The economic impact of COVID-19 on Canada’s international education sector in 2020

Executive summary

View/download the Economic impact of COVID-19 on Canada’s international education sector in 2020 (PDF, 833 KB)

The COVID-19 pandemic has negatively affected a number of sectors across the economy at large and has caused major disruptions to the global education sector. Whether we look at school closures, the rise in online/remote learning, or the impact on the international student sector, the entire spectrum of education activities has been impacted.

With an estimated pre-pandemic contribution of over CAD $22.7 billion in expenditures by international students, the international education sector is critical to Canada[1]. COVID-19 lockdowns, the subsequent border closures, and travel restrictions both domestically and around the world, greatly affected student mobility and consequently the international student sector. This study looks at quantifying the economic impact of COVID-19 on Canada’s international education sector in 2020. For the purposes of the study, the COVID-19 impact has been defined as the difference between the theoretical impact on the Canadian economy had the pandemic not happened[2], and the actual recorded impact in 2020.

The study sought to assess the impact of COVID-19 in 2020 through analysis of:

- The most recent data on the number of international students and their expenditures in Canada;

- The effect of reduced enrollment and a large scale transition to on-line learning on Canada’s exports of education services;

- The costs associated with adjustments made by institutions to accommodate international students in response to the pandemic;

- Changes in revenue and expenditures derived from international students in Canada because of changes in enrollment and the transition to on-line learning.

Using the most up-to-date data on the number of study permit holders in Canada provided by Immigration, Refugees and Citizenship Canada (IRCC), the study found that the international student sector contracted significantly in 2020 because of the pandemic. The key findings of the report are as follows:

- The number of international students studying in Canada on December 31, 2020 was 533,370 (a 17% decrease from 2019), whereas the predicted number of students studying in Canada (using a base-case of no-COVID scenario) would have been 708,387, i.e. a 24% decrease. This decrease can be partly explained as a temporary decline, as a number of students likely switched to online-study while waiting for border and travel restrictions to ease, meaning this number is likely to go up in future as the pandemic eases.

- Similarly, for short-term students i.e. those who do not require a Study Permit, the number of student weeks was estimated to be 37% lower than what would be predicted in the case of a no-pandemic scenario[3].

- The decrease in the number of students studying in Canada equated to a loss of CAD $7.3 billion in total student expenditures[4], leading to a total loss of CAD $7.1 billion from Canada’s Gross Domestic Product in 2020[5].

- The loss in student expenditures equated to a loss of CAD $4.5 billion in labour income, or a loss of 64,300 full-time jobs in Canada (both directly and indirectly).

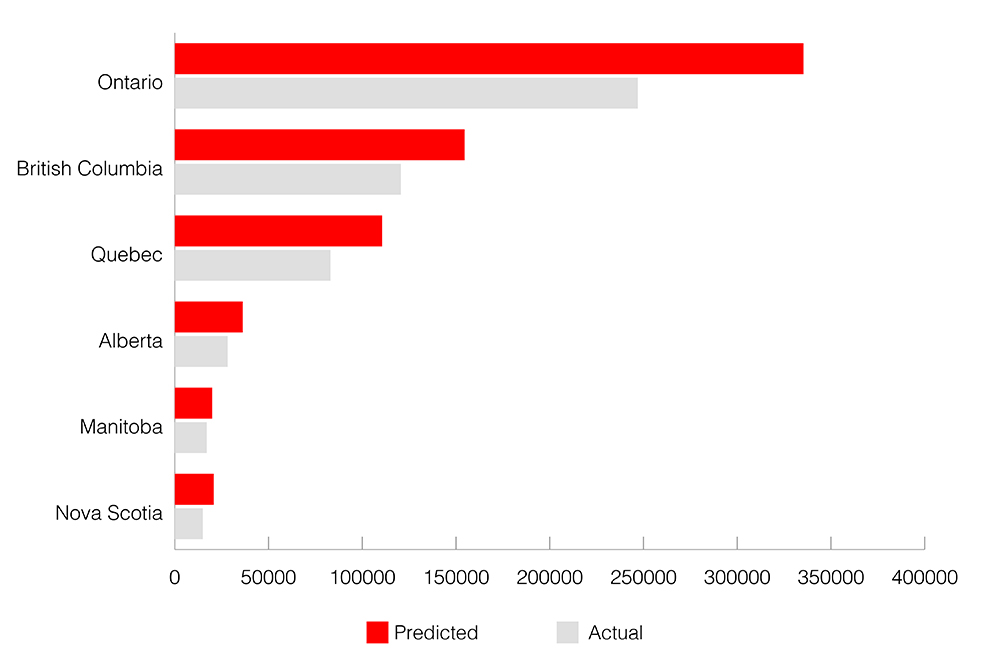

Disaggregating the data at the provincial level, in terms of GDP loss the provinces with the largest numbers of international students were most affected, with Ontario losing over $4.1 billion in GDP, followed by British Columbia with a $1.2 billion loss, and Quebec with just over $1 billion. However, in terms of number of students, the top three impacted provinces as measured by their one-year decline in the number of international students were in Atlantic Canada, with New Brunswick down 34.7%, Newfoundland and Labrador down 28.4% and Nova Scotia seeing a 28.1% decline from 2019; the three Territories collectively experienced a 33.2% decline over this period.

Figure 1 – Estimated Impacts of COVID-19 on Study Permit Holders in 2020 by Province/Territories

