Archived information

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Audit of Canada-Based Staff Overtime

Final Report

June 2015

Table of Contents

Executive Summary

Background

An Audit of the Management of Leave and Overtime for Canada-Based Staff (CBS) was approved as part of the Department of Foreign Affairs and International Trade (DFAIT) Risk-Based Audit Plan 2013-2016. During the planning phase for the audit, the management of leave was scoped out. While the management of leave represents potential risks, the size and complexity of this subject warrants a separate audit which will be considered in the context of future risk-based audit planning. This audit commenced prior to the amalgamation with the Canadian International Development Agency and therefore, the audit scope includes only the former DFAIT.

Overtime is authorized time worked by a person in excess of the standard daily or weekly hours of work. Overtime can be compensated by cash payment or by compensatory time-off at a premium rate; the specific rate and terms are detailed in the various collective agreements. In 2011-2012 approximately 70 percent of the total value of overtime was compensated as payment and 30 percent as compensatory time-off.

Overtime compensation is governed by:

- Financial Administration Act;

- Public Service Employment Act;

- Collective agreements;

- Treasury Board policy and directive on the terms and conditions of employment; and

- Departmental delegations of financial and human resources authorities.

The Human Resource Branch is responsible for the overall administration of pay and the integrity of the process; however, accountabilities and operational structures are changing. The Consolidation of Pay Services Project was announced by the government in 2012 to increase the effectiveness of public service compensation operations. Pay administration services are gradually being transferred from the Department to the Public Works and Government Services Canada (PWGSC) Center of Expertise in Miramichi, New Brunswick. The transfer is to be complete by 2015-2016.

Why is this important?

When managed appropriately, overtime is an important tool that can help managers balance salary budgets with operational pressures and maximize employee satisfaction and workplace well-being. As such, overtime can be considered an indicator of management efficiency. As of March 31, 2013, the former DFAIT had a workforce of 4,644 CBS; this includes non-rotational, mobile, and rotational employees that could be posted at headquarters, in missions abroad or in regional offices. While overtime expenditures have steadily declined over the past three years, they remain a significant expenditure for DFAIT. In 2012-2013, CBS were paid $13.9M in overtime and credited over 19,000 days of compensatory-time off (estimated value of $6M). Effective management controls are required to support sound stewardship over these significant financial and human resources.

What did we examine?

The objective of this audit was to assess Departmental controls and practices established for managing overtime for CBS of the former DFAIT. Specifically, the audit was designed to assess whether:

- DFAIT had designed and implemented an appropriate accountability structure, responsibilities, policy and guidance to support effective CBS overtime management practices;

- Controls and management practices were in place to ensure that CBS overtime is planned and controlled to support effective resource management;

- Controls were effective to ensure the Department is in compliance with applicable collective agreements, policies and directives; and

- Management was supported in carrying-out their monitoring and oversight responsibilities through the development and implementation of standardized tools and systems.

What did we find?

There is a need to strengthen oversight over the management of overtime for the Department and improve the effectiveness of internal controls over the processing of individual transactions.

Specifically, the audit observed:

- Accountabilities, roles and responsibilities are adequately defined: The Departmental delegations of human resources and financial authorities and the various Treasury Board policies and directives, provide an acceptable foundation for Departmental managers, employees and human resource specialists to have a clear understanding of accountabilities, roles and responsibilities.

- Budgetary control is not sufficient to ensure effective use against Departmental priorities: There is no consistent Departmental allocation of overtime budgets as it is at the discretion of the Assistant Deputy Ministers of the Branches. Not all fund centers, therefore, have a budget for overtime. As a result, there is no baseline established for in-year monitoring and reporting against the budget. Overtime compensated in cash is reported in the Departmental Financial System. Information related to overtime claimed as Compensatory Time-Off is reported through the Human Resources Management System (HRMS) but is not budgeted, monitored and reported in the Departmental FINSTAT. Consequently, there is no one source of information to provide senior management with important information regarding the overall cost of overtime in the Department and trends related to usage.

- Compensatory time-off is not being approved and monitored effectively: Managers are approving a greater amount of compensatory time-off than can reasonably be used within the time frames prescribed by collective agreements. This creates challenges in managing resources amongst different fund centres. Importantly, at the Departmental level, there is approximately $2M of annual cash-out of accumulated leave credits and that liability is not being actively monitored through financial reporting.

- Management approval of overtime claims contained a significant degree of error but with minimal materiality: The audit team stratified overtime claims into key risk areas and selected a random sample of 90 overtime transactions. Documentation was not available for 17 transactions resulting in auditors reviewing 73 transactions. The audit tested overtime transactions for compliance with Collective Agreements and found an error rate of 6 percent. The audit also tested for compliance to the Financial Administration Act and found an error rate of 40 percent. In all cases, the financial materiality of these errors was minimal.

- Service Standards for the timely processing of claims were not always met: 54 percent of transactions met the established service standards for processing time. 12 percent did not meet the standard and an additional 34 percent could not be tested due to lack of documentation.

Key Recommendations

- The Chief Financial Officer, in collaboration with the Assistant Deputy Minister, Human Resources, should put in place a process whereby overtime expenditures are reported and monitored, including compensatory time-off, at the Branch level.

- The Assistant Deputy Minister, Human Resources Branch, should determine the types of information, reports and trend analysis that would be useful for senior management decision-making and produce them on a regular basis.

- The Assistant Deputy Minister, Human Resources Branch, in collaboration with the Chief Financial Officer, should improve Departmental practices for approving compensatory time-off. The compensatory time-off liability should be monitored and actively managed, especially for rotational employees.

- The Assistant Deputy Minister, Human Resources Branch, should perform an in-depth review of high overtime users to determine if the overtime was warranted and if corrective measures should be taken.

- The Assistant Deputy Minister, Human Resources Branch, should ensure that compensation advisors:

- Verify that Section 32 and Section 34 are signed by a delegated authority prior to completing the processing of overtime claims; and,

- Enter data into the system corresponding to the month of the overtime form.

- The Assistant Deputy Minister, Human Resources Branch, should put in place a process to track errors in overtime claims and communicate errors to managers.

- The Assistant Deputy Minister, Human Resources Branch, should implement effective records management practices to ensure that documentation is kept to support the reconstruction of overtime transactions.

Management agrees with these observations and recommendations and has developed a Management Action Plan (Appendix B) to address the issues raised in this report.

Conclusion

There are management controls in place for processing individual overtime transactions. Improvements are suggested to the effectiveness of controls for individual transactions which could positively impact the compliance rate. At the departmental level, there are opportunities for strengthening oversight that would result in better information about overtime usage within the Department and enable proper stewardship and resource management.

Statement of Conformance

In my professional judgment as the Chief Audit Executive, this audit was conducted in conformance with the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing and with the Internal Auditing Standards for the Government of Canada, as supported by the results of the quality assurance and improvement program. Sufficient and appropriate audit procedures were conducted, and evidence gathered, to support the accuracy of the findings and conclusion in this report, and to provide an audit level of assurance. The findings and conclusion are based on a comparison of the conditions, as they existed at the time, against pre-established audit criteria that were agreed upon with management and are only applicable to the entity examined and for the scope and time period covered by the audit.

Jean Goulet

Chief Audit Executive

1.0 Background

Management of overtime is governed by the Public Service Employment Act, the Financial Administration Act, and a series of Treasury Board policies. Overtime can be compensated either by cash or by compensatory time-off in the form of leave credits. The terms and rates governing overtime compensation, for work performed outside of an employee's regular hours of work at the employer's request, are detailed in various collective agreements. The Department of Foreign Affairs and International Trade (DFAIT) has not put in place any additional policies, however there is a guideline on overtime in the context of a crisis.

The Department makes considerable use of overtime as a form of compensation.

While overtime has declined over the past three years it still represents a significant expense. In 2011-2012 and 2012-2013, approximately 60 percent of the total CBS workforce received overtime compensation each year. The volume of transactions is large – in 2012-2013, there were 21,037 transactions for compensatory time-off and 25,178 for cash payments.

| 2010-2011 | 2011-2012 | 2012-2013 | |

|---|---|---|---|

| Net Overtime Expenditures | $20,793,586 | $16,245,824 | $13,896,989 |

| Compensatory Leave Credits Earned (days) | 24,419 | 22,654 | 19,228 |

| Estimated Value of Compensatory Leave* | $7,325,700 | $6,970,462 | $6,064,215 |

| Estimated Value of Overtime Compensation (cash overtime payments – accumulated compensatory time paid + estimated value of compensatory leave) | $26,609,841 | $21,590,472 | $18,662,834 |

| CBS Salary and Wages Expenditures (minus EX salary and performance pay) | $351,650,472 | $337,107,039 | $327,265,060 |

| Estimated Overtime Compensation as a Percent of Salary and Wages | 7.7% | 6.4% | 5.7% |

Source of data: Salary Forecasting Tool, Financial Situation Reports and Human Resources Management System.

* Based on an assumption of an average salary of $78,000 for 2010-2011, $80,000 for 2011-2012 and $82,000 for 2012-2013.

2.0 Observations and Recommendations

2.1 Accountabilities and Responsibilities

Accountabilities and responsibilities are clearly outlined.

Manager accountabilities and responsibilities are clearly outlined in the:

- Human Resources Instrument of Sub-Delegation of Authorities which specifies that managers at the director level or equivalent can approve overtime.

- Financial Administration Act which requires delegated authorities to certify Section 32 to ensure sufficient availability of funds before initiating expenditure and then, provides for the commitment of that expenditure initiation as well as Section 34 which certifies that the goods or services have been fully delivered before payment is made.

- Treasury Board Directive on Terms and Conditions of Employment which outlines that the person with delegated authority is responsible for requiring the employee to work overtime; it is specific that the employee must not control the duration of the overtime worked.

The Treasury Board Circular 1977-37: Pay Administration assigns departments the responsibility for pay administration and the integrity of the overall pay process, which includes overtime. At the Department of Foreign Affairs and International Trade (DFAIT), the Human Resource Branch is responsible for the overall administration of pay. Within the Human Resources Branch, the Human Resources Operations Division includes: Labour Relations (responsible for interpretation of collective agreements) and Compensation Services (responsible for processing overtime claims).

Compensation advisors review the overtime forms for completeness and enter requests either in the Regional Pay System (the Government of Canada pay system) for overtime requested as cash payment or in the Human Resources Management System for compensatory time-off. A second compensation advisor also performs a peer-review of transactions.

The Human Resource Branch is responsible for the overall administration of pay and the integrity of the process; however, accountabilities and operational structures are changing. The Consolidation of Pay Services Project was announced by the Government in 2012 to increase the effectiveness of public service compensation operations. Pay administration services are gradually being transferred from the Department to the Public Works and Government Services Canada (PWGSC) Center of Expertise in Miramichi, New Brunswick. The transfer is to be complete by 2015-2016.

Despite this foundation for the understanding of accountabilities, there were issues noted with respect to their application as outlined in the following sections.

2.2 Budgetary Control: Planning and Monitoring

To exercise sound stewardship over salary budgets, fund center managers are expected to plan overtime based on their needs. These budgets should be monitored, adjusted when necessary and results reported to ensure that overtime budgets are not exceeded.

Overtime is not systematically and formally budgeted for all Fund Centers.

Total salary budgets are allocated to branches. Branches then allocate salary budgets to fund centres, and it is up to branch discretion to make a specific allocation for overtime within the salary envelope.

The planning practices of ten divisions (six at headquarters and four at missions) were reviewed to determine if overtime budgets had been allocated to their 36 fund centers. In 2011-2012, only one headquarters division and one mission had established overtime budgets at this level. While this increased slightly in 2012-2013, the majority of fund centres either had no formal overtime budgets, did not provide documentation to the audit team or budgeted for overtime only at a higher organizational level.

Fund center managers that had planned overtime expenditures indicated that estimates and actual expenditures from prior years were used to establish forecasts. This was done in collaboration with Financial Management Advisors and Bureau Management Offices. Managers also stated that it can be difficult to forecast workload due to extraordinary events such as ministerial events, official visits or international crisis. This reinforces the need for in-year monitoring.

Due to the lack of systematic allocation of overtime budgets at the fund centre level, some fund center managers indicated that they did not know whether they had sufficient funds for overtime to be worked prior to approving the overtime. In other divisions where overtime budgets were established based on historical averages, managers did not feel accountable for the established budgets as they were known at the outset to not be sufficient.

Monthly Departmental financial monitoring excludes compensatory time-off.

There is a monthly assessment of the Departmental financial position, entitled FINSTAT (financial status report). This includes: budgets, expenditures, commitments, free balance, and financial indicators such as the resource "burn rate." FINSTAT reports are established at the fund center level (the lowest level of delegation of financial authority), and aggregated at the bureau, branch and corporate levels. Financial management advisors support fund center managers throughout this process.

Overtime taken as compensatory time-off is not reported in FINSTAT, which only includes expenditure information. Compensatory time-off is recorded in the Human Resources Management System as a leave credit. As a result, FINSTAT provides only partial information on overtime and it does not include the cash-value of accumulated compensatory time-off.

Recommendation:

1. The Chief Financial Officer, in collaboration with the Assistant Deputy Minister, Human Resources, should put in place a process whereby overtime expenditures are reported and monitored, including compensatory time-off, at the Branch level.

Management Response: The Chief Financial Officer agrees with this recommendation and has included their detailed response in the Management Action Plan (Appendix B).

There is no systematic monitoring of Departmental overtime or reporting on trends.

There was limited ad hoc monitoring of overtime at various levels in the Department; however, it was not systematic and results were not comparable across the organization. For example, in June 2014 the Chief Financial Officer presented an overview of financial trends to the Departmental Executive Board; it included aggregate overtime expenditures and excluded compensatory time-off. As such, there is a missed opportunity to take corrective action, where required, on emerging Departmental overtime trends.

The audit team assessed available financial and human resources data to illustrate the type of information which could be brought to senior management attention. This information could include:

- the distribution of overtime compensation;

- identification of high overtime users (those that exceed departmental threshold) and the managers signing off on the overtime;

- fund centres with higher overtime expenditures than departmental average;

- amount of compensatory time paid out at cut-off period;

- the comparison of total compensation packages of top overtime users to the executive salary scale; and,

- in-depth analysis of fund centres/missions with high overtime usage.

This information should be based upon an historical perspective of trends. It will have to be undertaken on a periodic basis to provide senior management with a complete understanding of overtime in the Department.

A small portion of employees consumed a significant percentage of overtime compensation.

In 2011-2012, 1.4 percent of employees received $1.4 million in overtime payments which accounted for over 12 percent of total overtime cash payments in that year. In 2012-2013, there were 1.5 percent employees who received over $1.2 million in overtime payments, which accounted for over 12 percent of total overtime cash payments during that year. This data indicates that it is not a widespread issue across the department – there is a small population of employees on the first two lines of the table below that make use of a significant amount of overtime in comparison to their peers.

| Overtime Cash Payment ($000) | 2011-2012 Overtime Cash Payment ($) | 2012-2013 Overtime Cash Payment ($) | ||||||

|---|---|---|---|---|---|---|---|---|

| # of CBS | % of CBS | Total Cash Payment | % of Total Cash Payment | # of CBS | % of CBS | Total Cash Payment | % of Total Cash Payment | |

| 50K ~ 82K | 7 | 0.30 | $ 405,069 | 3.52 | 4 | 0.20 | $296,897 | 2.94 |

| 30K ~ 50K | 28 | 1.18 | $1,023,406 | 8.89 | 27 | 1.33 | $963,729 | 9.55 |

| 10K ~ 30K | 309 | 13.04 | $4,883,163 | 42.43 | 267 | 13.11 | $4,216,611 | 41.79 |

| 1K ~ 10K | 1,264 | 53.33 | $4,963,173 | 43.13 | 1,091 | 53.56 | $4,385,768 | 43.46 |

| < 1K | 762 | 32.15 | $292,838 | 2.54 | 648 | 31.81 | $252,659 | 2.50 |

| Adjustments | 0 | 0 | -$60,086 | -0.52 | 0 | 0 | -$25,007 | -0.25 |

| Total | 2,370 | 100 | 11,507,563 | 100 | 2,037 | 100 | 10,090,657 | 100 |

Source of data: Salary Forecasting Tool. Cash payments exclude year-end accruals.

There was a similar trend for usage of compensatory time-off. In 2011-2012, the top 43 overtime users claimed 14 percent of the total compensatory time-off during that year, or 3,171 out of 22,654 days in total. Each of these employees earned between 10 and 34 weeks. In 2012-2013, the top 35 overtime users claimed 14 percent of the total compensatory time-off during that year which equated to 2,609 days in total (average of 15 weeks of compensatory leave for each of the top 35 employees).

As a result of high overtime compensation, some employees are receiving payments comparable to executives.

The total salary and wages of the top ten users of overtime (overtime payments plus estimated cash equivalent of compensatory time-off earned) were comparable to the executive (EX) salary scale. Executives at the EX-01 level are usually in Director positions; EX-02-03, Directors General; and EX-04-05, Assistant Deputy Ministers. The data indicates that 19 of the top 20 overtime users (both paid and compensatory time off) earned more than EX-01s – the majority earned a salaries equivalent to the EX-02 and EX-03 salary range.

There is a risk that overtime compensation is not limited to addressing operational pressures related to departmental priorities, temporary work increases and urgent requests.

The audit team selected four missions for review based on the number of top overtime users and the mission ranking for total spending on overtime. The high level of overtime for three of these missions appeared reasonable to the auditors based upon extraordinary events, military presence, disaster recovery and the importance of their relationship with Canada. In the opinion of the auditors, however, there was no apparent justification for the high level of overtime in one of the four missions.

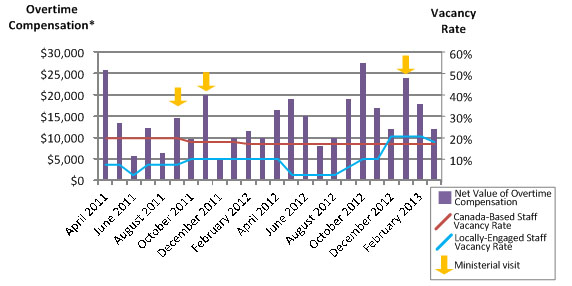

Management indicated that overtime usage was high due to ministerial visits, vacant positions, and trade priorities. Based on those explanations, a correlation between factors would be expected (the purple bars should follow the same pattern as the red and blue lines); however, that was not the case. As illustrated below, with the exception of two Ministerial visits, there is no correlation between the special circumstances and overtime.

This limited analysis does not permit the auditors to definitively conclude that this high degree of overtime was not warranted. This analysis was not conducted to single out a particular mission; rather, to demonstrate the type of analysis possible based upon available data that could provide useful information to senior management.

Graphic: Overtime Compensation for a Specific Mission, Vacancy Rate and Ministerial Visits

Source of Data: Human Resources Management System and Salary Forecasting Tool

*Net overtime cash payments and estimated value of compensatory time-off. Note that no payment information was available for November 2012 to March 2013.

Text Alternative

The graphic depicts the total amounts of overtime compensation per month (comprised of the net overtime cash payments and the estimated value of compensatory time-off) between April 2011 and February 2013. These amounts varied from approximately $5,000 to $27,000 during this period. Note that no payment information was available for November 2012 to March 2013.

The graphic shows a stable Canada-Based Staff vacancy rate of approximately 20% from April 2011 to February 2013. The vacancy rate for Locally-Engaged Staff, however, varied between 0 and 20% during that same period.

There were ministerial visits during the months of September 2011, November 2011 and January 2013.

The source of data is the Human Resources Management System and the Salary Forecasting Tool.

Recommendation:

2. The Assistant Deputy Minister, Human Resources Branch, should determine the types of information, reports and trend analysis that would be useful for senior management decision-making and produce them on a regular basis.

Management Response: Management agrees with this recommendation and has included their detailed response in the Management Action Plan (Appendix B).

2.3 Managing Compensatory Time-off

As per the collective agreements, overtime shall be compensated in cash, except that, upon request of an employee and with the approval of the employer, overtime can be compensated in equivalent leave with pay. In 2011-2012 and 2012-2013, 30 percent of total overtime compensation was granted as compensatory time-off and 70 percent as cash payment.

Collective agreements also stipulate that compensatory time-off earned in a fiscal year, if not used within a 12 month period or at certain date within the following fiscal year, should be paid at the employee hourly rate at the time of payment.

Compensatory time-off, if managed appropriately, could be used as a powerful tool for managers to manage their budgets and balance their resource capacity with operational needs.

Compensatory time-off provides flexibility to both managers and employees to balance workload, budgets and workplace well-being. Managers are not always considering operational requirements when approving compensatory time-off. Interviews with managers indicated that compensation for overtime was often granted based upon employee preferences. Many managers were unaware of the stipulations in the collective agreements that they could determine the method of compensation based on operational requirements. Some managers also expressed that they did not want to deny employee preferences. As a result, managers may not have considered operational needs when approving overtime or the ability to take compensatory leave within the timeframe prescribed within the collective agreements.

A greater amount of compensatory time-off was approved than could feasibly be used within the prescribed timeframe.

At the Departmental level for 2011-2012 and 2012-2013, approximately 60 percent of the approved compensatory time-off was actually taken as leave. The remaining 40 percent was converted to cash payments which may not have been forecasted in the departmental financial system. This issue is important at the fund center level where the impact of having high users of compensatory time-off can be significant.

The data included in the Human Resources Management System for 2011-2012 indicates that far more compensatory time-off was approved than could reasonably be used within the prescribed timeframe. As a result, compensatory leave credits were paid out to employees at an average rate of 73 percent.

The payout of compensatory leave credits results in a financial liability which is not monitored through the monthly FINSTAT reports.

Accumulated compensatory time-off represents a potential financial liability as managers have the obligation to pay for any compensatory time-off not used within the prescribed timeframes. Interviews with managers indicated that very few monitored their fund centers' accumulated compensatory time-off on a regular basis. With the current approach, compensatory time-off can easily bypass financial monitoring until late in the fiscal year. For one fund center reviewed, a year end compensatory time-off liability was so large that it could not be covered. As a result, the Business Management Officer had to transfer funds from another fund center. Given the amount of the compensatory time-off liability for the Department – estimated at $2M per year – this could create a financial risk for the Department.

The impact of accumulating a compensatory time-off liability is two-fold. At the financial level, albeit minor, accumulated compensatory time-off is paid at a higher hourly rate due to incremental wage increases since the overtime was originally performed. Additionally, the cash-out of accumulated compensatory time-off is an administrative burden for business management officers and compensation advisors who have to create payments at year-end (PAYE).

The rotational nature of the CBS workforce reinforces the need for sound management of compensatory time-off.

The impact of the compensatory time-off liability is exacerbated due to the fact that 48 percent of CBS are in rotational positions. Often employees accumulate compensatory time-off while working for one fund center and carry this liability forward with them to a new fund center when changing assignments. The new manager, therefore, inherits either a budget shortfall if they pay out the compensatory time-off, or a resource shortage if the employee takes the time off that they have earned. In some cases, funds may be recovered from the previous fund center which, again, adds to the administrative burden.

Recommendations:

3. The Assistant Deputy Minister, Human Resources Branch, in collaboration with the Chief Financial Officer, should improve Departmental practices for approving compensatory time-off. The compensatory time-off liability should be monitored and actively managed, especially for rotational employees.

4. The Assistant Deputy Minister, Human Resources Branch, should perform an in-depth review of high overtime users to determine if the overtime was warranted and if corrective measures should be taken.

Management Response: Management agrees with these recommendations and has included their detailed response in the Management Action Plan (Appendix B).

2.4 Processing Overtime Transactions

To provide assurance that overtime transactions were processed in compliance with collective agreements and the Financial Administration Act, a random sample of transactions was selected for review. The total population was stratified to cover each type of overtime worked (e.g. stand by, call-back) and placed emphasis on areas of higher risk such as overtime related to travel.

Employees, managers and compensation advisors are involved in the processing of transactions.

- Employees are responsible for completing and signing an Overtime Authorization and Payment Report.

- Delegated managers are responsible for pre-approving the overtime, signing off on Section 32 and Section 34.

- Compensation Advisors are responsible for conducting a Quality Assurance review of the authorized payment forms, making any necessary corrections and entering the information into the appropriate departmental system.

Transactions were not always processed in accordance with the applicable collective agreements, the Financial Administration Act and the Departmental Accounts Verification Policy.

Collective Agreements

To provide assurance that collective agreements were applied correctly, a sample of transactions was reviewed. There is an inherent level of complexity with processing of overtime claims due to CBS being represented by seven different collective agreements. The rules vary from one collective agreement to another; managers and compensation advisors are expected to interpret a number of overtime articles.

Given this complexity, it is not surprising that there were numerous errors on overtime forms submitted to compensation advisors which had been certified by managers under Section 34. Compensation advisors corrected the majority of those errors; however, auditors found a 6 percent rate of errors that were not caught during the Quality Assurance review. Table 3 highlights the type of errors. In all cases, the financial materiality of these errors was minimal. According to the Departmental Account Verification Policy, when errors are discovered through quality assurance review, documents must be returned to the originating party for corrective action. Changes were made to the forms by compensation advisors, however, without notifying the delegated manager. While the intent was likely to be helpful and speed up the process, sometimes there can be circumstances and a rationale for approving a specific rate for which only the manager would be aware.

Table 3: Summary of Audit Results – Collective Agreements

Summary of Errors

- Overtime forms signed by managers containing errors which were corrected by compensation advisors (Error Rate: 60%)

- Additional transactions containing errors identified by auditors (Error Rate: 6%)

Error Types (two transactions included multiple errors)

- Claimed more than one form of overtime for same hours (Error Rate: 1%)

- Incorrect calculation of hours (Error Rate: 3%)

- Incorrect rate of overtime (Error Rate: 3%)

- Data entry error (Error Rate: 1%)

Financial Administration Act

Section 32 of the Financial Administration Act provides the authority to initiate expenditures and to commit funds before expenditures are incurred. For overtime, this means that the manager with delegated authorities has required the person to work overtime and there are funds available. Approval under Section 34 of the Financial Administration Act is to ensure that work has been performed prior to making a payment. For overtime, this means that the manager with delegated authority certifies that: the overtime reported was accurate; pre-approved; and, that the employee did not control the duration of overtime. Managers who sign overtime claims must have delegated financial authority for the fund center at the time of the transaction as evidenced by the specimen signature card. The transaction review yielded an error rate of over one third of transactions for Financial Administration Act Sections 32 and 34. The types of errors are outlined below.

| Summary of Errors | Error Rates | |

|---|---|---|

| Section 32 | Section 34 | |

| Fund centre on Specimen Signature Card did not match fund centre of overtime transaction | 29% | 23% |

| Manager did not type out name legibly, could not validate | 7% | 4% |

| Date on Specimen Signature Card did not match date of overtime transaction | 1% | 4% |

| Specimen Signature Card not provided | 1% | 1% |

| Incomplete file | 1% | 1% |

| Total Errors | 39% | 34% |

Compensation advisors peer-review each other's transactions; however, the effectiveness of the process could be improved. Auditors found a 6 percent error rate for compliance to collective agreements and an error rate of over one third for compliance with the Financial Administration Act.

Departmental Accounts Verification Policy

The Departmental Account Verification Policy states that Compensation Services are to verify the signatures on overtime forms in advance of any payment, however the audit found that Compensation advisors were not validating delegated authority against specimen signature cards. This same issue was raised on a previous audit which was reported in May 2013 – the expected completion date for corrective action was September 2013. Given the rotational nature of Departmental managers and reduced staff in the compensation unit, it is difficult to keep track of manager delegations. A systematic verification of delegated authority prior to entering overtime transactions would help ensure compliance with the requirements of the Financial Administration Act.

The audit also found that errors in the exercise of Section 34 were not tracked. As a result, the Department is missing an important source of information to develop guidance and training for employees and managers on overtime. As per the Departmental Account Verification Policy, when errors are frequent and serious, a review of accounting practices may be carried out for corrective action. Without tracking of errors in overtime claims or approvals, the Department is missing the mechanism through which the requirements for further review would be identified.

The quality of data jeopardizes the Department's ability to produce meaningful information.

Employees are required to report on overtime monthly; however, transaction records are often 'bundled' by compensation advisors to reduce data entry requirements. While this does not affect the amount of the overtime payment, it limits the usefulness of overtime data for workforce or operational analysis as information is not available on a monthly basis. In 2011-2012 and 2012-2013, 10 percent of transactions had a date range spanning more than one month. As a result, there is no way to know when the overtime was performed without consulting individual overtime forms.

Interestingly, during our analysis we noted that 33 percent of overtime transactions paid in 2011-2012 and 2012-2013 were for overtime worked in previous years going back to 2001. Management may want to look into this issue further.

Recommendations:

5. The Assistant Deputy Minister, Human Resources Branch, should ensure that compensation advisors:

- Verify that Section 32 and Section 34 are signed by a delegated authority prior to completing the processing of overtime claims; and,

- Enter data into the system corresponding to the month of the overtime form.

6. The Assistant Deputy Minister, Human Resources Branch, should put in place a process to track errors in overtime claims and communicate errors to managers.

Management Response: Management agrees with these recommendations and has included their detailed response in the Management Action Plan (Appendix B).

Established service standard for processing time were not always met.

Service standards were established by the Human Resources Branch in 2009. These standards include 30 days for processing payment requests once received by compensation advisors and 15 days for processing compensatory time-off requests. Compensation services met this standard 62 percent of the time. They did not meet the standard in 14 percent of the cases – a further 24 percent could not be measured due to missing date stamps or systems data. For the transactions where the service standards were not met, the average processing time for compensatory time-off was 53 days, and for cash payments it was 47 days.

Records management within the compensation unit was not sufficient to permit full testing of selected files.

There was no documentation provided by the Compensation Unit to support the payment or leave credits provided to employees for 17 of the 90 overtime transactions requested for the review.

Recommendation:

7. The Assistant Deputy Minister, Human Resources Branch, should implement effective records management practices to ensure that documentation is kept to support the reconstruction of overtime transactions.

Management Response: Management agrees with this recommendation and has included their detailed response in the Management Action Plan (Appendix B).

3.0 Conclusion

There are management controls in place for processing individual overtime transactions of Canada-Based Staff of the former Department of Foreign Affairs and International Trade; however, they are not operating effectively. Improvements were suggested regarding the: validation of authority for approving claims; tracking errors; records management; and data quality.

Regarding the broader management of overtime at the Departmental level, the audit found there were few controls in place. There is an opportunity to implement oversight and management measures such as establishing budgets, systematic monitoring and reporting. This will result in greater information about overtime usage and enable proper stewardship and resource management. This will also position the Department to identify issues, such as the management of the compensatory time-off liability and take appropriate action on a continuous basis.

There is a formal delegation of human resources and financial authorities, a clear understanding of responsibilities and established practices for compensation advisors, employees and managers. This will serve as the foundation to implement the recommendations in this audit report.

Appendix A: About the audit

Objective

The objective of the audit was to assess Departmental controls and practices established for managing overtime for Canada-Based Staff (CBS) of the former Department of Foreign Affairs and International Trade (DFAIT). Specifically, the audit assessed whether:

- DFAIT had designed and implemented an effective management framework (accountability, roles and responsibilities, policy and guidance) to support effective CBS overtime management practices;

- Controls and management practices were in place to ensure that CBS overtime was planned and controlled to support effective resource management;

- Controls were effective to ensure the Department was in compliance with applicable collective agreements, policies and directives; and,

- Management was supported in carrying-out their monitoring and oversight responsibilities through the development and the implementation of standardized tools and systems.

Criteria

The selected criteria for the examination phase have been derived, with some adjustments, as per the elements of the draft document Core Management Controls. These controls have been developed by the Office of the Comptroller General. They relate to the Management Accountability Framework and aim to fully respond to the engagement objectives and scope.

Audit Criteria and Related Core Management Controls

Audit Criterion 1

1. DFAIT has designed and implemented effective controls to govern overtime management within the Department.

1.1 Accountabilities, roles and responsibilities for overtime management are clearly defined and communicated.

1.2 Guidelines, procedures and appropriate training have been developed, implemented and communicated to govern and manage overtime.

Related Core Management Controls

- Accountability: AC-1, AC-3

- People: PPL-4

- Stewardship: ST-12

Audit Criterion 2

2. Processes and Controls are in place to ensure that overtime is properly planned, controlled, and in compliance with applicable collective agreements, policies and directives.

2.1 Managers properly plan and budget overtime needs and consider alternative solutions to mitigate overtime use.

2.2 Processes and controls are in place to ensure that overtime is properly authorized, recorded, approved and compensated within the required timeframe.

2.3 Overtime is compensated in compliance with applicable collective agreements, policies and directives.

Related Core Management Controls

- Stewardship: ST-1, ST-2, ST-4, ST-7, ST-10, ST-11, ST-12, ST-13, ST-15, ST-18

- People: PPL-4

- Risk Management: RM-3, RM-7

Audit Criterion 3

3. Reporting and monitoring mechanisms are in place to identify, assess and mitigate administrative and operational risk related to overtime.

3.1 Reporting and monitoring mechanisms are in place to report overtime use and to identify and assess areas of risk.

3.2 Managers have access to reliable and timely information on overtime utilization and regularly review overtime spending.

Related Core Management Controls

- Governance and Strategic Directions: G-6

- Stewardship: ST-4, ST-15, ST-17, ST-20

- People: PPL-4

- Risk Management: RM-2, RM-4

Scope

The audit included all types of overtime for all CBS of the former DFAIT, during fiscal years 2011-2012 and 2012-2013.

Methodology

The audit was conducted in accordance with the International Standards for the Profession of Internal Auditing and the Treasury Board Standards for Internal Audit. The methodology consisted of:

- Data mining and analysis of information in the Integrated Management System (the Departmental Financial System), Salary Forecasting Tool and Human Resources Management System;

- Testing controls and detailed review of overtime claims;

- Document review (policies, procedures, directives, processes and relevant audit and inspection reports); and

- Interviews with management, human resources and finance staff at headquarters, as well as fund centers in the missions.

Appendix B: Management Action Plan

Audit Recommendation 1

The Chief Financial Officer (CFO), in collaboration with the Assistant Deputy Minister, Human Resources, should put in place a process whereby overtime expenditures are reported and monitored, including compensatory time-off, at the Branch level.

Management Action Plan

The CFO Branch will determine the most effective means of reporting and monitoring overtime expenditures and the financial costs for compensatory time off in the FINSTAT reports.

Responsible

Corporate Planning, Finance and Information Technology (Chief Financial Officer)

Expected Completion Date

Branch overtime budgets have been established and the reporting and monitoring process is in place. Reporting to commence on August 1st.

Audit Recommendation 2

The Assistant Deputy Minister, Human Resources Branch, should determine the types of information, reports and trend analysis that would be useful for senior management decision-making and produce them on a regular basis.

Management Action Plan

HCM and SCM to engage in consultations with senior management to determine what type of information is useful in the dashboard for decision making purposes. Establish a process to obtain monthly reports from Human Resources Management System (HRMS) and Salary Forecasting Tool (SFT) that indicate overtime approval and usage by Branch, Bureau and Division as well as group and level.

Responsible

Human Resources (HCM) - SCM

Expected Completion Date

The process to capture data and develop reports is in place. Consultations have taken place with senior management and reporting will commence on August 1st.

Audit Recommendation 3

The Assistant Deputy Minister, Human Resources Branch, in collaboration with the Chief Financial Officer, should improve Departmental practices for approving compensatory time-off. The compensatory time-off liability should be monitored and actively managed, especially for rotational employees.

Management Action Plan

Financial Management Advisors (FMAs) to include monthly reports of overtime (cash) with Business Management Offices (BMOs) so that usage can be a part of FINSTAT review discussions.

Modify current rotational/mobile assignment practices to include the sharing of CTO balances (compensatory) with host managers as part of the decision making process for assignments.

HCM to develop practical guide on the approval and use of overtime for managers.

Responsible

SCM – HCM, HCM

Expected Completion Date

Reporting to commence on August 1st on a monthly basis

Guide to be in effect when all pay accounts have been transferred to Miramichi. This should coincide with the launching of the Pay Modernization initiative in December 2015.

Audit Recommendation 4

The Assistant Deputy Minister, Human Resources Branch, should perform an in-depth review of high overtime users to determine if the overtime was warranted and if corrective measures should be taken.

Management Action Plan

The quarterly reports of high overtime (OT) users with issued by the BMO,s should assist the ADM of Branches to identify high o-t users and take the necessary corrective action if required.

Responsible

ADM of Branches

Expected Completion Date

Reporting to commence on August 1st on a quarterly basis

Audit Recommendation 5

The Assistant Deputy Minister, Human Resources Branch, should ensure that compensation advisors:

- Verify that Section 32 and Section 34 are signed by a delegated authority prior to completing the processing of overtime claims; and,

- Enter data into the system corresponding to the month of the overtime form.

Management Action Plan

The introduction of Extra Duty Pay (EDP) process in the Compensation Web Application (CWA) has automated the following business process. Section 34 list of delegated managers are provided by Corporate Accounting (SMD) to Public Works and Government Services Canada (PWGSC). CWA will electronically ensure that approvers for section 32 and 34 have the appropriate authority. All CTO forms sent to the Center of Expertise (CoE) for processing will have been verified by a trusted source at PWGSC in the Centre of Expertise in Miramichi.

Responsible

SCM - HCM

Expected Completion Date

Completed

Audit Recommendation 6

The Assistant Deputy Minister, Human Resources Branch, should put in place a process to track errors in overtime claims and communicate errors to managers.

Management Action Plan

The introduction of fully automated EDP system tracks errors and communicates these to the delegated manager via the Compensation Web Application.

Responsible

SCM-HCM

Expected Completion Date

Completed

Audit Recommendation 7

The Assistant Deputy Minister, Human Resources Branch, should implement effective records management practices to ensure that documentation is kept to support the reconstruction of overtime transactions.

Management Action Plan

The records management will be done by the Centre of Expertise in Miramichi when the transfer is completed.

Responsible

HCM

Expected Completion Date

Completed by December 1, 2015 when the transfer of all pay accounts is completed.