Archived information

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Audit of the Administration of the Foreign Service Directives

Final Report

November 2015

Table of Contents

- Executive Summary

- 1. Background

- 2. Observations and Recommendations

- 3. Conclusion

- Appendix A: About the audit

- Appendix B: Audit scope in FSD expenditures

- Appendix C: Testing results—FSDs requiring monitoring

- Appendix D: FSD payments requiring descretionary authority

- Appendix E: Management action plan

Executive Summary

In accordance with the approved Transitional Risk-Based Audit Plan for 2014-2015, the Office of the Chief Audit Executive at the Department of Foreign Affairs, Trade and Development (DFATD, the Department) conducted an audit of the Administration of the Foreign Service Directives (FSDs, the Directives).

The FSDs are designed to provide a system of allowances, benefits and conditions of employment that, in combination with salary, enables the Department to recruit, retain, and assign qualified staff to its missions around the worldFootnote 1. The provisions of the Directives recognize differences among regions, countries and cities in terms of living conditions, cost of living, traveling home for holidays, children’s schooling or day care, adequate housing, etc.

The Directives are co-developed with bargaining agents and public service employers at the National Joint Council of the Public Service of Canada (NJC)Footnote 2 and form part of the employees’ collective agreements. In 2014-2015, the Department spent approximately $135 million on 41 FSDs to 1,767 Canada-based staff who were accompanied by 2,991 dependants, posted in 174 missions and located in 107 countries.Footnote 3

The objective of this audit was to provide assurance that the FSDs are managed in an effective, efficient and financially sustainable manner as well as being consistently applied, and respecting their guiding principles of comparability, incentive-inducement and program-related provisions. The audit focused on the application of the FSDs from fiscal year 2012-2013 through to December 2014. Specifically, the audit scope included:

- FSD payments authorized at both headquarters (HQ) and missions from April 1 to December 31, 2014 for sample testing purposes;

- administration and management practices for the past three years;

- the FSD Portal and data; and

- financial forecasting practice and FSD deficit management for the past four years.

The audit team observed that the Department has a management structure that supports the day-to-day administration of the FSDs. Audit work on selected transactions determined that there are opportunities to improve efficiency of the FSD administration. It should be noted that the materiality of the transactional errors found was not significant. Nevertheless, the auditors found that the following areas require management attention:

- Formal risk management of the FSDs was not evident, which in turn may impact on the Department’s ability to make fully informed decisions, focus monitoring and to support an efficient FSD administration;

- Some of the approval of the FSD claims was not supported by sufficient information and consistent assessment against the FSD policy requirements, which presents a risk that some approved FSD claims may not be admissible;

- Internal controls over source information from various branches for the calculation of the FSD benefits were not sufficient. This led to incorrect payments and numerous adjustments; and

- FSD fund management and budgeting practices should be improved.

Conclusion

The management of FSDs is structured to support the day to day administration of FSDs and to ensure compliance with the FSDs; however, formal risk management and risk-based monitoring were not evident to allow for informed decision-making and efficient FSD administration. In addition, internal control weaknesses were identified in relation to: FSD payment approval; source information used in the calculation of the FSD benefits and entitlements; as well as in the area of the FSD funds management.

Statement of Conformance

In my professional judgment as Chief Audit Executive, the audit was conducted in conformity to the Institute of Internal Auditors’ International Standards for the Professional Practice of Internal Auditing and the Internal Auditing Standards for the Government of Canada, as supported by the results of the quality assurance and improvement program. Sufficient and appropriate audit procedures were conducted and evidence gathered to support the accuracy of the findings and conclusion contained in this report, and to provide an audit level of assurance. The findings and conclusion are based on a comparison of the conditions, as they existed at the time of the audit, against pre-established audit criteria that were agreed upon with management. The findings and conclusion are applicable only to the entity examined, for the scope and period covered by the audit.

Chief Audit Executive

1. Background

The internal audit of the administration of Foreign Service Directives (FSDs, the Directives) was identified in the approved Transitional 2014-2015 Risk-Based Audit Plan. This audit was included in the Plan due to the important role of the Directives in support of the government programs outside of Canada as well as the financial materiality of the FSD budget.

FSDs in the Context of the Government of Canada

FSDs are a series of 41 benefits, allowances, conditions of employment and/or interpretations of specific issues provided to employees who work outside of Canada. The purpose of the FSDs is to enable departments and agencies to recruit, retain and deploy qualified employees in support of government programs outside of Canada. Payments made under the FSDs during an employee’s posting cover a range of expenses including foreign service premiums, post differential allowances, post living allowances, relocation and accommodation expenses. A complete listing of FSDs is available online.