View accessible version of figure 1

- Ontario (predicted) – 335,327

- Ontario (actual) – 246,975

- British Columbia (predicted) – 154,548

- British Columbia (actual) – 120,565

- Quebec (predicted) – 110,584

- Quebec (actual) – 83,040

- Alberta (predicted) – 36,224

- Alberta (actual) – 28,210

- Manitoba (predicted) – 19,945

- Manitoba (actual) – 17,040

- Nova Scotia (predicted) – 20,804

- Nova Scotia (actual) – 14,955

- Saskatchewan (predicted) – 12,378

- Saskatchewan (actual) – 9,420

- New Brunswick (predicted) – 8,439

- New Brunswick (actual) – 5,510

- Newfoundland and Labrador (predicted) – 5,559

- Newfoundland and Labrador (actual) – 3,980

- Prince Edward Island (predicted) – 4,257

- Prince Edward Island (actual) – 3,440

- Territories (predicted) – 322

- Territories (actual) – 215

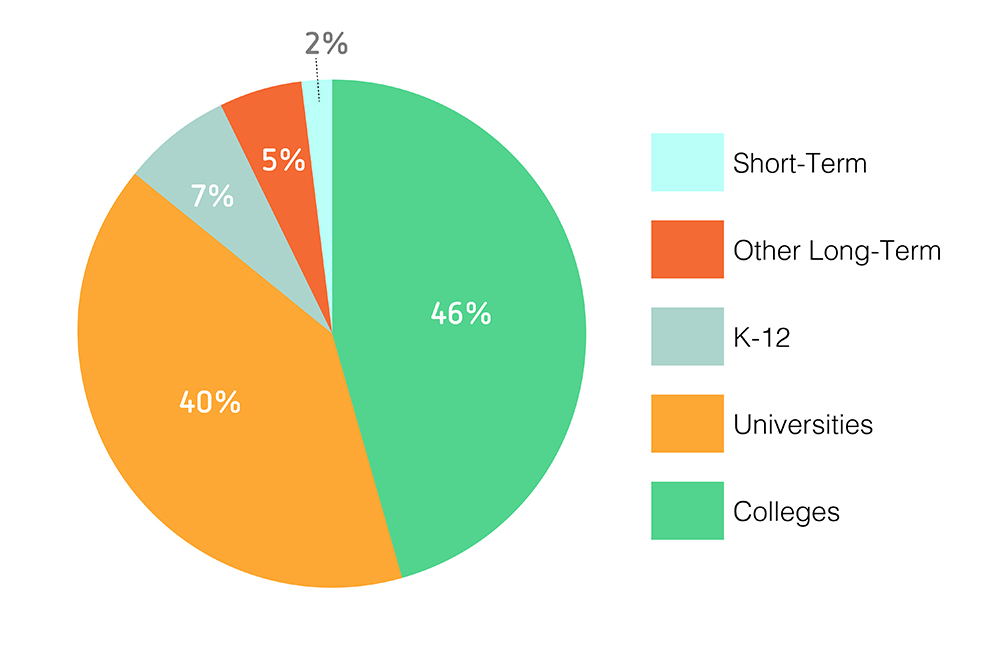

By study level, the decline in the number of international students studying at the college level contributed to the greatest estimated GDP loss, measured at $2.55 billion, followed by university students at $2.26 billion. This is illustrated in the figure below. Note that CEGEP students and Quebec Program students are included in ‘Other Long-Term’, while ‘Short-Term’ includes language students and K-12 students who did not study on study permits.

Figure 2 – Estimated Share of Total GDP Losses in 2020 by Study Level

View accessible version of figure 2

- Colleges – 46%

- Universities – 40%

- K-12 – 7%

- Other Long-Term – 5%

- Short-Term – 2%

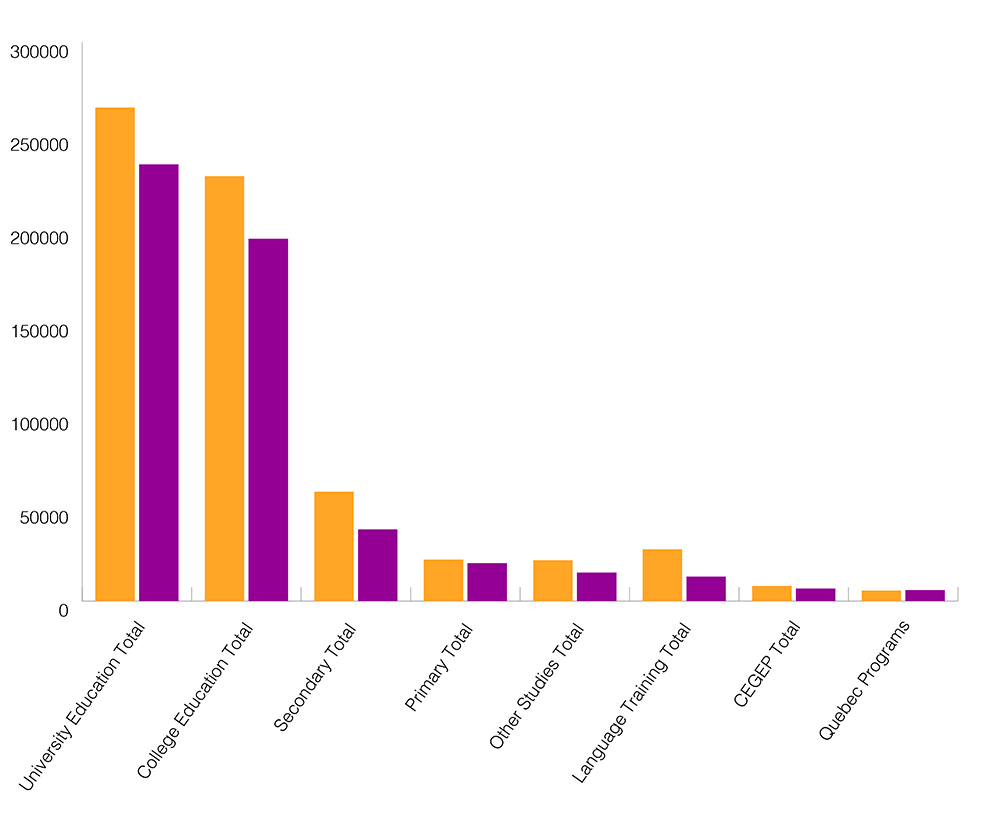

On a more granular level, to see how the pandemic affected each level of study in 2020, the chart below illustrates the difference in international students by study level between December 31, 2019, and December 31, 2020. The numbers of international language students declined the most, by nearly 53%, followed by international secondary students at approximately 34%.

Figure 3 – Canada - Study Permit Holders on December 31st by Study Level, 2019 vs 2020

View accessible version of figure 3

- University Education Total (2019) – 264,965

- University Education Total (2020) – 234,410

- College Education Total (2019) – 228,135

- College Education Total (2020) – 194,510

- Secondary Total (2019) – 58,740

- Secondary Total (2020) – 38,525

- Primary Total (2019) – 22,350

- Primary Total (2020) – 20,375

- Other Studies Total (2019) – 21,955

- Other Studies Total (2020) – 15,340

- Language Training Total (2019) – 27,850

- Language Training Total (2020) – 13,165

- CEGEP Total (2019) – 8,110

- CEGEP Total (2020) – 6,765

- Quebec Programs (2019) –5,685

- Quebec Programs (2020) – 5,900

The pandemic’s impact on the numbers of international students from major source countries varied as well. These declines ranged from a 4% decrease for study permit holders from Iran to 24.6% for South Korean study permit holders. The top two source countries, India and China saw declines of 17.6% and 16.9%, respectively.

Figure 4 – Top 10 Source Countries for Study Permit Holders on December 31, 2020 compared to December 31, 2019

View accessible version of figure 4

- India (2019) – 218,790

- India (2020) – 180,275

- China (2019) – 140,775

- China (2020) – 116,935

- Vietnam (2019) – 21,510

- Vietnam (2020) – 18,910

- France (2019) – 23,890

- France (2020) – 18,295

- South Korea (2019) – 24,110

- South Korea (2020) – 18,170

- Iran (2019) – 14,635

- Iran (2020) – 14,045

- United States of America (2019) – 14,895

- United States of America (2020) – 12,740

- Brazil (2019) – 14,505

- Brazil (2020) – 11,050

- Nigeria (2019) – 11,915

- Nigeria (2020) – 10,635

- Bangladesh (2019) – 8,400

- Bangladesh (2020) – 7,785

Of the top countries with over 1,000 study permit holders on December 31, 2019, there were 14 countries which experienced declines of 20% or more from 2019 to December 31, 2020. This was led by Spain with a 58.8% drop, Saudi Arabia at 50.7% and Germany at 50.2%.

Figure 5 – Source Countries with Largest Declines in Study Permit Holders from 2019 to 2020 (minimum 1,000 Study Permit Holders in 2019)

View accessible version of figure 5

- Spain – 58.8%

- Saudi Arabia – 50.7%

- Germany – 50.2%

- Japan – 36.8%

- Italy – 34.8%

- United Kingdom – 31.4%

- Thailand – 28.8%

- Mexico – 26.0%

- South Korea – 24.6%

- Turkey – 24.4%

- Brazil – 23.8%

- France – 23.4%

- Ukraine – 22.2%

Other impacts

- Research – Based on conversations with college and university officials, it was concluded that the impact of COVID-19 on research expenditures in the international educational student sector was minor in 2020, as most of the research work continued using online collaboration tools. Universities Canada noted that on-campus research activities continued with minimal disruption and international collaborations adapted accordingly[6].

- Student Emergency Funding - As many international students were required to leave student residences starting in March 2020, they incurred additional costs for private accommodations. In some cases, students needed emergency funding to overcome their financial difficulties, part of which came from the institutions themselves. No reliable data exists for this activity, but based on discussions with key informants, the overall cost appears modest.

- Cost of Managing Pandemic - Managing the pandemic has been an ongoing activity throughout 2020 for all sectors of the economy. Quantifying this impact is not possible, but there is no question the health crisis has resulted in significant time spent by management and others that would otherwise had been allocated to other activities. In addition, direct costs would include additional cleaning, COVID-19 signage, and other measures to comply with provincial health regulations.

- Cost of Repatriating Students - The international education sector would have incurred some costs associated with emergency repatriation of students working on research projects and studying abroad. As these students would have returned at some point in time, the net costs of this activity would have been minimal.

- Online/Remote Learning – The pandemic contributed to a rise in online learning across the education sector and has served as a catalyst for growth in educational technology on a global level. According to Quacquarelli Symonds, a leading research firm in the area of international education:

The current situation has shone a light on new domestic and international markets, allowing institutions to maximize the value of their offering by reaching people that could not be reached before. The outbreak has accelerated the development of institutions’ online learning capabilities and altered the way they communicate their capabilities and reputations to students[7].

The growing market for online education has been driven by technological advancements on the part of educational institutions, a market of eager learners, and increasing penetration of smart devices across the globe. Various estimates of the overall global market in online education project growth of between 8% and 13% each year until 2025, from USD $222 billion in 2020 to a projected USD $350 billion.

Canadian institutions proved capable of quickly adapting to the pandemic situation by shifting to online study early on. Being relatively adept at this type of course delivery helped mitigate a potential loss in income in 2020-21, and also gave institutions the opportunity to further develop their online delivery of programs. In Canada, an informal inquiry into the ratio of international students studying at Nova Scotia institutions during the 2020-21 school year found that 10% of all students studying online were doing so from outside of Canada.

It is important to note that the conclusions in this report have focused on the economic impact of international students studying in Canada. Depending on the institution of study, 2020 saw varying mixtures of online and in-person classes. However, there was a component of the international student population that took their entire course-load online from their home country. A significant portion of these students who began their studies online were ‘temporary online students’, i.e. those who postponed their arrival to Canada to a later date waiting for the pandemic situation to stabilize. For the purposes of this study, the expenditures of these students (notably their tuition fees) were not, in fact, counted. The student numbers in this study are based on the actual number of students in Canada on Dec. 31, 2020. Regardless of the likely temporary nature of the spike in online study in 2020, given the growth projections in the online education market, and the fact that this trend is likely set to continue well beyond the pandemic, remote/online study represents a significant opportunity for Canada’s international education sector, economic and otherwise.

Conclusion

To state that the COVID-19 pandemic disrupted the education sector would be a gross understatement. From elementary schools to post-secondary institutions, the entire sector felt the impact of the pandemic. In Canada, the international student sector faced a significant negative economic impact. A steep 17% year-on-year decline in the number of international students studying in Canada led to an estimated CAD $7.3B loss in total student expenditures, which translated to a decline of CAD $7.1B in Canada’s GDP in 2020. This represents a significant loss, and as the analyses show, this loss was felt unevenly across Canada as well as within the sector itself, with certain provinces and certain segments/levels of study being disproportionately impacted. Although the report looked at losses at the provincial/territorial level, the real economic impact is oftentimes more significant at the community level; given that university and colleges frequently represent major industries at the local level, the significance of the impact is compounded by the fact that often these areas are not economically diverse enough to offset the contraction of the international student economic sector.

One of the bright spots from this overwhelmingly negative year, however, has been the rise of online/remote learning. The pandemic forced institutions to accelerate this transition, in order to stay competitive and adjust to the travel restrictions and uncertain circumstances facing their international students. The COVID-19 health crisis resulted in most long-term student programs switching to an online format at the end of the winter 2020 semester, continuing through to the end of 2020.

In conclusion, despite these challenging circumstances, the Canadian government’s management and handling of the crisis, particularly with regards to the safe and orderly entry of international students, received positive recognition globally. More than a year into the pandemic, there are signs pointing to a recovery and Canada continues to be viewed as a top international study destination by prospective students, parents and agents.

To request the full version of the report, please contact Eduresearch-Edurecherche@international.gc.ca.

References

[1] Canmac 2018 Economic Impact Assessment Study.

[2] Using annual and monthly IRCC data, the theoretical impact of a no-COVID-19 situation was calculated by creating a regression model through the analysis of growth trends of study permit holders in Canada in 2018 and 2019.

[3] The number of short-term international students was estimated using student numbers provided by Languages Canada and the Canadian Association of Public Schools-International, namely the confirmed numbers of short-term international students who did not require study permits.

[4] Student expenditure estimates were taken from a variety of sources. The main expenditure categories estimated were as follows:

- Tuition and compulsory fees

- Books and materials

- Accommodation

- Discretionary expenses

- Transportation

- In line with previous studies, scholarships and awards were estimated at 1% of tuition.

[5] GDP impact refers to both direct impacts and indirect impacts, which measures the impact on firms supplying goods and services to the education services and other sectors.

[6] Correspondence with Universities Canada representative, March 18, 2021, and particularly for the STEM programs of study.

[7] What Opportunities and Challenges does Online Learning Present to the Admissions Office During COVID-19 and beyond? Quacquarelli Symonds, 2020.

- Date modified: