced and there is a potential for duplication of effort among the various service delivery points.

Recommendation:

- In the same manner as was recommended in the 2010 Audit of the Delivery of Corporate Services in Headquarters, the Department should:

- Confirm to whom the authority for materiel management is delegated and ensure it is aligned with the accountability for same and clearly communicated throughout the organization;

- Mandate the delegated authority to review and strengthen the control framework over the management of materiel; and

- Clearly communicate roles and responsibilities of all parties involved in materiel management.

2.2 Improve planning to enable the Department to rationalize its actual spending on materiel and capitalize on opportunities for cost savings and cost avoidance across the life-cycle of materiel management.

Planning for the acquisition, maintenance/repair and disposal of the Department’s materiel is not generally undertaken in a manner that permits the Department to fully realize the current and future demands for materiel and to take advantage of economies of scale at Headquarters and abroad.

Effective materiel management would include life-cycle planning that is based on knowledge of existing materiel holdings and their condition along with a forecast of future requirements for acquisitions, maintenance/repair and disposal. Materiel management plans should reflect departmental objectives and priorities. Ideally, the implementation of materiel management plans should be subject to cost-benefit analyses.

A good plan would be integrated into the budget and include activities, schedules, and resources needed to meet planned materiel management actions. The Department is unable to conduct adequate planning because information related to existence, location and condition of materiel is incomplete, inadequate and inconsistent. Departmental materiel management planning cannot be based on knowledge of existing holdings and their condition which is necessary to forecast future requirements for acquisitions, maintenance/repair and disposal. There isn’t a consistent approach to planning across the organization. This results in a lack of correlation between materiel requirements and the budget, the absence of a complete understanding of the short and long term needs of the Department for materiel.

Planning for life-cycle replacement of materiel in Headquarters generally does not take place while planning efforts in missions are inconsistent. In a sample of twelve Missions included in the audit, three had detailed materiel planning for the cyclical maintenance and replacement of furniture and appliances; other Missions had no materiel management plans at all.

The audit team noted that there is a plan in place for the cyclical refurbishment of Official Residences and Chanceries. Occasions were identified, however, where sufficient communication did not take place within the Department to avoid the refurbishment of properties which were subsequently sold.

The auditors noted the following positive planning efforts:

- The planning for the materiel associated with the new Emergency Watch and Response Centre was initiated early in the project and tracked in significant detail;

- The International Platform Branch assessed future materiel requirements at Missions and negotiated discounted prices for bulk purchases, making inventory available to Missions on the electronic shopping website: Shop@DFAIT;

- Planning was undertaken for the cyclical replacement of the executive fleet;

- Planning for security equipment starts years early involving other stakeholders, including the Property Strategy Section for new buildings; and

- Regional Security staff plan for security equipment at Missions.

As a consequence of weaknesses in planning, the Department fails to fully appreciate the current and future demands for materiel and to take advantage of economies of scale at Headquarters and abroad. Further, DFAIT lacks a prioritized set of materiel needs that would enable the Department to allocate funding to acquisitions that most directly support the delivery of the Department’s programs and activities. The absence of a standard, consistent, systematic means of documenting the planning for materiel in Missions results in an onerous exercise when good planning tools are not available.

Considering the Department spends on average more than $50 million per year on materiel, planning is critical to document the rationale for such spending.

Recommendations:

- It is recommended that the Chief Financial Officer articulate clear requirements for materiel management planning in HQ and Missions, supported by standard processes, procedures and tools, as appropriate.

- It is recommended that, the Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch ensure that within the Department, short and long-term acquisition, refurbishment and disposal project plans be clearly identified and communicated to all affected parties.

The process by which materiel is acquired is generally fair and competitive.

A strong acquisition process would be expected to enhance access, competition, and fairness, resulting in the optimal balance of cost (including transportation), quality, timeliness, and environmental benefits.

Goods at Missions and at Headquarters are acquired using standing offers where practical. This includes large purchases such as automobiles for the Executive Fleet and furniture groupings for Staff Quarters at Missions. Smaller purchases at Missions are generally obtained using an informal competitive process in the local market.

Sole sourcing is used when necessary to obtain items that are only offered by one supplier or when the requirement includes compatibility with other government departments.

The audit team also reviewed the acquisition process for Canadian artwork and found it well managed. A selection process using a committee has been implemented to make the determination of which Canadian artists’ works will be promoted by adding them to the Department’s collection.

Fleet vehicle acquisitions at Missions need effective oversight from Headquarters.

The financial threshold for sole source justification is $25,000. However, from a review of Missions’ acquisition files, several vehicles, over $25,000 each, were acquired by sole source. Also, four vehicle purchases reviewed exceeded the Materiel Authorization Table guidelines. The policy at this time is that only Head of Mission vehicle purchases receive Headquarters scrutiny.

Recommendation:

- It is recommended that the Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch identify and implement effective ways and means of providing oversight to vehicle acquisitions in Missions, and consider the benefits of a central fleet management process for missions.

Disposal of Assets can be undertaken more strategically and efficiently.

The Treasury Board Policy on Management of Materiel requires that departments ensure that: "The disposal of surplus materiel assets is concluded as effectively as possible, as soon as possible after they become surplus to the requirements of program delivery, in a manner that obtains highest net value for the Crown, and in compliance with the Treasury Board Directive on Disposal of Surplus Materiel”. Materiel can be disposed by being sold, donated or scrapped.

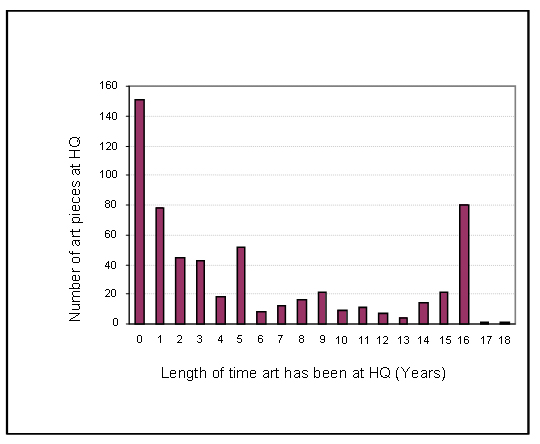

Using data provided by the Visual Art Collection, it was determined that 441 or approximately 7.7% of the 5764 pieces in the art collection have been sitting idle at Headquarters, awaiting assignment, for at least 1 year and up to 18 years.

Figure 2: Artwork at Headquarters and Available for Assignment

Figure 2 Text Alternative

| Length of time art has been at HQ (years) | Number of art pieces at HQ |

|---|---|

| 0 | 151 |

| 1 | 78 |

| 2 | 45 |

| 3 | 43 |

| 4 | 18 |

| 5 | 52 |

| 6 | 8 |

| 7 | 12 |

| 8 | 16 |

| 9 | 21 |

| 10 | 9 |

| 11 | 11 |

| 12 | 7 |

| 13 | 4 |

| 14 | 14 |

| 15 | 21 |

| 16 | 80 |

| 17 | 1 |

| 18 | 1 |

The audit team was advised that some low valued artwork pieces are being warehoused at Headquarters as they are no longer considered appropriate for circulation.

Prior to the summer of 2009, Missions received 90 percent of disposal proceeds with 10 percent of the revenue from the disposal of materiel remaining at Headquarters. During FY 2009-2010 the rules changed. Headquarters indicated that this made the disposal process more transparent, provided more oversight and allowed Headquarters to redistributes the disposal generated funds to the Mission network based on current needs and pressures. Based on this change of policy, Missions submit their net proceeds of disposal sales and do not receive back 90 percent of the revenue they generated. In two missions, staff indicated that the fact that there is no revenue going directly back to the Missions that generated it, results in a disincentive to management to pay attention to disposals. These Missions perceive that disposing of materiel carries a cost and effort that is not to their benefit. As a result, there may be increased risk of surplus materiel being “scrapped” instead of being disposed of for value or not being recorded correctly as a sale.

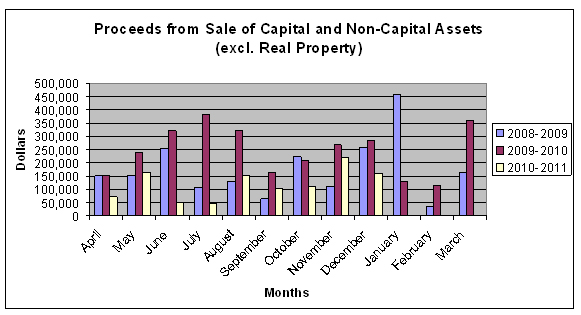

As shown in the graph below, the Financial Management Support Unit, Physical Resources, completed an analysis showing that in FY 2010-2011, the Department collected $1,078,124 to December 31st which was about half the proceeds earned at the end of December during FY 2009-2010 ($2,344,393).

Figure 3: Proceeds from Disposals of Three Fiscal Years

Figure 3 Text Alternative

| Month | Year | Dollars |

|---|---|---|

| April | 2008-2009 | $150,534 |

| 2009-2010 | $152,484 | |

| 2010-2011 | $71,237 | |

| May | 2008-2009 | $153,594 |

| 2009-2010 | $238,655 | |

| 2010-2011 | $162,786 | |

| June | 2008-2009 | $254,098 |

| 2009-2010 | $321,297 | |

| 2010-2011 | $49,742 | |

| July | 2008-2009 | $107,914 |

| 2009-2010 | $384,143 | |

| 2010-2011 | $47,416 | |

| August | 2008-2009 | $128,071 |

| 2009-2010 | $322,820 | |

| 2010-2011 | $153,058 | |

| September | 2008-2009 | $63,490 |

| 2009-2010 | $162,914 | |

| 2010-2011 | $102,198 | |

| October | 2008-2009 | $221,781 |

| 2009-2010 | $209,548 | |

| 2010-2011 | $112,770 | |

| November | 2008-2009 | $110,168 |

| 2009-2010 | $267,375 | |

| 2010-2011 | $220,115 | |

| December | 2008-2009 | $259,880 |

| 2009-2010 | $285,157 | |

| 2010-2011 | $158,802 | |

| January | 2008-2009 | $457,891 |

| 2009-2010 | $129,352 | |

| 2010-2011 | $0 | |

| February | 2008-2009 | $37,103 |

| 2009-2010 | $113,297 | |

| 2010-2011 | $0 | |

| March | 2008-2009 | $162,342 |

| 2009-2010 | $360,722 | |

| 2010-2011 | $0 |

While there may be other factors contributing to the sharp decline in revenue there appears to be a correlation between the rule change and the revenue generated from disposals. Possible reasons could be:

- Missions are being more discriminate and disposing of less because there is no monetary incentive to sell items, resulting in items being kept at the Mission for more of their useful life; or

- Missions are disposing of items but recording a greater number as scrap with no proceeds.

Compounding the issue noted above, the lack of inventory listings and controls, addressed later in the report, increases the risk of materiel identified for disposal being stolen.

A new website, called Mission eXchange, has been created by the International Platform Branch in order to facilitate the transfer of surplus assets between Missions. This initiative is intended for use by Management Consular Officers for the purpose of listing surplus goods for reuse by other Missions. Shipping costs, especially to neighbouring countries, are often much less than the cost of new goods being purchased and shipped from Ottawa.

The audit team was informed of the intention to link Mission eXchange to the Shop@DFAIT website, bringing new and previously-owned items together to assist Management Consular Officers in their acquisition processes. The Mission eXchange website, while focused on delivering services to Missions, has the potential to provide similar services to HQ organizations.

Recommendation:

- It is recommended that the Assistant Deputy Minister, International Platform Branch:

- Develop a process to dispose of artwork that is no longer required for Departmental operations and establish a trigger for the disposal of works of art such as a certain number of years in continuous storage (implying undesirability) or a minimum appraised value (implying a work so valuable they require special conservation expertise);

- Consider ways and means to ensure the Department realizes maximum revenue from the disposal of surplus materiel at Missions; and

- Expand the application of Mission eXchange services to address acquisition and disposal actions in Headquarters.

The Department’s vehicle fleet could be reduced.

DFAIT has a substantial investment in a fleet of approximately 800 vehicles. The Department should ensure that they are employed for their intended purpose and used to their full potential.

Senior management has recognized that there is an opportunity for savings in this area. The recent Vehicle Fleet Rationalization/Optimization – Savings Initiative has completed an analysis of fleet size and has identified 72 Missions where vehicles could be reduced from the Departmental fleet. The Initiative has identified potential savings of approximately $1.5 million in the first year if the report recommendations are implemented and $1.05 million in year two and ongoing.

The audit team observed that the Department operates vehicles with very low kilometre annual usage both in Headquarters and in Missions. In Headquarters it was observed that there were four spare vehicles plus two vehicles waiting disposal. Staff responsible for the Executive Fleet indicated that two spare vehicles would be sufficient to meet the Headquarters requirement.

The maintenance of vehicles could be improved

In Missions, various staff including property managers and drivers are delegated the responsibility for vehicle maintenance. In one Mission, there was no clear assigned responsibility for vehicle maintenance. As a result no maintenance was performed on a vehicle for a period of more than one year, likely shortening the life expectancy of the asset.

At Headquarters, the Department is using the services of a private fleet management company to manage the Executive Fleet. The monthly management fees are less than one hundred dollars for a fleet of approximately ten vehicles. This is significantly less than the estimated salary cost that would otherwise be required to perform these management functions. The Operational Fleet at Headquarters is not using a comprehensive fleet management service.

Recommendations:

- It is recommended that the Assistant Deputy Minister, International Platform Branch and the Chief Financial Officer consider the benefits of a comprehensive fleet management service for the Headquarters Operational fleet and its potential application to some Missions.

- It is recommended that the Assistant Deputy Minister, International Platform Branch and the Chief Financial Officer adjust the size of the Department’s fleet taking into consideration the recommendations of the Vehicle Fleet Rationalization / Optimization – Savings Initiative.

There may be potential for the Department to realize savings in the warehousing functions at Headquarters and Missions.

DFAIT uses commercial warehouses and space at Headquarters to receive and hold new and reusable materiel, and to store and group materiel for shipment to Missions. Approximately fifteen Missions also have warehouses - either Crown owned or rented. Other Missions use storage areas in garages, Chanceries and Official Residences.

There are three commercial warehouses at Headquarters used for goods within the scope of this audit as well as warehouse space for IT equipment.

- The International Platform Branch warehouse is used to store Mission furniture and furnishings and used by the Design group to hold heritage furniture and valued assets used to furnish Chanceries and Official Residences.

- The Consular Services and Emergency Management Branch rents warehouse space to store security equipment for Missions (90%) and Headquarters (10%).

- The Corporate Operations Bureau of the Corporate Finance and Operations Branch uses commercial space as well as garage space at Headquarters to store new and reusable materiel for the National Capital Region.

It has been suggested by the Centres of Expertise that there is the potential for savings by consolidating Headquarters warehousing in one location to realize efficiencies not only in storage costs but also through improved communication between Branches related to shipments to Missions. Standard container loads can greatly reduce shipping costs compared to crating and shipping small loads by air or sea.

Recommendations:

- It is recommended that the Chief Financial Officer ensure that a means is put in place to track Warehouse expenses, to allow management to clearly identify the cost of storing and crating Departmental materiel at Headquarters and Missions in order to improve the management of warehousing.

- The Chief Financial Officer, the Assistant Deputy Minister International Platform Branch and the Assistant Deputy Minister Consular Services and Emergency Management Branch should initiate a study to assess the cost-benefits of consolidating the Department’s warehouses in the National Capital Region.

2.3 Improve recording and reporting of materiel.

The Department does not have reliable information for materiel management decision making

The audit team learned from the outset of the audit that there is no single materiel management information system used in the Department to collect and generate complete and accurate data on materiel. In fact, the business problems that led to the creation of a Materiel Management Renewal Project were:

- The majority of Missions were not using the Materiel Management Module of the Department’s Integrated Management System;

- A multitude of processes, systems, spreadsheets and black books were used; and

- Accurate corporate inventory information was not available.

The audit team also observed that Missions operate stand-alone inventory recording systems – ranging from commercial inventory applications to MS-Excel spreadsheets and MS-Access databases. In some cases Missions had introduced bar-coding for some materiel. The audit team found stand-alone systems often to be:

- Unsupported;

- Subject to failure upon the departure of the key Mission staff who developed or implemented them;

- Subject to the breakdown of system components;

- Lacking consistent information elements;

- Difficult to contribute to Department-wide roll-ups;

- Lacking the same level of safeguarding as is available in the Department’s central financial system (IMS); and

- At an increased risk of loss of data, loss of hardware, corruption of software or use by unauthorized persons.

In the majority of Missions sampled, testing and interviews indicated that inventory of materiel was either not available or not updated.

However, it was noted that inventory information, held at Headquarters, is available for some valuable assets, such as fine art, heritage items and vehicles. In all Missions visited, the audit team was able to confirm existence of a sample of fine art pieces selected from the inventory list provided. The audit team was also able to confirm that a sample of fine art available in one Mission was correctly recorded in the inventory system. Inventory records are also available for materiel stored at commercial warehouses used by Headquarters.

Without accurate and complete inventories of Departmental materiel, there is an increased risk of the disappearance of valuable and attractive assets.

DFAIT is in contravention of the Treasury Board’s Materiel Management policy because "accountable materiel assets must be controlled using records that can be audited." The inconsistency of inventory systems and reporting to management at DFAIT did not permit sufficient audit evidence to be gathered to provide assurance that materiel is accounted for appropriately.

The Materiel Management Renewal Project (MMRP) has the potential to address a number of weaknesses related to the recording and reporting of materiel.

The Materiel Management Renewal Project is a joint initiative by the International Platform Branch and Corporate Finance and Operations Branch to provide a common approach to DFAIT’s materiel management business processes.

The project is leveraging the Integrated Management System (IMS) to create easier ways to input data for non-procurement specialists at Headquarters and at Missions. It is focussing on making the Materiel Management screens of the IMS more user friendly and on integrating Bar-code and Radio Frequency Identification technologies. Departmental common processes are being adapted to improve the accuracy, reliability and accessibility of the Department’s financial information related to materiel management. This is intended to lead to stronger financial management, improved financial controls and data integrity, which should contribute to better decision making. As a result, a broader capacity to support oversight and compliance with the Financial Administration Act, Government of Canada Regulations and policies on Procurement, Materiel Management and Finance are expected to be achieved.

At the time of the audit, the Materiel Management Renewal Project was validating business requirements, developing input screens and testing Radio Frequency Identification systems. The project is awaiting a request for proposals for Bar-code readers to be posted on the MERX Canadian Public Tenders service. The delays related to the acquisition of Bar-code readers were described by the team as a significant constraint to the timely completion of the project.

The project plan originally indicated that the deployment phase would be in the middle of FY 2011-2012. The audit team was advised that the project was in the process of planning to test their solution in the summer of 2011. They plan to seek SIGNET certification and to run a pilot in a small group of Missions during the fall of 2011. The roll-out of the project is expected to take place early in 2012.

Demonstrable senior management support of the Materiel Management Renewal Project is required to ensure buy-in throughout the organization leading to full and sustained use of the Materiel Management Module of the Departmental Integrated Management System by all users.

Even if the technological solution is implemented, it will be successful only if Departmental personnel use it to record materiel. The project team indicated that they did not expect 100 percent take-up of the Materiel Management Renewal Project (MMRP) solution in Missions. Using bar code technology, they would consider 70 percent implementation to be a success. A project team member felt that combining bar coding and Radio Frequency Identification systems may increase the uptake to 90 percent by providing value added – even to Missions with bar code systems in place today. The project team’s assessment was that Missions, which have their own stand-alone systems containing thousands of bar-coded items, would otherwise be reluctant to adopt the central solution.

A partial implementation of the Materiel Management Renewal Project means that the Integrated Management System will not provide Headquarters with complete, accurate and timely information concerning the materiel holdings in the Department. Multiple sources would still have to be consolidated to gather Department-wide information.

It is uncertain at this time when this new system will provide assurance that DFAIT materiel is recorded and reported accurately. Recording inventory of materiel is no small feat. A key decision for senior management will be whether to undertake a resource intensive exercise upon system readiness to ensure accurate inventory at the first possible opportunity versus an incremental approach to building inventory as new materiel is acquired.

The ultimate success of the initiative is dependent upon senior management leadership, continually emphasizing the importance of the IMS-based Inventory management solution, and a sustained focus by involved staff in Headquarters and Missions, following the new business processes.

Recommendation:

- The Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch should ensure that recording and reporting of materiel is improved through the implementation and effective use of the technology solution of the Materiel Management Renewal Project.

The DFAIT Capital Asset Policy is not explicit.

The audit team expected to observe that clear and unambiguous procedures to guide Departmental staff in determining when to capitalize materiel were in place and that recording of capital assets was fully enforced.

The capitalization of assets, individually valued at or above the $10,000 threshold is clearly set out in the DFAIT Capital Asset Policy. However, there is an issue with assets that are separately valued under $10,000 and are bought in a group with the total price higher than this threshold. Currently, there is no consistent practice for recording these assets. For example, a centre of expertise might buy ten assets individually priced at $5,000 in bulk and capitalize those assets in a pool while another centre of expertise would record these items individually resulting in them being expensed in the year they were purchased. There is no specific section in the policy that states who is to decide “when to pool” or “not to pool” or if pooling is to be done at all.

The TB Capital Asset Policy has given flexibility to departments by stating that they “may capitalize assets acquired in a given asset class or pool and amortize the pool over a pre-determined amortization period”. DFAIT has remained vague on this issue and has not customized the statement to the Department’s needs and situation. Consequently, the Departmental Capital Assets Policy and Capital Assets Guidelines do not give employees, responsible for recording the data, any direct guidance on how to deal with this situation.

In some cases materiel such as vehicles that are clearly identified as exceeding the $10,000 threshold, are not recorded correctly in some Missions. According to the Materiel Management Manual, Missions are supposed to notify Headquarters of any purchases of capital assets in order to be provided with an Asset Master Record, Internal Order and Statistical Order numbers. These numbers are needed to identify the purchased materiel as a capital asset and allow it to be recorded and tracked in the Department’s financial system. Some Missions have not sent information regarding their capital assets to Headquarters for several years, while other Missions routinely provided Headquarters with complete information for all their capital asset purchases.

These inconsistent practices put the Department at a risk of not having reliable financial information pertaining to the Department’s capital holdings.

Recommendation:

- It is recommended that the Chief Financial Officer:

- Provide clear policy and guidance to centres of expertise concerning the consistent recording of pooled purchases of assets individually valued less than $10,000;

- Ensure that bureaus which use information on capital assets, agree on a common means of identifying, reporting and recording capital asset purchases and disposals at Missions; and

- Provide clear communication to Missions concerning their requirement to record capital asset purchases and disposals and report these to Headquarters.

Existing practice does not reflect the established procedures to safeguard materiel upon change of occupants of Departmental residences.

Canadian Based Staff usually spend several years at a residence provided by DFAIT when posted to Missions abroad. According to the Materiel Management Manual, inventory verification has to be performed for the Official Residence and the staff quarters in conjunction with the preparation of Occupancy Agreements. This should take place immediately after occupancy of the accommodation and prior to delivery of personal effects and again when the premises are vacated. Of the twelve Missions tested, the majority of incoming Heads of Mission did not apply the policy as intended, in a timely manner.

Often, there is no indication of inventory taken at the time of arrival of the Head of Mission (HOM) supporting his responsibility and accountability for high valued items in the Official Residence and Chancery such as fine art and heritage items. In cases where there was an inventory signed by the HOM, the dates of signature were much later than the date of the HOM’s arrival. The absence of signed inventory sheets can result in weak accounting for the location, amount and condition of art and heritage items, furnishings for the Official Residence and the Chancery. This restricts the Department’s ability, to locate items that may have been misplaced or to hold a HOM accountable for loss or damages.

Recommendation:

- It is recommended that the Assistant Deputy Minister, International Platform Branch develop an effective procedure to inventory materiel and its condition, in the Official Residence and Chancery, upon the arrival of a Head of Mission.

2.4 Strengthen materiel management policies and procedures to provide comprehensive guidance to the Department.

Additional materiel management procedures and direction are required for Headquarters.

The audit team expected to find clear current departmental policy and written guidance in place, to permit materiel management staff and management to fulfill their materiel management responsibilities in Missions and HQ.

The Treasury Board Policy on Management of Materiel provides required direction to government departments. Due to the unique nature of DFAIT operating internationally there is a need for a DFAIT specific policy.

DFAIT does not have a Department-wide Policy on Materiel Management. It has developed some tools, including some related policies, manuals and guidelines. A particularly important tool, the Materiel Management Manual, has been developed for Mission needs. There is no similar tool to provide guidance to Headquarters.

The Materiel Management Manual does not clearly indicate the authority under which the manual is issued, nor does it explicitly differentiate between Departmental policy, directives and guidance. As a consequence, it is hard to tell if the manual is policy with authority or just a guide which has no authority.

Incorporating pertinent information from the manual into policy could strengthen the ability to enforce the procedures and strengthen accountability. In addition, strengthening policy and guidance would contribute to uniform recording and reporting of materiel.

Some materiel management procedures and direction require clarification and enforcement in Missions.

Based on our review, we noted that in general the Materiel Management Manual provides direction, guidance and required procedures to Mission staff involved in materiel management. Objectives are clearly stated and sound, step-by-step procedures are outlined under each chapter of the manual. Nevertheless, additional clarification and direction is needed in certain areas of the manual. The following are some areas of concern identified:

- Cost Recovery: In cases where employees damage DFAIT materiel, there is no consistency in holding employees accountable or recovering the associated costs. The policy has not clearly defined what should be considered normal wear and tear. Consequently it is far too open to interpretation. In order to apply the same standards to all staff and ensure that all appropriate charges are recorded and reported consistently, Missions require clear standards.

- Provision of Materiel for Health Reasons: The audit team was advised that there are requests each year for the Mission to purchase and provide an employee with furnishings or equipment for their residence for personal use that are not in the Materiel Authorization Tables. These items would normally be considered a personal responsibility such as: air purifiers (for people with respiratory / asthma problems), sleep apnoea machines, and orthopaedic mattresses. There is no written direction or policy on this and although there is a requirement for management to accommodate employees in the work place for health and safety reasons, this policy may not be applicable at residences. Clear departmental direction needs to be established.

- Although not explicitly stated in the Materiel Management Manual, the common practice at most Missions is that the Head of Mission does not bid on items offered for disposal by their Mission. The Department is exposed to a conflict of interest situation when the same person deciding to dispose of an item, purchases the item. Although the Materiel Management Manual refers to disposals, more explicit departmental direction needs to be established related to participants in disposal activities.

Recommendations:

- It is recommended that the Chief Financial Officer ensure that Departmental policies, procedures and guidelines are developed and communicated for materiel management activities through a Materiel Management Manual for Headquarters.

- It is recommended that the Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch ensure that the areas of the Materiel Management Manual that are subject to interpretation are clarified, including:

- Cost Recovery;

- Provision of Materiel for Health Reasons; and

- Participation in disposal activities.

At Missions, the practices related to the recreational and personal use of vehicles are not consistently aligned with Departmental policies.

There is a distinction in the Department between personal use of a departmental vehicle, such as transportation from home to workplace, and personal/recreational use of a dedicated vehicle which was part of a program called “The Recreational Hardship Support Program”.

This program was established under Treasury Board authority in July 1983 as an outcome of the McDougall Royal Commission on Conditions in the Foreign Service. It included a provision for the use of vehicles by employees assigned to selected hardship Missions.

The policy concerning the recreational use of vehicles has not been updated to reflect direction from Headquarters in recent years to stop funding. Consequently it was observed that Missions continue to use vehicles for recreational purposes. In February 2010, the Vehicle Fleet Rationalization/Optimization – Savings Initiative report (version 4) documented recommendations for cost savings, in part associated with the elimination of fourteen of these vehicles.

Personal use of DFAIT’s fleet vehicles may be authorized by Heads of Missions in writing in advance of use, only in exceptional circumstances. At Missions, vehicle log sheets were not designed to capture personal use of vehicles, making it difficult to track when official vehicles at Missions are used for personal purposes as in the cases described above. The audit team was informed that the inconsistent application of personal use of official vehicle rules was an issue already known by the Department. A decision-making chart for Personal Use of Official Vehicles at Missions is being drafted to better clarify related policy requirements. At the time of the audit, the chart had not been completed, approved or distributed to Missions.

The audit team noted that a DFAIT Policy on Investment in Vehicle Fleet at Canadian Missions Abroad is being drafted with the intent to implement the findings of the Vehicle Fleet Rationalization/Optimization – Savings Initiative. The policy should include:

- Clear criteria for the determination of vehicle requirements;

- Clear roles and responsibilities in Missions and Headquarters; and

- Requirements for monitoring by and reporting to Headquarters.

It was noted that the draft policy, reviewed by the audit team, continued to lack precision in the above policy elements. The draft policy does not make reference to personal use of vehicles. The audit team was told that this will be addressed in a separate policy.

Recommendations:

- It is recommended that the Assistant Deputy Minister, International Platform Branch and the Chief Financial Officer ensure that the Treasury Board authority for the recreational use of vehicles and the Departmental policy and practice in this regard are aligned.

- It is recommended that the Assistant Deputy Minister, International Platform Branch ensure that the DFAIT Policy on Investment in Vehicle Fleet at Canadian Missions Abroad includes:

- Clear criteria for the determination of vehicle requirements;

- Clear roles and responsibilities in Missions and Headquarters;

- Requirements for monitoring by and reporting to Headquarters; and

- A separate policy is developed to clarify the personal use of Departmental vehicles at Missions.

3. Conclusion

Overall, the Department’s materiel management framework has weaknesses that require senior management attention to permit DFAIT to realize the full potential benefit from its materiel investments.

The Chief Financial Officer is not positioned to exercise functional authority over materiel management although he maintains accountability for procurement and for the integrity of financial information, two areas heavily affected by materiel management. The department should strengthen the control framework for materiel management, clarifying authorities, roles, responsibilities and accountabilities.

There are control weaknesses in key phases of the materiel management life-cycle. Profound weaknesses in inventories of materiel in the Department have contributed to challenges in planning, acquisition, maintenance and disposal of materiel. However, there are opportunities for cost savings and cost avoidance across the life-cycle of materiel management.

Improvements are required in the identification, recording and reporting of materiel. Departmental initiatives such as the Materiel Management Renewal Project (MMRP) are attempting to address some of the identified issues. However, it is not a “silver bullet”. The project has its own challenges to reach full implementation.

While Departmental materiel management policy and direction are well aligned with Treasury Board policies, directives, standards and guidelines, increased clarification, enforcement, and detailed guidance is required.

Appendix A: About the Audit

Objective

The main objective of the audit was to assess the adequacy of DFAIT’s materiel management framework in supporting effective and efficient operations.

The audit also considered the ongoing work of the Materiel Management Renewal Project to determine if additional steps are required to address deficiencies.

Criteria

The selected criteria for the examination phase have been derived, with some adjustments, as per the elements of the draft document "Core Management Controls." These controls have been developed by the Office of the Comptroller General (OCG). They relate to the 2009 Management Accountability Framework (MAF) and aim to fully respond to the engagement objectives and scope. They address effectiveness, efficiency and economy of materiel management.

Audit Criteria 1: Authority, accountability, roles, and responsibilities are well defined and communicated.

Related Management Accountability Framework – Key Elements: Accountability: AC-1 and AC-3; People: PPL-4

Audit Criteria 2: Materiel is effectively and economically managed on a life cycle basis (Assessment and Planning, Acquisition, Operation & Maintenance and Disposal).

Related Management Accountability Framework – Key Elements: Governance and Strategic Direction: G-4; Stewardship: ST-1, 8, 9, 13 & 22

Audit Criteria 3: Accurate and timely financial and non-financial information is available and is used by management.

Related Management Accountability Framework – Key Elements: Stewardship: ST-9, 12, 14 & 20; Governance and Strategic Direction: G-6

Audit Criteria 4: Appropriate policies and procedures are developed, documented and implemented.

Related Management Accountability Framework – Key Elements: People: PPL-4; Policy and Programs: PP-1, 2 & 3; Risk Management: RM-2

Scope

The planning and examination phases of the audit were conducted from June 2010 to January 2011. The audit examined Headquarters and Mission processes with regard to Materiel Management. Regional Offices were scoped out as their Materiel Management activities are limited and as a result were considered as low risk for this audit.

Based on the preliminary analysis and risk assessment the audit team decided to focus on the following group of higher risk assets during process review, control testing and file/transaction review.

- Armoured Vehicles;

- X-Ray Machines;

- Security Equipment;

- Heritage Items / Visual Art;

- Official Residence, Staff Quarters and Chancery furnishings;

- Mission and HQ Vehicles; and

- Headquarter office furnishings, furniture and fixtures.

The audit further scoped out the following categories of assets:

- Financial assets: cash, receivables, prepaid expenses, investments, etc.

- Information Technology (IT) assets as the Office of the Comptroller General undertook the Horizontal Internal Audit of Information Technology Asset Management in Large Departments and Agencies in 2009-2010 in which DFAIT was included and

- Real Property, as the Office of the Chief Audit Executive covered this important area in an audit undertaken in 2010-2011.

Methodology

The audit was conducted in accordance with the International Standards for the Profession of Internal Auditing and the Treasury Board Standards for Internal Audit.

The methodology consisted of:

- Data mining and analysis of records in the Departmental financial system – Integrated Management System (IMS);

- Testing controls in areas of high risk including the examination of specific transactions during the period of August 1, 2009 to September 30, 2010;

- Analyzing financial and non-financial information;

- On site inspection of assets, controls and documentation;

- Examination of the documented materiel management processes prepared by Corporate Policy, Reporting and FIS Implementation (SMSP);

- Walkthroughs of a sample of materiel management processes covering the life cycle;

- Interviews with management and staff at HQ and Mission; and,

- Document review (policies, procedures, Materiel Management Handbook, directives and relevant audit and inspection reports)

Appendix B: Management Action Plan

Audit Recommendation 1: The Department should:

- Confirm to whom the authority for materiel management is delegated and ensure it is aligned with the accountability for same and clearly communicated throughout the organization;

- Mandate the delegated authority to review and strengthen the control framework over the management of materiel; and

- Clearly communicate roles and responsibilities of all parties involved in materiel management.

Area Responsible: Assistant Deputy Minister, Corporate Services (SCM)

Management Action: Note that an agreement establishing the accountabilities for the delivery of common services abroad was signed by the Chief Financial Officer (CFO) and Assistant Deputy Minister (ADM) Platform on May 2, 2011. The Department will:

- Ensure that authority for materiel management is delegated and aligned with the accountability for same and is clearly communicated throughout the organization.

(Expected Completion Date: Complete) - A review of materiel management practices has been completed as part of the initial stage of the Materiel Management Renewal Project (MMRP). Once completed and implemented, the MMRP will ensure standardized processes and a strengthened control framework.

(Expected Completion Date: Complete) - The roles and responsibilities for materiel management will be clearly communicated.

(Expected Completion Date: Complete)

Audit Recommendation 2: The Chief Financial Officer should articulate clear requirements for materiel management planning in HQ and Missions, supported by standard processes, procedures and tools, as appropriate.

Area Responsible: Headquarters AdministrationBureau (SPD)

Management Action: The CFO will provide clear requirements for materiel management planning in HQ and Missions and will develop standard processes, procedures and tools, which will be communicated and enforced during the MMRP implementation.

(Expected Completion Date: Complete)

Audit Recommendation 3: It is recommended that, the Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch ensure that within the Department, short and long-term acquisition, refurbishment and disposal project plans be clearly identified and communicated to all affected parties.

Area Responsible: Platform Corporate Services (AAD)

Management Action: Upon full implementation of the MMRP project, standard information will be available to support planning. Plans for assets requiring cyclical replacement will be developed and communicated using a commodity based phased approach.

(Expected Completion Date: Complete)

Audit Recommendation 4: The Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch identify and implement effective ways and means of providing oversight to vehicle acquisitions in Missions, and consider the benefits of a centralFootnote 1 fleet management process for missions.

Area Responsible: Client Relations and Mission Operations (AFD) in collaboration with AAD

Management Action:

- For CFO actions, refer to item #2 above.

(Expected Completion Date: Complete) - Upon full implementation of the MMRP project, the benefits of a central fleet management process for missions will be investigated.

(Expected Completion Date: Complete) - Fleet acquisitions, vehicle selection, international trade agreement thresholds, and green considerations will all be overseen centrally by Mission Client Services (AFO). AFO will allocate funding to missions for planned vehicle purchases, as supported by the mission budget planning exercise; funds will only be transferred when notified by mission.

(Expected Completion Date: Complete)

Audit Recommendation 5: The Assistant Deputy Minister, International Platform Branch should:

- Develop a process to dispose of artwork that is no longer required for Departmental operations and establish a trigger for the disposal of works of art such as a certain number of years in continuous storage (implying undesirability) or a minimum appraised value (implying a work so valuable they require special conservation expertise);

- Consider ways and means to ensure the Department realizes maximum revenue from the disposal of surplus materiel at Missions; and

- Expand the application of Mission eXchange services to address acquisition and disposal actions in Headquarters.

Area Responsible: Physical Resources (ARD)

Management Action: ADDENDUM:

- Revisions to the Policy on Disposal of Works of Art were made following the presentation of this recommendation.

- Art work is not to be sold.

- This recommendation therefore no longer applies.

(Expected Completion Date: Complete)

Audit Recommendation 6: The Assistant Deputy Minister, International Platform Branch and the Chief Financial Officer should consider the benefits of a comprehensive fleet management serviceFootnote 2 for the Headquarters Operational fleet and its potential application to some Missions.

Area Responsible: AAD for HQ and AFD for North American Missions

Management Action: The cost effectiveness of a comprehensive fleet management service (ARI) for the Headquarters Operational Fleet and the North American Missions will be investigated.

(Expected Completion Date: Complete)

Audit Recommendation 7: The Assistant Deputy Minister, International Platform Branch and the Chief Financial Officer should adjust the size of the Department’s fleet taking into consideration the recommendations of the Vehicle Fleet Rationalization / Optimization – Savings Initiative.

Area Responsible: AFD & SPD

Management Action: The Department's fleet will be reviewed to take into consideration the fleet rationalization /Optimization - savings initiative.

(Expected Completion Date: Complete)

Audit Recommendation 8: The Chief Financial Officer should ensure that a means is put in place to track Warehouse expenses, to allow management to clearly identify the cost of storing and crating Departmental materiel at Headquarters and Missions in order to improve the management of warehousing.

Area Responsible: SPD

Management Action: Efforts will be made to provide functionality within the MMRP system environment to adequately capture and report on warehousing expenses for both HQ and Missions.

(Expected Completion Date: Complete)

Audit Recommendation 9: The Chief Financial Officer, the Assistant Deputy Minister International Platform Branch and the Assistant Deputy Minister Consular Services and Emergency Management Branch should initiate a study to assess the cost-benefits of consolidating the Department’s warehouses in the National Capital Region.

Area Responsible: AAD

Management Action: A study to assess the cost-benefits of consolidating the Department’s warehouses in the National Capital Region will be conducted.

(Expected Completion Date: Complete)

Audit Recommendation 10: The Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch should ensure that recording and reporting of materiel is improved through the implementation and effective use of the technology solution of the Materiel Management Renewal Project.

Area Responsible: SPD/AAD

Management Action: The Materiel Management Renewal Project (MMRP) currently being developed will ensure that the functionality required to efficiently and effectively capture and report on materiel management activity is implemented using an integrated technology that clearly supports all stakeholders while eliminating the need for subordinate “black book” systems.

(Expected Completion Date: Complete)

Audit Recommendation 11: The Chief Financial Officer should:

- Provide clear policy and guidance to centres of expertise concerning the consistent recording of pooled purchases of assets individually valued less than $10,000;

- Ensure that bureaus which use information on capital assets, agree on a common means of identifying, reporting and recording capital asset purchases and disposals at Missions; and

- Provide clear communication to Missions concerning their requirement to record capital asset purchases and disposals and report these to Headquarters.

Area Responsible: Corporate Accounting (SMD)

Management Action: The Capital Asset Policy will be updated to clarify when to record pooled purchases of assets individually valued at less than $10,000. This will be done at the same time as the CFO led Capital Asset Review, which is planned for completion by March 2012. The updated Policy will be communicated by the CFO throughout the Department once it has been completed.

(Expected Completion Date: Complete)

Audit Recommendation 12: The Assistant Deputy Minister, International Platform Branch should develop an effective procedure to inventory materiel and its condition, in the Official Residence and Chancery, upon the arrival of a Head of Mission.

Area Responsible: AAD

Management Action: The procedures in the Materiel Management Manual will be strengthened and the changes communicated to the Missions as appropriate.

(Expected Completion Date: Complete)

Audit Recommendation 13: The Chief Financial Officer should ensure that Departmental policies, procedures and guidelines are developed and communicated for materiel management activities through a Materiel Management Manual for Headquarters.

Area Responsible: SPD

Management Action: Departmental policies related to Materiel Management will be established and clearly communicated. Supporting procedures and guidelines will be updated or developed to ensure a consistent and comprehensive approach to satisfying policy objectives. A Materiel Management Manual for Headquarters, similar to the Mission Manual, will be developed and implemented.

(Expected Completion Date: September 2015)

Audit Recommendation 14: The Chief Financial Officer and the Assistant Deputy Minister, International Platform Branch should ensure that:

- The areas of the Materiel Management Manual that are subject to interpretation are clarified, including:

- Cost Recovery;

- Provision of Materiel for Health Reasons; and

- Participation in disposal activities.

Area Responsible: SPD/AAD

Management Action: For HQ, a newly developed Materiel Management Manual will ensure that clarification is provided.

(Expected Completion Date: Complete)

For Missions, clarifications will be integrated with the Materiel Management Manual and changes communicated.

(Expected Completion Date: Complete)

Audit Recommendation 15: The Assistant Deputy Minister, International Platform Branch and the Chief Financial Officer should ensure that the Treasury Board authority for the recreational use of vehicles and the Departmental policy and practice in this regard are aligned.

Area Responsible: AFD in consultation with Foreign Service Directives (AED) & AAD

Management Action: Proposals on the recreational use of vehicles will be presented to Senior Management and when approved will be included in the Mission Vehicle use policy. They will be implemented simultaneously with the Fleet Rationalization policy.

(Expected Completion Date: Complete)

Audit Recommendation 16: The Assistant Deputy Minister, International Platform Branch should ensure that the DFAIT Policy on Investment in Vehicle Fleet at Canadian Missions Abroad includes:

- Clear criteria for the determination of vehicle requirements;

- Clear roles and responsibilities in Missions and Headquarters;

- Requirements for monitoring by and reporting to Headquarters; and

- A separate policy is developed to clarify the personal use of Departmental vehicles at Missions.

Area Responsible: AFD in consultation with AAD

Management Action: Amendments to the Materiel Management Manual will: ensure uniform criteria for vehicle specifications; clearly delineate roles and responsibilities of Mission and Headquarter; provide specific directions on personal use of Departmental vehicles at missions.

(Expected Completion Date: Complete)

Further study will be undertaken to investigate developing an application where information to support monitoring and reporting can be captured and analyzed.

(Expected Completion Date: Complete)

Appendix C: Figures

Figure 4: Materiel Expenditures FY 2009-2010

Figure 4 Text Alternative

| Type of Expenditure | Expenditures($) |

|---|---|

| Household furnishings | $11,229,607 |

| Office furniture and fixtures | $11,683,621 |

| Artwork | $189,508 |

| Security/safety/access items | $7,193,516 |

| Office supplies and misc small items | $7,180,702 |

| Fuel (vehicle and heat) | $7,129,049 |

| Motor vehicle purchase and repair | $6,352,984 |

| Books, subscriptions & newspapers | $3,943,278 |

| Communication assets | $1,892,979 |

| Repairs and maintenance | $1,499,129 |

| Heating and air cond systems | $511,898 |

The main types of materiel acquired by DFAIT include office and household furniture, office supplies, security-related goods and vehicles. In FY 09/10 these purchases were broken down as shown in Figure 4 above.