FSDs are co-developed with bargaining agents and public service employers at the National Joint Council (NJC) and form part of the employees’ collective agreements of the participating parties under the By-Laws of the NJC. As mandated by the By-Laws of the NJC, the Foreign Service Directives Committee is in place and consists of both the bargaining agents and departmental representatives. The Committee’s role is to review and recommend changes to the FSDs and also hear final level grievances on these authorities. This Committee recommends changes to various rates and premiums on a periodic basis. FSDs are reviewed cyclically, generally every three years by the Committee, to ensure continued relevance and sufficiency.

FSD Administration at DFATD

The Department administers the FSDs for its employees, and their respective dependants, who work in Canada’s missions abroad. These include DFATD career foreign service employeesFootnote 4 and foreign assignment employeesFootnote 5. As well, DFATD administers FSDs for employees from other government departments (OGDs) who have signed a Memorandum of Understanding with DFATD to administer the FSDs on their behalf.

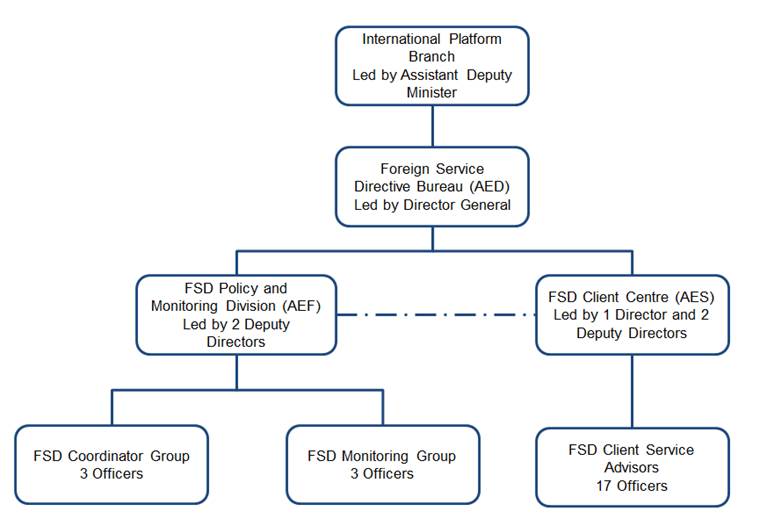

Reporting to the International Platform Branch of DFATD, the FSD Bureau (AED) is responsible for administering the payment of FSDs. AED has two divisions through which its mandate is carried out: the FSD Client Service Centre (AES) and the FSD Policy and Monitoring Division (AEF). AES plays a key role in providing client-oriented advice to employees and their dependants who are assigned abroad. AEF is responsible for clarifying/interpreting policies and contributing to the improvement of the FSD package on behalf of the Department, while monitoring the expenditures made under the authorities provided by the FSDs. In addition, AEF also provides the lead support on the DFATD position for the FSD Cyclical Review.

There are approximately 17 FSD client service advisors led by one director and two deputy directors. Client service advisors are assigned to various missions. There are four FSD coordinators led by a deputy director and three FSD Monitoring Officers led by a unit head, who are responsible for verifying and monitoring FSD payment expenditures. In fiscal year 2014-2015, these employees and missions processed just over $135 million in financial benefits related to FSDs. The following organizational chart shows the reporting relationships for DFATD FSD management and administration.

Text Alternative

- International Platform Branch - Led by Assistant Deputy Minister

- Foreign Service Directive Bureau (AED) - Led by Director General

- FSD Policy and Monitoring Division (AEF) - Led by 2 Deputy Directors

- FSD Coordinator Group - 3 Officers

- FSD Monitoring Group - 3 Officers

- FSD Client Centre (AES) - Led by 1 Director and 2 Deputy Directors

- FSD Client Service Advisors - 17 Officers

- FSD Policy and Monitoring Division (AEF) - Led by 2 Deputy Directors

- Foreign Service Directive Bureau (AED) - Led by Director General

In 2013-2014, there were a total of 41 Directives applicable to approximately 1,700 employees and their 2,900 eligible dependants who were posted in 174 missions located in 107 countriesFootnote 6. Some of the FSD payments were also made directly to approximately 800 service suppliers worldwide (i.e. moving companies, schools). AED staff and missions process more than 90,000 transactions annually. With continually changing factors affecting the FSD benefits and entitlements, and a large client base, the FSD administration process is complex.

The FSD Portal

In response to this complexity, an FSD Portal was launched in 2012 with 11 FSDs included in the first phase of implementation. The FSD Portal allows employees assigned abroad to submit and track FSD requests and view their profiles. The FSD Portal was designed and implemented as a means to:

- improve data integrity and comptrollership of FSD expenditures;

- bring greater consistency and efficiency to the administration and tracking of the FSDs;

- provide better reporting and monitoring capabilities;

- provide improved client oriented service; and

- maximize productivity of AED and mission resources which are involved in the administration of the FSDs.Footnote 7

The second phase of the FSD Portal implementation, for the remainder of the FSDs, was scheduled to be completed within a 2-4 year timeframe from the project launch.

2. Observations and Recommendations

The audit team conducted an examination of FSDs based on the criteria described in Appendix A. The auditors interviewed 15 DFATD employees, selected 10 case studies and tested 138 transactions from 10 different FSDs. Based on this work, observations and recommendations were made and developed, which are detailed below, in the themes of: governance and management structure; FSD compliance and administration; and FSD expenditure forecasting and fund management.

2.1 Governance and Management Structure

2.1.1. Departmental Guidance

The Department has guidelines, instructions and policy clarifications that are in compliance with the NJC requirements for FSDs. Documentation is readily accessible to DFATD employees as well as those of OGDs who are, or will be serving on assignments outside Canada.

Within DFATD, guidance to employees on the application of FSDs is provided predominately by AES client service advisors. Desk Procedures have been developed specifically for the FSD client service advisors that provide a detailed overview on how to consistently and accurately process the FSDs. Employees rely on the knowledge and advice provided by the client service advisors to ensure the principles of the FSDs are respected. In addition, training for new service advisors primarily took the form of job shadowing. A weekly Questions and Answers session is organized by the head of AEF and intended to address common issues and concerns raised during service provision.

Guidance on FSDs is also available on the Department’s intranet and within the FSD Portal, where DFATD employees can find the procedures and steps on where, when and how to apply for individual FSDs. In addition, a Foreign Service Handbook that was developed by AED and dated in 2014 for employees of DFATD and OGDs to assist them and their dependants throughout the preparation for, and during the full posting cycle. AEF coordinates the updating of this handbook which is available on line as of 2015-2016.

In compliance with the FSDs, the Department conducts pre-posting briefing programs at HQ for DFATD and OGD employees. These programs provide a detailed briefing with respect to the specific application of FSDs and related provisions and procedures.

2.1.2. Management Structure

The majority of the managerial decisions and activities with regard to the administration of the FSDs take place at HQ. However, given that some of the FSD payments occur in missions or are paid in local currency, the Heads of Mission and Management Consular Officers (MCO) also assume responsibilities for reviewing, verifying and approving certain FSD claims in compliance with the departmental delegation instrument.

Interdepartmental Working Groups and Sub-Committees

As required by certain FSDs, exceptional claims must be submitted for review and approval by an interdepartmental co-ordinating committee. Interdepartmental working groups were established. Working Group A (WGA) is chaired by the representative from Treasury Board Secretariat (TBS) and provides policy guidance on the application of the FSDs on complex cases, mostly with regard to the intent of the Directives. Working Group B (WGB) is chaired by AEF and attended by OGD representatives. An Education Sub-Committee reviews cases specific to education provisions and makes recommendations on education requests and submits them to WGB for consideration.

The auditors’ examination of WGB minutes showed that decisions made by the Committee members were based on a review of documentation. Discussions and decisions were clearly stated and appropriately documented. As the WGA focuses on policy, which is outside the scope of the audit, their minutes were not examined.

Operational Model

The review of the AED organizational charts, work descriptions, and interviews with staff indicated that the current operational model supports the AED mandate and its daily operations. In addition, the work descriptions clearly articulate the respective roles and responsibilities. Interviews conducted with both AES and AEF officers showed that they are clear on their assigned roles and responsibilities. Generally, the auditors found that the roles and responsibilities assumed by AES and AEF officers were aligned with what was defined in their respective work descriptions.

The Department has also established service standards for assisting clients. There are clear expectations for the services provided, which ensure that advice is given within a committed time frame.

2.1.4. Risks Management and Monitoring

Given the complex processes of the FSD administration and the involvement of more than 100 responsibility centres at missions and HQ, the audit team expected to see a risk-based work plan that ensures the tasks having the most significant impact on achieving the organization objectives are prioritized. As well, the auditors expected to be able to assess how the operational issues with the highest complexity and materiality to the organization were defined, managed and monitored. Interviews with AEF and AES staff showed that they are aware of certain risks associated with the administration of the FSDs as well as with the individual FSDs. However, these risks have not yet been formally identified, analyzed and integrated into AED’s decision-making processes.

The auditors noted that efforts to verify FSD expenditures were not aligned with the potential level of risk and the materiality to the Department. For example, interviews indicated that the FSD coordinator spends a disproportional amount of time reviewing low materiality education expenses for textbooks compared to the higher materiality tuition and school fees.

In the absence of risk-based FSD administration, the audit team expected that the verification of FSD expenditures performed by section 33 of the Financial Administration Act (FAA) would function as a compensation control in case section 34 of the FAA failed. The audit found that the review of section 33 was based on a higher level list of risks that had not been updated for years. The current high-risk payments are defined by the Payment Service Division within the Accounting Operations (SMFP) as a single transaction for relocation, vacation pay, schools and all advance payments over $50,000. SMFP performs no reviews, even on a random sampling basis, on expenditures outside of the high risk list. During the period under the audit review, high risk expenditures accounted for only 0.1% in the number of payment transactions and 5% of the total dollar amount of FSD expenditures. With this practice, along with the fact that current monitoring practices are not risk-based, there is a risk to the organization that FSD expenditures that were not appropriately authorized may not be detected.

The AEF monitoring function is resourced by three monitoring officers and headed by a manager. The audit team found that emphasis of the AEF monitoring group is currently placed on verifying and processing FSD payments rather than monitoring. The monitoring activities that do occur are limited to ensuring that the maximum of certain FSDs has not been exceeded and that expenses are coded to the correct General Ledger.

The auditors also found that errors and adjustments were not being monitored and analyzed. For example, rationale for the significant number of adjustments on the monthly allowances was not analyzed and actioned upon in order to minimize the risk of future occurrences.

In consequence, at strategic level, the audit found a risk-based monitoring plan has not been developed to target monitoring of high risk payments in an effort to minimize losses and maximize efficient utilization of monitoring staff resources. The FSDs that present potentially high risks to the Department are not regularly monitored. An excerpt of the testing results on FSDs requiring monitoring is presented in Appendix C.

Recommendation 1

The Assistant Deputy Minister, International Platform Branch, should develop, implement and monitor a formal FSD risk management framework which includes monitoring and reporting.

2.2. FSDs Compliance and Administration

The auditors expected to see measures in place to ensure compliance with the FSDs, and that employees and their dependants who are eligible for FSD benefits and entitlements receive correct amounts in a timely manner. These measures included: whether the FSD payments were appropriately approved by the delegated authorities with documented review and policy requirement assessment; if the internal controls over the calculation of the FSDs benefits were in place and functioning; and that FSDs were administered effectively and efficiently.

2.2.1. FSD payment approval

The Department updated its Delegation Instrument in November 2014. For the majority of FSD payments at HQ, authority for Section 34 is predominately exercised by the FSD client service advisors and AEF coordinators. In addition, AEF officers exercise restricted authority for shipment and storage of household effects. At missions, the MCOs, Head of Mission and other staff also exercise authority for section 34.

When reviewing the sample of FSD payments, the auditors expected to see that the approval of the payments was based on a documentation review and assessment that would allow the deputy head to determine the eligibility of the FSD expenditures claimed. The case study showed that 23 out of 69 cases had missing or insufficient supporting documents for the transactions under review. Statistical testing on three FSDs requiring invoices or other supporting documentation indicated that 27% of the payment approval files had non-existent or insufficient documented justification. The auditors, therefore, were unable to determine if these approved FSD expenses should have been paid or not.

Many FSDs contain provisions for exceptions or limitations that need to be considered on an individual basis by the Deputy Head. As per the Directives, there are three levels of discretionary approvals from none, to partial to full discretionary approval authority. According to the Department, FSD expenditures for the fiscal year 2013-2014, there were $8 million full discretionary FSD expenditures. The audit team was not able to quantify the total expenditures of FSDs requiring partial discretionary approving authorities because discretionary expenditures are not separately tracked and reported.

The audit team selected the following five FSDs requiring either full or partial managerial approval authority for detailed examination: FSD 15.13; FSD15.28; FSD25; FSD33 and FSD34.2. The review of these FSD expenditure claims required supporting documentation to determine if claims were reimbursable. Details of the examination work are presented in Appendix D. In the majority of files reviewed, the auditors did not find evidence that the applicable FSD policy requirements were fully reviewed and assessed.

Although overall policy and guidance for assisting the FSD application have been developed for FSD recipients, the auditors found that there is limited guidance or policy clarification for Deputy Heads with regard to the level of review and documentation required when approving discretionary FSD claims. Without adequate guidance, there is a risk that the FSD requirements may not be consistently assessed and documented.

Recommendation 2

The Assistant Deputy Minister, International Platform Branch, should ensure procedures and guidance relating to the performing and documentation of all FSD claims reviews are developed. The implementation of these procedures should be formally monitored.

2.2.2 Internal Controls over FSD Administration

During the audit examination period, 11 FSDs were added to the FSD Portal, including four monthly allowances that account for 71% of the total departmental FSD expenditures and 87% of the total FSD payment transactions. The FSD Portal requires a great amount of data input that is uploaded, entered and often updated from various sources and by different responsibility centres both at HQ and missions. Therefore, the reliability, accuracy and timeliness of the source information used directly affects the correct calculation of the FSD payments. Accordingly, the auditors reviewed the source information used in the FSD Portal as well as the associated internal controls.

Internal Controls over Source Information

The main information source of FSD data input is the Posting Confirmation Form (PCF), which is uploaded and used in the FSD Portal for calculating employee FSD allowances. Thus, an effective administration of the PCF is an essential control to ensure the information input is reliable and accurate. The auditor’s statistical testing, case studies and analyses revealed that information in the PCF is often incomplete. For example, the statistical sampling test showed that 26% of the PCFs issued to employees going abroad were not signed by the client service advisors, which is the evidence of the exercise of section 34 of the FAA. Of the ten employee case studies reviewed, it was revealed that eight employees did not have a PCF signed by the client service advisor for the correct posting period. Additionally, the statistical testing for FSD allowances showed that in 35% of sample cases the PCFs were signed for section 34 after the PCF was issued.

The Department uses the Amendment to PCF to reflect and confirm on-going changes affecting the monthly allowances and other FSD benefits. These changes include posting destination and duration, family configuration, dependants’ age, temporary absence, and so on. Changes, which are expected due to the nature of the posting process, take place over the course of the employee’s posting cycle. However, the information on how and when these changes are authorized and recorded in the system is not clearly defined or documented. This lack of controls over changing information may increase the risk of incorrect FSD payments or delayed adjustments.

Another area of risk identified by the auditors was the access controls to the FSD Portal. A total of 15 employees from AES and AEF as well as three systems staff were granted ‘super user’ access to the FSD Portal. This means that these users have had the same level of access to rates, adjustments, uploads, Human Resource Management System import, and daily and monthly payments to the Information Management System. The consequence of this comprehensive level of access is that a secondary review would be impossible in the system. Therefore, there is a risk that the access to the FSD portal may not be appropriately segregated and may compromise the integrity of the information.

Adjustments on FSD Allowances

The results of the FSD allowance sample testing showed that two thirds of allowance payments had errors and adjustments for a variety of reasons such as salary change, dependants’ arrival time change, cross posting, temporary absence from mission and hardship level change. The review of these adjustments shows that 78% originated from outdated information, which could have been avoided if the internal controls over source information had been stronger or more time sensitive.

Additionally, it was found that a formal secondary review was not performed for adjustments when posted in the FSD Portal and the Management Information System. None of the adjustments were subject to a post-payment verification and adjustments were made and posted by a designated officer only at the request of the FSD service client advisors. The statistical test on FSD allowances showed that two thirds of the examined cases had errors and adjustments. Further analysis on these adjustments revealed that 48% had no supporting documentation.

Recurring errors and adjustments require extra resources to be dedicated to making constant adjustments on a daily basis. This also means that employees may not receive the correct FSD benefit or receive the benefit on time. While recognizing that higher than normal error rate would be expected during the launch of the FSD Portal, it is essential that the causes of errors be analyzed and that the necessary controls over source information and adjustments are in place and operational.

Recommendation 3

The Assistant Deputy Minister, International Platform Branch, should lead a review to improve the controls over source information and implement measures to ensure that accurate and timely information is used in the calculation of the FSD benefits.

2.3 FSD Expenditures Forecasting, Fund Management and Budgeting

One of the audit focuses was to provide assurance that the FSDs are managed in a financially sustainable manner. The audit team reviewed and analyzed the forecasting and budgeting processes of the FSD expenditures.

In order to assess the reliability of the forecasted FSD expenditures, the auditors compared the projected FSD expenditures with the actuals for the past three fiscal years from 2012-2013 to 2014-2015, as reported in the Financial Information Status UpdateFootnote 8. The analysis showed that the differences between the forecasted and actual expenditures within each year have not been significant and gradually decreased over the three years under review. This indicates that the Department has improved the FSD forecasting practice for the past three years.

Despite the improvements in forecasting within each year, for the past three consecutive years, the Department incurred an FSD funding deficit. This means that the FSD expenditures exceeded budgeted FSDs. The auditors examined the processes on how the FSD funding level is calculated for the subsequent year, which is then used for the authorization of the FSD budget to the Department. More specifically, the auditors reviewed the submitted FSD funding estimates and the determining basis for the past three years (2012-2013 to 2014-2015). As a result, two major factors were identified that have contributed to the FSD structural deficit:

- The reduction of FSD funding level for 2012-2013 along with various other in-year funding reductions were disproportionate to the net change of the number of Canada Based Staff abroad. This set an insufficient opening budget in 2012-2013 and caused an on-going multi-year funding deficit.

- The calculation of the FSD incremental funding did not completely follow the formula defined in the agreement between the Department and TBS for the calculation adjustments for the annual reference level update and supplementary estimates (Quasi-statutory Framework).

Recommendation 4

The Chief Financial Officer should review the current FSD funding level estimation process to ensure the calculation of incremental funding fully reflects the principles defined in the Quasi-statutory Framework.

3. Conclusion

The management of FSDs is structured to support the day to day administration of the Directives and to ensure compliance with FSDs; however, formal risk management and risk-based monitoring were not evident to contribute to an informed decision-making process and an efficient administration. In addition, the following areas for improvement were identified as follows:

- Internal controls for FSD expenditure payments should be supported by sufficient documentation and consistent review;

- Controls over source information used for FSD benefit calculation should be strengthened to ensure compliance and more efficient administration; and

- FSD funding estimates and budgeting process should be reviewed.

Appendix A: About the audit

Audit Objective

The objective of the audit was to provide assurance that the Foreign Service Directives are managed in an efficient, effective and financially sustainable manner, are consistently applied and respect the guiding principles of comparability, incentive-management and program-related provisions.

Audit Scope

The scope of the audit included:

- FSD payments authorized at both HQ and missions from April 1 to December 31, 2014 for sample testing purposes;

- administration and management practices for the past 2-3 years;

- the FSD Portal information and data;

- financial forecasting information and trend analysis for the past 3-4 years; and

- examination of the following FSDs:

- FSD 55, 56, 58: Monthly Allowances

- FSD 34: Education at Mission

- FSD 50: Vacation Travel Assistance

- FSD 33: Lycée in Canada

- FSD 15.13: Shipment of Household Effects to Canada and Moving Expenses at Mission

- FSD 15.13.2: Shipment of Household Effects – Cross Posting

- FSD 15.28: House Hunting Trip

- FSD 25: Shelter Share

The audit examined information contained in the FSD Portal, some of which comes from other departmental information systems such as the Human Resources Management System and the Information Management System. However, the internal controls within these systems were not included in the audit scope.

Audit Criteria

The criteria were developed following the completion of a detailed risk assessment and considered the core management controls from the Audit Criteria related to the Management Accountability Framework, developed by the Office of the Comptroller General, Treasury Board Secretariat. The audit criteria were discussed and agreed upon with the auditees. The detailed criteria are presented as follows:

1.0 Governance and management frameworks are in place to oversee the application of FSDs so that:

- 1.1 Departmental guidance is in compliance with NJC Foreign Service Directives

- 1.2 Roles and responsibilities are defined and communicated

- 1.3 Risks associated with the application of the FSDs are identified, assessed, managed and monitored

- 1.4 FSD expenditures are appropriately forecasted, budgeted, monitored and reported

2.0 Procedures, systems and processes are established to ensure efficient and compliant administration of FSDs

3.0 Discretionary authorities are appropriately and consistently exercised.

Audit Approach and Methodology

The Audit of the Foreign Service Directives was conducted in accordance with Treasury Board Policy on Internal Audit, Directives, and the Internal Audit Standards for the Government of Canada and conforms to the International Standards for the Professional Practice of Internal Auditing of the Institute of Internal Auditors.

In order to conclude on the above criteria, and based on identified and assessed key risks and internal controls associated with the related business processes, the audit methodology included, but was not limited to, the following:

- designing flowcharts of FSD administration, payment and monitoring processes;

- identifying and reviewing relevant policies, guidelines, and legislation;

- analyzing financial and non-financial information;

- reviewing relevant documentation and a sample of files for transactional testing, case studies and analytical review; and

- conducting interviews and walkthroughs of FSD administration processes with DFATD staff and management.

The audit team determined and selected statistically valid sample of 138 FSD payment transactions for the detailed testing. The sample was selected based on a stratified random strategy with a 95% confidence interval and a precision of± 5%. The sample was randomly selected and representative of the defined population and sub population from which the testing results can be extrapolated and an overall opinion can be drawn. On a judgemental basis, the audit team also selected sample for analytical review.

The audit team worked in close coordination with the Internal Control group (SCM) in the area of FSD transactional testing. FSDs are one of the 12 business processes, of which the related key controls were identified and tested for both design and operating effectiveness by SCM. Given the testing performed by SCM was parallel with the timeframe of the internal audit of the FSDs, this coordination has minimized the disruption to the client and avoided duplicate effort by the two groups. Out of 138 transactions determined for statistical testing, the audit team tested only 54 transactions and used the test results for the remaining 84 transactions performed by SCM.

Appendix B: Audit scope in FSD expenditures

FSD Expenditures from April to December 2014 totaled $111 million, not including FSD 8 - Short Term Assignments and FSD 25 - Shelter Costs. The scope of the audit represents 66% ($73,066,062.41) of the total FSD expenditures for the period under review.

Text Alternative

Percentages of FSD Expenditures for the Audit Scope (April-December 2014)

15.13 Shipment and Storage of Houdehold Effects - 12.76%

15.28 House Hunting Trip - 0.47%

33 Education Assistance at Lycée in Canada - 1.54%

34.2 Elementary and Secondary education at Post - 14.28%

50 Vacation Travel Assistance - 9.62%

55 Post Living Allowance - 8.56%

56.2 Foreign Service Premium - 16.82%

58 Post Differential Allowance - 0.47%

15.13.2 Relocation Sipping Household Effects Cross Posting - 1.37%

Out of audit scope - 34.11%

Appendix C: Testing results—FSDS requiring monitoring

| FSD | Description | Finding | Risk to Organization |

|---|---|---|---|

| FSD 50 Vacation Travel Allowance | It is a tax-free allowance provided to employees and their families for vacation travel to visit Canada and/or take a vacation away from the post for each posting. One of the conditions of this allowance set by the Directives is that the employee should only spend it for the specific purpose identified by the employer. To this end, the employee is required to certify that the allowance has been used for the purpose intended and within time-limits. The employee is also required to retain evidence of travel to support the allowance for a period of seven years. | The audit team randomly selected 34 payment transactions from approximately 1000 FSD 50 transactions accounting for $10 million involving 1,000 employees for the period under review. The representative results of the test showed that 12% of the employees either could not provide required 75% of the receipts to demonstrate that the funds were spent for the purpose intended or did not certify the trip prior to the issuance of FSD 50 allowance for the subsequent trip. In addition, half of the employees did not submit their certification within the required timeframes. The testing results derived from SCM had also confirmed the audit finding. In one case representing 16.7% of the statistical sample, a recently retired employee had destroyed all receipts for the evidence of travel using FSD 50 allowance, which is not in compliance with the Directives. | There is a risk that the Department may not comply with the FSDs. |

| FSD 70 (Reporting Requirements and Verification of Allowances | The Deputy Head may request to verify the details of the use of the FSD 50 allowance. | The audit examination revealed that no verification or detailed review has been undertaken by AEF, even on a sample basis. This review would help to determine if the employee’s certification report is valid as to at least 75% of the FSD allowance was spent on intended travel. The AEF only performs a routine anomaly check on the FSD 50 allowance that is ready for payment in the Portal. | There is a risk that the employees may not use the travel allowance for intended purpose and the Department may not be aware of the situation |

| FSD 34 (Elementary and Secondary Education at the Post) | The Deputy Head may approve an allowance for admissible education expenses if the school is either on the approved representative school list or has submitted the exceptional cases to the Education Sub-committee and has it approved. | The audit analysis of selected 22 missions revealed that for nine missions, education fees were paid for schools that were neither on the representative school list nor approved by the working group B as required by the FSD 34 directive. These fees under review involved 51 payment transactions in 2014-2015, for a total of $272K. | There is a risk that missions may not be consistent in approving and referring cases to the Committee. |

Appendix D: FSD payments requiring descretionary authority

| FSD | Description | Audit Examination Results |

|---|---|---|

| FSD15.13-Shipment HHE on cross posting | In the review of a representative sample of, the auditors examined whether and how the Deputy Head determined if the claimed shipment weight was within the limitation defined in the FSDs. | Testing results showed that 54% of invoices did not have the weight information of shipment. Thus, the auditors questioned the basis on which these FSDs expenditures were approved. |

| FSD 15.28—House Hunting Trip (HHT) | This benefit may be authorized by the Deputy Head when an employee is notified of relocation to a new place of duty where Crown-held accommodation will not be available and can reasonably demonstrate that the proposed HHT is cost-effective. | Testing shows that 57% of the payment transactions were approved without supporting receipts and approved expense claim forms. In addition, no documented assessment was available indicating that the post being relocated to did not have an available Crown-held accommodation nor was there a reasonable demonstration that the proposed HHT would have been cost-effective as required by the FSD 15.28 directive. |

| FSD25 –Shelter Cost | The employee must pay for occupancy of Crown-held accommodation or where an employee is in receipt of shelter assistance. The Directives also articulate the shelter cost may be fully or partially waived with the approval of the Deputy Head under certain circumstances and within certain periods. | The audit team selected ten cases where employees’ shelter cost was waived for detailed review. The audit analysis revealed that 50% of the cases did not fully demonstrate that the shelter cost was waived in accordance with the FSDs policy requirements. |

| FSD33 - Education Assistance at Lycée in Canada | The managerial discretion of the Deputy Head may be exercised when the application is extended beyond the two-year period if the rotational status is confirmed and as a result of operational requirements. | The audit analysis showed that 7 out of 10 selected cases where the employees had been paid for more than three years with school fees had no letter confirming employee’s rotational status. Out of the 10 cases, only one case had a letter where operational needs were confirmed. Therefore, the auditors were not able to determine if these expenditures would be admissible pursuant to the FSD policy requirements. |

Appendix E: Management action plan

| Audit Recommendation | Management Action | Area Responsible | Expected Completion Date |

|---|---|---|---|

| 1. The Assistant Deputy Minister, International Platform Branch, should develop, implement and monitor a formal FSD risk management framework which includes monitoring and reporting. | The Assistant Deputy Minister, International Platform Branch (ACM) agrees with the recommendation. The FSD Bureau (AED) will work with the Corporate planning, Performance and Risk Management Bureau (SRD) to put in place a formal FSD risk management framework which will includes monitoring and reporting. This action item will be achieved in two phases, the development phase and the implementation phase. | AED, SRD | Development phase: October 1-December 31st, 2015. Implementation phase: January 1st to December 31st, 2016 |

| 2. The Assistant Deputy Minister, International Platform Branch, should ensure procedures and guidance relating to the performing and documentation of all FSD claims reviews are developed. The implementation of these procedures should be formally monitored. | ACM agrees with the recommendation and will ensure that procedures relating to FSD claims are developed, monitored and communicated as required by including in current tools and resources such as the FSD Desk book, pre-posting training for outgoing Heads of Mission and Management Consular Officers, via broadcast message and by including on the AED Intranet site. AED is reviewing each mission delegated FSD as part of the development of the Portal to ensure that the appropriate authority has clearly defined roles and responsibilities. A monitoring framework to ensure that procedures are followed will be developed. | AED, AEF, AES | March 31st, 2016 |

| 3. The Assistant Deputy Minister, International Platform Branch, should lead a review to improve the controls over source information and implement measures to ensure that accurate and timely information is used in the calculation of the FSD benefits. | ACM agrees with the recommendation and notes that work on this area has already begun. ACM will ensure that the controls are strengthened to ensure that the base information on rates is accurate by clarifying procedures, ensuring a pre-determined rhythm of verifications based on risk factors and addressing system issues in a timely manner. It is important to note, however, that not all sources of information, both from timeliness and accuracy perspectives, are within the control of ACM, ie, the management of the pay system, the finalization of Posting Confirmation Forms, etc. This often leads to errors or delays that are unavoidable however ACM will continue to work with the owners of this information or these systems to improve performance. | AED, AEF | June 30th, 2016 |

| 4. The Chief Financial Officer should review the current FSD funding level estimation process to ensure the calculation of incremental funding fully reflects the principles defined in the Quasi-statutory Framework. | The CFO branch has reviewed the current funding methodology to ensure that it meets the principles defined in the Quasi-Statutory Framework. However, as the current Quasi-Statutory Framework does not adequately align funding to expenditures, the CFO branch opened discussions with TBS in September 2015 regarding the need to modify the existing Quasi-Statutory Framework. The objective is to obtain agreement from TBS regarding proposed changes by June 2016. This will allow DFATD to include new funding methodology in Supplementary Estimates A/B (FY 2016-17). | SWD | July 2016 |