Economic impact of Canada’s participation in the Comprehensive and Progressive Agreement for Trans-Pacific Partnership

Office of the Chief Economist

Global Affairs Canada

February 16, 2018

1. Introduction

This analysis assesses the potential economic impact of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) for Canada, based on the CPTPP negotiation outcomes concluded in Tokyo, Japan, on January 23, 2018. It highlights the projected economic gains of Canada’s participation in the CPTPP, and compares these to a scenario based on the original Trans-Pacific Partnership (TPP) agreement that included the United States.

The eleven countries that are party to the CPTPPFootnote 1 form one of the largest trading areas in the world, accounting for nearly 13.5% of global GDP.Footnote 2 The CPTPP countries as a group are Canada’s third-largest trading partner. Bilateral trade between Canada and other CPTPP countries, including both goods and services, amounted to $105 billion in 2016, accounting for 8.1% of Canada’s total trade. Two of Canada’s top 5 trading partners, Mexico and Japan, are CPTPP countries. Bilateral foreign direct investment between Canada and CPTPP countries amounted to $122.2 billion in 2016.

Canada already has free trade agreements (FTAs) with three CPTPP countries: Chile, Mexico and Peru. The CPTPP will establish new FTAs with seven additional Asia-Pacific countries: Australia, Brunei Darussalam, Japan, Malaysia, New Zealand, Singapore and Vietnam. In 2016, Canada’s bilateral trade with these seven partners totalled $71.3 billion. This is collectively greater than Canada’s current trade with its third-largest bilateral trading partner, Mexico. The bulk of Canada’s trade with these countries is accounted for by trade with Japan—the world’s third-largest economy.

On January 30, 2017, the United States gave notice of its intent not to ratify the TPP, which prompted the eleven remaining members of the TPP to pursue a new agreement, the CPTPP. The absence of the United States from the TPP significantly changes the dynamics of the economic benefit calculation. Canada is expected to benefit considerably more from the CPTPP relative to the TPP for two main reasons:

- Unlike the TPP, the CPTPP will not result in any erosion of Canada’s preferential access to the U.S. market established under NAFTA. Under the TPP, the United States would have liberalized its trade with other TPP countries, which would have eroded the relative degree of preference accorded to Canada under NAFTA. This could have resulted in a displacement of Canadian exports to the United States. This displacement effect in the U.S. market would have been significant because of the size and importance of the U.S. market for Canada’s trade. While the erosion of Canadian preferences in the U.S. market could have been partially offset by the newly created preferences in other TPP countries, it is unlikely that these gains would have been significant enough to completely offset the losses in the U.S. market.

- In the absence of U.S. competition, Canada will enjoy better market access to other CPTPP countries than U.S. competitors, enabling Canadian exporters to capture larger market shares in these countries.

On the other hand, the absence of the United States from the CPTPP will likely result in smaller potential gains for Canada as compared to the TPP in a few sectors where TPP outcomes would have provided Canada with better access than it currently has under NAFTA. For example, Canada’s expected TPP export gains in sugar and professional services that would have resulted from U.S. commitments in these sectors will not occur under the CPTPP. Also, if the United States had joined the TPP, the resulting increase of U.S. GDP would have translated into greater Canadian exports to the United States. Since the United States is not a party to the CPTPP, this extra boost on Canadian exports will not materialize.

2. Modelling and data framework

The economic impact assessment of the CPTPP is based on simulations with a dynamic computable general equilibrium (CGE) model of global trade. This model follows the structure of the Global Trade Analysis Project (GTAP) model developed and supported by Purdue University.Footnote 3 This model allows users to assess the potential impact of a trade agreement by examining interaction among different sectors as a result of trade liberalization, capturing the economy-wide effect of the agreement on the national economy.

To assess the economic impact of the CPTPP, this analysis compares the economic performance of all CPTPP countries between a baseline scenario (prior to implementation of CPTPP) and a post-liberalization scenario (following full implementation of the CPTPP). The baseline scenario simulates the evolution of the global economy to 2040 in the absence of the CPTPP, based on the projected macroeconomic benchmarks and demographic changes provided by the International Monetary Fund and other international organizations. The baseline scenario incorporates the existing tariff schedules under most-favoured nation (MFN) treatment along with all bilateral FTAs among CPTPP countries, as well as any unilateral tariff liberalization made by countries.

The post-liberalization scenario models the impact of the CPTPP on Canada and the other countries, as well as on non-CPTPP countries. Therefore, the net effect of the CPTPP can be quantified as the difference between the baseline and post-liberalization scenario expressed in terms of changes in GDP, exports and imports. This approach ensures that all other macroeconomic forces affecting the economy, such as macroeconomic fluctuations, employment changes, exchange rate shifts and technological developments, stay the same for both the baseline and post-liberalization scenarios, thus isolating the effects of the CPTPP.

Source: Office of the Chief Economist, Global Affairs Canada

The data used for this modelling exercise is based on the GTAP database version 9, which benchmarks all bilateral trade flows, trade protection and domestic support to 2011. To better represent the current environment, however, tariff data have been updated to reflect current levels of protection in all CPTPP countries. Since 2011, a number of bilateral FTAs have been concluded and implemented among CPTPP countries, such as the Japan-Australia FTA, as well as certain unilateral liberalization initiatives undertaken by some CPTPP members, including Canada.

For the purpose of this study, the global economy is disaggregated into 57 sectors and 19 regions/economies. In addition to the 11 CPTPP countries, the United States, China, Indonesia, South Korea, Taiwan, Thailand and the European Union are separately identified, along with an aggregate for the rest of the world.

Finally, as a note of caution, the modelling results should be considered in the context of both the advantages and limitations of the CGE model being used. The CGE model can reflect only the expansion of trade in products already traded in a given bilateral trading relationship; it cannot predict the creation of trade in new product areas. This limitation is particularly important when the existing trading relationship is fairly narrow. Hence, the assessment can be expected to underestimate the gains from liberalization.

3. Modelling CPTPP liberalization measures

The CPTPP is a trade agreement that covers digital trade, intellectual property rights, state-owned enterprises, non-tariff barriers, regulatory coherence, labour and environment as well as traditional areas such as goods, services, investment and government procurement. Due to the limitations of the model, only non-tariff barriers are taken into account in the model. In addition to tariff reduction and tariff elimination, this study models the effects of services trade and investment liberalization, the establishment of new CPTPP rules of origin in the automotive and textile sectors, and new CPTPP market access under Canada’s supply-management regime. As such, there could be some under- or over-estimation of the size of the gains for Canada and other countries resulting from the CPTPP.

Tariff reductions and eliminations with new FTA countries

The CPTPP tariff commitments comprise more than 100,000 tariff lines and more than 200 pages of tariff-rate quota (TRQs) commitments for agricultural products. These tariff lines and TRQs were incorporated into the GTAP model.

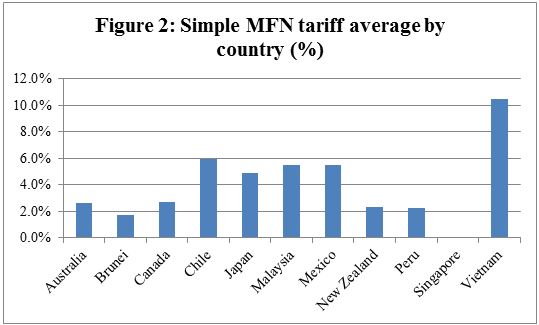

Canada has overall lower levels of tariff protection than most of its CPTPP partner countries (see Figure 2). Hence, holding other conditions constant, liberalization under the CPTPP would be expected to provide a net advantage for Canada. While tariffs are already low on average for most CPTPP countries, there is still considerable room for liberalizing Canada’s trade with the seven countries with which Canada does not already have an FTA and for liberalizing some agricultural products in all CPTPP countries. For instance, Vietnam’s simple average applied tariff is 10.6%, while Japan’s tariffs on fresh/chilled and frozen beef are 38.5%.

Source: World Trade Organization

The liberalization of tariffs results in a loss of government revenue, but benefits consumers and producers. More importantly, liberalization also reduces economic inefficiency (known also as deadweight losses) resulting from market distortion, allowing for greater economic gains. The new preferential market access under the CPTPP is projected to provide Canadian exporters with tariff savings of $428 million per year, with the bulk coming from exports to Japan ($338 million), Australia ($47 million) and Vietnam ($25 million) (see Figure 3). More specifically, Canadian exports to Japan are expected to see tariff savings of $167 million on wheat and barley exports, $51 million on pork products, $21 million on beef and $32 million on wood products.

These figures are estimates of accrued tariff savings for Canadian exporters as a result of the CPTPP. The estimate was calculated by applying CPTPP tariff reductions (on the basis of full implementation of the Agreement) to current Canadian exports to partner countries. This methodology does not take into account the dynamic effect, i.e. the expected increase in exports over time as a result of improved market access, and therefore represents a conservative estimate.

These tariff savings give Canadian exports an extra cost advantage relative to exports from non-CPTPP countries. In addition, tariff elimination under the CPTPP will provide a level playing field with export competitors that are also parties to the CPTPP; some of which have existing FTAs with other CPTPP countries. For example, Australia already has an FTA with Japan that provides preferential access for several agriculture products that compete directly with Canadian exports, which face higher duties.

Source: Global Affairs Canada

For some countries and sectors, CPTPP outcomes could be different from the existing bilateral tariff preferences under existing FTAs. For these sectors, the best bilateral outcomes were used to replace the CPTPP outcomes, as businesses will choose the most advantageous tariff treatment available to them to maximize their commercial interest.

Tariff reductions and eliminations with existing FTA countries

Since Canada already has FTAs with Chile, Mexico and Peru, liberalization of trade in Canada’s existing FTA partners with other CPTPP countries erodes the relative degree of preferences currently accorded to Canada. This would result in a displacement of Canadian exports to existing Chile, Mexico and Peru.

Similarly, liberalization of Canada’s trade with other new FTA partners will displace imports from existing FTA partner countries in Canada. As a result, Canada’s imports from existing FTA partners are expected to decline as a result of the CPTPP.

Liberalization of services trade and investment

The CPTPP takes a broad approach to cross-border trade and investment in services, with services covered unless specifically excluded or listed in a country’s schedule of non-conforming measures (i.e. a negative list approach). Measures include enhanced obligations to secure current and future levels of liberalization in the services sector. Moreover, the CPTPP ensures that commitments by members are locked-in based on their current domestic regime and therefore cannot become more restrictive.

This study focuses on evaluating the locking-in, or binding effect, of services commitments. The extent of service commitments is assessed by comparing the actual CPTPP offers in services against commitments under the WTO General Agreement on Trade in Services (GATS) of 1995, or the best bilateral offers. This comparison provides an assessment on the extent of commitments for each sector by each country in relative terms. To quantify the economy-wide effect of these commitments, we associate these commitments to potential savings in trade and investment costs in services, which reflect the transaction costs involved in international trade and investment in services.

Overall, quantifying the effect of services commitments and market access is much more challenging than is the case for goods. Economic gains from services and investment commitments are modelled as trade cost savings resulting from enhanced regulatory certainty and transparency, which contribute directly to productive efficiency gains. In other words, economic gains in services are modelled as direct productive efficiency gains resulting from replacing previously scheduled obligations with new obligations.

Rules of origin

In a regional trade agreement like the CPTPP, rules of origin ensure that a share of the production of a finished product is performed within the free trade area. Only products that meet the rules of origin are considered as “originating” within the free trade area and, therefore, are eligible for preferential tariff treatment under the free trade agreement. The aim of this policy measure is to provide an incentive to local producers to source parts and labour from within the free trade area, thereby ensuring that both production and the benefits of the preferential tariff treatment accrue primarily to member countries.

In this analysis, two rules of origin issues have explicitly been accounted for:

- Automotive products: Under the NAFTA, assembled vehicles must have at least 62.5% of their content from the region to qualify for NAFTA preferences. Under the CPTPP, 45% of content needs to be from a CPTPP country. Had the United States remained in the TPP, assemblers would have had an incentive to source more parts from non-TPP countries, such as China. More than 90% of Canadian auto production is exported to the United States and benefits from preferential market access under NAFTA. As the United States is not a party to the CPTPP, Canadian automotive products must continue to adhere to NAFTA rules of origin in order to continue benefitting from NAFTA preferences. Thus, the establishment of new rules of origin under the CPTPP is not expected to have a direct effect on the production patterns and sourcing decisions of the Canadian auto industry.

- Based on current sourcing and production patterns, and without the ability to accumulate U.S. materials under the CPTPP, Canadian vehicles cannot meet the CPTPP regional value content requirement (45%). However, except for Australia, Malaysia and Vietnam, Canada has duty-free access to all CPTPP countries, either on a MFN basis or through FTAs already in force. Canada has secured side letters with Australia and Malaysia that establish a rule of origin with a lower regional value content requirement, which will allow Canadian-made vehicles to benefit from preferential treatment.

- Textiles and apparel: The CPTPP includes “yarn forward” rules of origin for textile and apparel products. These rules require that production of specified yarns and fabrics used in textile and apparel production, as well as associated cutting and sewing, must occur in a CPTPP country in order for a product to be eligible for preferential treatment under the Agreement.

- In this analysis, based on the existing production and trade patterns, we assume that Canada would not be able to meet the rule of origin requirement for textiles and wearing apparel products under the CPTPP. Therefore, Canada is not expected to gain increased access to markets in other CPTPP countries despite reductions of textile tariffs in these countries.

4. Quantifying economic gains of the CPTPP

Joining the CPTPP is expected to provide a net advantage to Canada resulting from increased market access and greater regional economic integration with Asia-Pacific countries. The CPTPP is projected to boost Canada’s GDP by $4.2 billion in the longer term (i.e. by 2040). This is significantly higher than the GDP gains of $3.4 billion that were projected under the TPP that included the United States. This increase in GDP is driven by increases in exports of goods and services, and by increases in investment.

Canada’s export gains in the CPTPP would be significantly greater than they would have been under the TPP. Under the CPTPP, total Canadian exports to other CPTPP countries are projected to increase by $2.7 billion or 4.2%, compared to export gains of $1.5 billion under the TPP.

Total exports to all countries increase by around $2.0 billion, as there is some shifting of exports away from non-CPTPP countries toward now more lucrative CPTPP markets. Nonetheless, this is significantly more than the $285-million increase under the TPP. In addition to the increase in exports, investment in Canada increases by $810 million, as a result of both greater foreign direct investment as well as more investment by domestic businesses.

Exports to new FTA partner countries

The central benefits for Canada from the CPTPP are the preferential market access to new FTA partner countries through tariff elimination and reduction. Canadian exports to these new FTA partner countries are expected to expand by $3.2 billion, with the largest gains coming from Japan, Australia, Vietnam and Malaysia. Among these markets, the most noticeable gain for Canada is with Japan. Under the CPTPP, total Canadian exports to Japan are expected to increase by $1.8 billion or 8.6%, compared to $1.3 billion under the TPP; exports of pork and beef products should benefit most from the absence of the United States:

- Canadian pork exports to Japan are projected to increase by $639 million or 36.2% under the CPTPP, vs. $400 million under the TPP. Under the CPTPP, the Japanese safeguard measure for pork imports will be eliminated within 10 years after the entry into force of the Agreement; therefore, the Japanese safeguard measure for pork imports should not affect the potential for Canadian pork exports to Japan.

- Canadian beef exports to Japan are projected to increase by $378 million or 94.5% vs. $228 million under the TPP. The projected increase in Japan’s beef imports under the Agreement from all CPTPP countries are not expected to trigger the beef safeguard measure in Japan because the specified volume is sufficiently large that any increase in exports resulting from the CPTPP should not trigger the safeguard.

Other Canadian exports to Japan projected to increase are wood products, by $226 million (or 15.8%); non-ferrous metals, by $54 million (or 7.1%); and chemical products, by $51 million (or 7.1%).

| TPP countries | CPTPP countries | |||

|---|---|---|---|---|

| Change | % | Change | % | |

| U.S. | -652 | -0.1% | -286 | -0.1% |

| Australia | 664 | 11.2% | 689 | 11.6% |

| Brunei | 1 | 1.2% | 1 | 1.3% |

| Chile | 13 | 0.5% | 19 | 0.8% |

| Japan | 1346 | 6.6% | 1767 | 8.6% |

| Malaysia | 234 | 5.0% | 200 | 4.3% |

| Mexico | -504 | -2.8% | -418 | -2.3% |

| New Zealand | 110 | 10.8% | 123 | 12.1% |

| Peru | 1 | 0.0% | 7 | 0.4% |

| Singapore | 92 | 0.9% | 99 | 0.9% |

| Vietnam | 206 | 12.8% | 271 | 16.8% |

In addition to expanded trade with Japan, Canada is also expected to see an increase in exports to other CPTPP countries. In particular, Canadian exports to Australia would expand by $689 million or 11.6%. Noticeable gains would be in the sectors of machinery and equipment ($166 million) and transportation equipment ($170 million).

Canadian exports to Malaysia are expected to increase by $200 million or 4.3%. Canadian export gains would be concentrated in machinery and equipment ($91 million) and automotive products ($17 million).

Canadian exports to Vietnam are expected to increase by $271 or 16.8%. Leading Canadian exports to Vietnam include food products ($52 million) and chemical products ($33 million), though these export gains all start from very low bases.

Canadian exports to New Zealand would increase by 12.1% or a net increase of $123 million. Machinery and equipment ($39 million) and food products ($14 million) dominate total Canadian export gains to New Zealand.

Imports from new FTA partners under the CPTPP are also projected rise by $6.9 billion. The increase in imports from new FTA countries is led by motor vehicles and chemical products from Japan and labour-intensive products such as textiles, apparel and leather products from Vietnam. This will largely come at the expense of lower Canadian imports from China and other non-CPTPP countries.

Trade with existing CPTPP FTA partners

The export gains for Canada resulting from new access under the CPTPP will be partially offset by a $392-million decline in exports to Canada’s existing FTA partners, namely Chile, Mexico and Peru, largely due to an erosion of NAFTA preferences in Mexico.

Similarly, imports by Canada from the existing FTA members would fall by $447 million, mainly due to a decrease in imports from Mexico resulting from erosion of Mexico’s preferences in Canada.

Trade with the United States

Under the CPTPP, Canadian exports to the United States are not expected to change significantly as the United States is not party to the CPTPP. However, there would be a decline in imports by Canada from the United States, resulting from erosion of U.S.’s NAFTA preferences in the Canadian market. Total Canadian imports from the United States are projected to fall by $3.3 billion, led by a decline in automotive products imports.

Trade by sector

Overall, Canada’s exports to the world would expand in the sectors of beef, pork, vegetable oils, wood products, motor vehicles and parts, machinery and equipment, and services. Increases in imports would be dominated in the sectors of apparels, leather products, chemical products and machinery and equipment.

| Exports | Imports | |||

|---|---|---|---|---|

| Change | % | Change | % | |

| Wheat, cereal grains, other crops | -36.0 | -0.24% | 16.8 | 0.50% |

| Vegetables, fruit, nuts | 27.0 | 0.39% | 17.6 | 0.20% |

| Oil seeds | -65.3 | -0.51% | 4.6 | 0.52% |

| Live animals | -17.9 | -1.07% | 3.6 | 1.67% |

| Other animal products | -1.3 | -0.04% | 12.8 | 1.37% |

| Other agriculture | 0.2 | 0.22% | 1.3 | 0.18% |

| Forestry | -12.2 | -0.38% | 4.4 | 0.63% |

| Fishing | 5.7 | 0.24% | 4.2 | 0.35% |

| Coal | 6.4 | 0.05% | 2.0 | 0.12% |

| Oil and gas | 77.1 | 0.08% | 34.7 | 0.14% |

| Other minerals | -4.7 | -0.01% | -3.2 | -0.03% |

| Beef | 380.5 | 9.49% | 18.5 | 0.83% |

| Pork | 625.1 | 10.07% | 87.2 | 1.84% |

| Vegetable oils and fats | 42.2 | 0.52% | 12.8 | 0.66% |

| Dairy products | 3.5 | 0.43% | 135.1 | 13.08% |

| Sugar | 37.0 | 7.88% | 7.8 | 0.58% |

| Other food products | 24.2 | 0.12% | 56.0 | 0.23% |

| Beverages and tobacco products | 13.5 | 0.47% | 14.7 | 0.16% |

| Textiles | 18.5 | 0.71% | 69.4 | 0.57% |

| Wearing apparel | 19.0 | 1.69% | 294.3 | 2.75% |

| Leather products | 36.9 | 15.47% | 127.8 | 3.06% |

| Wood products | 167.7 | 0.82% | 93.2 | 0.58% |

| Paper products, publishing | -89.0 | -0.21% | 30.9 | 0.18% |

| Petroleum, coal products | 5.9 | 0.03% | 75.4 | 0.23% |

| Chemical, rubber, plastic products | -28.8 | -0.03% | 160.6 | 0.15% |

| Other mineral products | 0.9 | 0.03% | 20.4 | 0.20% |

| Ferrous metals | 15.3 | 0.11% | 23.4 | 0.11% |

| Other metals | -99.2 | -0.13% | -5.4 | -0.01% |

| Metal products | -4.5 | -0.04% | 95.6 | 0.43% |

| Motor vehicles and parts | 255.9 | 0.23% | 84.3 | 0.07% |

| Other transport equipment | 97.5 | 0.29% | 61.0 | 0.29% |

| Electronic equipment | -12.9 | -0.12% | 50.8 | 0.13% |

| Other machinery and equipment | 128.6 | 0.22% | 176.7 | 0.13% |

| Other manufactured goods | 0.7 | 0.04% | 36.0 | 0.26% |

| Services | 338.2 | 0.20% | 288.3 | 0.19% |

| Total | 1,955.7 | 0.21% | 2,113.3 | 0.24% |

Impact on the automotive sector

As noted above, although there is a slight increase in imports of motor vehicles and parts from the world as a result of the CPTPP, this is offset by a small increase in exports. Overall, production in the automotive sector is expected to rise very modestly, by $206 million.

The reason for the modest impacts on automotive imports is twofold. First, as noted above, the lower rules of origin requirements under the CPTPP do not provide an incentive for Canadian assemblers to use more parts from non-CPTPP countries, such as China, because production is geared to NAFTA rules of origin.

Second, while inputs of assembled vehicles from Japan (the only country among new CPTPP partner countries that produces cars) rise modestly, this is largely offset by lower imports from other countries, principally the United States, as well as Mexico and the European Union.

It should be noted that the increase in exports is likely an underestimate, as Canada has secured, as part of the CPTPP, a legally binding and enforceable side agreement with Japan on auto standards and regulatory measures. However, this is not modelled in the analysis.

An independent studyFootnote 4 on the potential impact on the Canadian automotive industry of Canada’s trade agreements with Asian countries such as Japan and South Korea also suggested that the effect of tariff reductions under an FTA with Japan on the Canadian automotive industry would be very limited.

5. Conclusion

The economic analysis conducted by the Office of the Chief Economist at Global Affairs Canada concludes that the CPTPP would generate long-term economic gains for Canada totalling $4.2 billion. The gains are driven by increases in goods and services exports and investment.

The increases in exports are driven primarily by new preferential access for Canadian businesses to the markets in which Canada does not already have an FTA, such as Japan, Vietnam, Malaysia and Australia. The gains for Canada cover a broad range of sectors across the Canadian economy, including some agricultural products such as pork and beef, wood products, machinery and equipment, and transportation equipment. The impacts on the automotive sector are slight, with a small increase in output and exports.

The CPTPP gains are greater than the $3.4 billion gain expected under the TPP, due to improved market access for Canadian business to other CPTPP countries in the absence of U.S. competition. The results are consistent with estimates by the Canada West Foundation, which reports that Canada’s GDP gains would improve to $3.4 billion under the CPTPP, compared to $2.8 billion under the TPP.Footnote 5

- Date Modified: