Archived information

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Internal Audit of Grants and Contributions in Geographic Programs Branch

Final Report

December 2012

Table of Contents

- Acronyms and Initialisms

- Executive Summary

- 1.0 Background

- 2.0 Audit Objective, Scope, Approach, and Criteria

- 3.0 Main Audit Findings and Recommendations

- Appendix A: List of Recommendations and Management Action Plan

- Appendix B: Recipient Profile by Disbursements in GPB

- Appendix C: Sample Project List

- Total GPB Aid Disbursements from Fiscal Year 2010 to 2012

Acronyms and Initialisms

- APP

- Agency Programming Process

- BMI

- Business Modernization Initiative

- CDPF

- Country Development Programming Framework

- CFO

- Chief Financial Officer

- CFOB

- Chief Financial Officer Branch

- CIDA

- Canadian International Development Agency

- CRP

- Corporate Risk Profile

- CRR

- Country Risk Register

- FRET

- Fiduciary Risk Evaluation Tool

- GPB

- Geographic Programs Branch

- IMRT

- Investment Monitoring and Reporting Tool

- IRR

- Investment Risk Register

- MGPB

- Multilateral and Global Programs Branch

- NGO

- Non-Governmental Organization

- PBA

- Program-Based Approach

- PWCB

- Partnerships with Canadians Branch

- RBAM

- Risk-Based Administration Matrix

- SPPB

- Strategic Policy and Performance Branch

- SVP GPB

- Senior Vice-President, Geographic Programs Branch

Executive summary

In accordance with its approved Risk-Based Audit Plan for 2011-2014, the Office of the Chief Audit Executive at the Canadian International Development Agency (CIDA) conducted an internal audit of grants and contributions in the Geographic Programs Branch (GPB). The objective of this audit was to provide reasonable assurance that measures are in place to ensure that the use and management of grant and contribution funding in GPB is compliant with the Treasury Board Policy on Transfer Payments and the related Directive, as well as with other applicable CIDA policies.

In 2006, the Independent Blue Ribbon Panel on Grant and Contribution Programs concluded that fundamental change was needed to make the delivery of grants and contributions more efficient while ensuring greater accountability. In response, the government announced a three-year action plan to reform the administration of grant and contribution programs. As one of the key elements of this plan, a new Policy on Transfer Payments was developed, aimed at increasing efficiencies and reducing the administrative burden on recipients of grants and contributions.

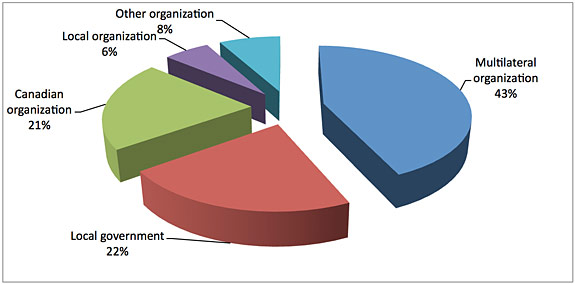

In 2011-2012, GPB's grants and contributions spending was approximately $1.34 billion, about 40 percent of the Agency's total. Of this amount, 43 percent flowed through multilateral organizations at the country and regional levels. Over the past three years, GPB's grants and contributions were made to more than 100 countries and 483 recipients, from which 80 percent of the funding went to 20 countries of focus (Appendix B: Grants and Contributions Recipient Profile).

The audit found that the Agency's risk management framework and related supporting policies have been adopted by GPB and integrated into branch business processes, and risk tools are used as required and aligned with the Corporate Risk Profile.

In most cases, the oversight of risk management is well established and integrated into business and project planning processes.

Although program managers assessed and were well aware of the risks specific to the country, program and the recipients, and the measures used to manage and mitigate those risks, it was not evident how these risk factors were used in making programming decisions and establishing administrative requirements.

The internal coordination between GPB and other programming branches, especially with the Partnerships with Canadians Branch (PWCB), has improved in some country programs; however, this practice is not consistent and formalized due to minimal guidance on the whole-of-Agency approach.

The consultation and engagement with stakeholders, especially with country recipients, took place significantly at both program and investment levels. Nevertheless, a well-thought-out plan would ensure that the consultation and engagement needs for achieving program objectives are fully and consistently met.

Audit Conclusion

In general, GPB has put many key measures in place, using a risk-based approach, to ensure that the use and management of grants and contributions complies with the Policy on Transfer Payments and other applicable policies.

Opportunities for improvement were identified in developing branch or program plan and guidance in areas of consultation and engagement with GPB's applicants and recipients, establishment of service standards, and collaboration with other programming branches.

Statement of Conformance

In my professional judgment as the Chief Audit Executive, this audit was conducted in conformance with the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing and with the Internal Auditing Standards for the Government of Canada, as supported by the results of the quality assurance and improvement program. Sufficient and appropriate audit procedures were conducted, and evidence gathered, to support the accuracy of the findings and conclusion in this report, and to provide an audit level of assurance. The findings and conclusion are based on a comparison of the conditions, as they existed at the time, against pre-established audit criteria that were agreed upon with management and are only applicable to the entity examined and for the scope and time period covered by the audit.

Chief Audit Executive

1.0 Background

The internal audit of grants and contributions in GPB was part of the 2011-2014 Risk-Based Audit Plan recommended by the Audit Committee and approved by the President on March 25, 2011.

Although the Policy on Transfer Payments took effect in October 2008, the Agency was not required to conform to certain provisions until April 1, 2012 upon renewal of CIDA's Terms and Conditions for International Development Assistance. These provisions directly address the Report of the Independent Blue Ribbon Panel on Grant and Contribution Programs. They include the use of a risk-based approach for the management of grants and contributions, the consultation and engagement with stakeholders, and an appropriate harmonization of transfer payment programs within the department.

GPB consists of five regional directorates that provide development assistance in a specific country or region. These programs are typically based on a development plan created by the government of that country. While GPB has disbursed funds to more than 100 countries and 483 recipients over the last three years, 80 percent of the funding went to 20 countries of focus. GPB's partners include recipient governments, multilateral institutions, non-government organizations, other donors, universities, associations and private corporations.

The Agency has recently implemented a number of change initiatives that impact GPB business processes and is planning for further significant changes in the future. As part of the Business Modernization Initiative (BMI) Project, the Agency Programming Process (APP) is designed to achieve a consistent and whole-of-Agency approach to CIDA's programming processes and is expected to be implemented in early 2013. GPB's decentralization plan locates operations, associated roles, experts, authorities, and accountabilities in the field to strengthen aid effectiveness. As well, the Chief Financial Officer Branch (CFOB) has introduced a new Policy on Fiduciary Risk and related tools and processes to enhance the assessment of fiduciary risks. Given the potential impact these and other changes have on the way the Agency and GPB does business, the audit team reviewed and assessed ongoing progress and implications in relation to relevant audit lines of enquiry.

2.0 Audit Objective, Scope, Approach and Criteria

2.1 Objective

To provide reasonable assurance that measures are in place to ensure that the use and management of grant and contribution funding in GPB is compliant with the Policy on Transfer Payments, as well as with other applicable CIDA policies.

2.2 Scope

The audit focused on assessing the Agency's readiness for its compliance with new provisions articulated in the Policy on Transfer Payments and the related Directive and Guidelines.

Based on consultations with GPB, past audits and evaluation coverage, materiality of aid disbursements, and the Agency's decentralization plan, five country programs were selected for reviewFootnote 1. In addition, a sample of 19 projects from the five country programs was selected for audit testing. This selection was based on materiality and was designed to provide representative coverage of delivery channels, aid modalities, types of recipients, and fiduciary risk assessment tools. The sample projects were selected from those started after October 2008 and operational in 2011-2012.

The audit scope excluded the following types of projects:

- Administrative arrangements with other federal government departments, as an audit was performed in 2011-2012;

- Directive programming projects resulting in a contract, to which the Policy on Transfer Payments was not applicable; and

- Program Support Unit projects, as these were least relevant to the three audit criteria.

2.3 Approach and Methodology

The internal audit of grants and contributions in GPB was conducted in accordance with Treasury Board policy, directives and standards on internal audit, and conforms to the International Standards for the Professional Practice of Internal Auditing of the Institute of Internal Auditors. The evidence gathered was sufficient to provide senior management with proof of the conclusions derived from the internal audit.

In order to conclude on the criteria, and based on identified and assessed key risks and internal controls associated with the related business processes, the audit methodology included, but was not limited to, the following:

- Review of the Treasury Board's Policy on Transfer Payment, Directive and Guidelines, and related CIDA policies, guidelines and instructions;

- Review and analysis of five country programs and 19 project files and related documentation;

- Interviews with various levels of project and program management from GPB, CFOB, BMI and the Strategic Policy and Performance Branch (SPPB);

- A survey of Canadian NGOs which implement the Agency's grants and contributions programs;

- Analysis of financial and non-financial information; and

- Validation of key audit findings.

2.4 Audit Criteria

Audit criteria were developed in relation to the following three lines of enquiry based on results of the risk and internal control assessment and the Treasury Board Core Management Controls. Audit criteria were also shared and discussed with GPB, CFOB and SPPB. The audit was to determine:

- if the design, delivery, monitoring and reporting of the grant and contribution programs in GPB was risk-based;

- if applicants and recipients of grants and contributions program funding in GPB were consulted, engaged and served with reasonable and practical service standards; and

- if GPB coordinated its efforts with other implicated branches in program design, delivery, monitoring and reporting.

3.0 Main Audit Findings and Recommendations

3.1 Risk-Based Management Approach

Risk Management Framework and Tools

The Policy on Transfer Payments requires that transfer payments "be managed in a manner that is sensitive to risks, that strikes an appropriate balance between control and flexibility, and that establishes the right combination of good management practices, streamlined administration and clear requirements for performance."

The Agency's risk management framework is outlined in "Managing Risk at CIDA: 2010 to 2020" and is further supported by a number of key policy documents including the new Policy on Fiduciary Risk and the Policy on Program-Based Approaches. Furthermore, Integrated Risk Management is one of the three components of CIDA's Risk-Based Management Policy and promotes a continuous, proactive, and systematic process to understand, communicate, and manage risk in a cohesive and consistent manner. As a corporate requirement, this framework and related supporting policies have been adopted by GPB and integrated into branch business processes. The audit also found that GPB is adhering to the risk management approach and processes described in the Agency's risk management framework.

The Agency has developed many risk management tools and guides readily available to employees. GPB uses these tools for developing branch, country, and investment risk registers. One of the most recent risk tools for assessing fiduciary risks is the Fiduciary Risk Evaluation Tool (FRET) implemented in 2011-2012. It was designed to help program staff conduct a consistent and systematic fiduciary risk assessment of projects and to collaboratively develop risk profiles of funding recipients. To facilitate an appropriate use of FRET assessment results, the Risk-Based Administration Matrix (RBAM) was implemented in July 2012. It is designed to link the risk rating of the FRET assessment with the administrative requirements in the funding agreement and for financial instrument selection.

Overall, the audit found that GPB had adopted the risk tools and used them as required, and that most risk tools were well aligned and integrated. For example, the Agency's Corporate Risk Profile (CRP), GPB Risk Profile, Country Risk Register (CRR), Investment Risk Register (IRR) and the Risk Register in the Investment Monitoring and Reporting Tool (IMRT) have the same structure and format. As well, most tools use a similar rating scale, which helps to ensure consistency of assessments across the Agency, branches and programs.

The audit also found that in general, there is sufficient training and guidance documentation available to ensure that GPB staff are well informed on the purpose and use of tools. While FRET and RBAM training is not mandatory, the training and communication plans for the introduction of the FRET is comprehensive and readily available. Most program staff stated that they found the FRET training useful.

Application of Risk-Based Approach

The Directive on Transfer Payments requires that departmental managers with responsibility for the design and redesign of a transfer payment program assess the key elements and document evidence of their consideration including:

- the risks specific to the transfer payment program, the potential risks associated with applicants and recipients, and the measures that will be used to manage these risks;

- the rationale used in the selection of the appropriate transfer payment instruments; and

- the administrative requirements on applicants and recipients, and a strategy to ensure these are no more than is needed to meet the department's control, transparency and accountability requirements.

Risk Identification and Assessment

The identification and assessment of risk in GPB occurs at various levels and time frames, and is an ongoing process that influences branch, country, and project level decisions. On a semi-annual basis, the GPB Risk Profile is reviewed and updated, using inputs from both the Agency CRP and country level programming. CRRs are created as part of the development of Country Strategy and Country Development Programming Framework (CDPF) documents and considers both the branch risks and country-specific risks. At the project level, IRRs are prepared for each GPB project and reflect the country level risks that may impact project results, as well as risks specific to the project, the recipient, and the beneficiaries. As a part of this process, a FRET assessment is prepared to consider fiduciary risks. The results of the FRET assessment are incorporated into the IRR. Ongoing monitoring and evaluation of projects and country environmental assessments provide feedback for updates to the risk registers and any required changes to risk mitigation strategies.

The audit found that in most cases, the risks specific to the country, program and the recipients, and the measures used to manage and mitigate those risks, had been assessed and documented.

At the country level, CRRs had been prepared in all cases and registers were found to be aligned with the GPB Risk Profile. Additionally, risk factors and lessons learned had been identified and highlighted in all CDPF and/or Country Strategy documents examined. In four out of five country programs, the highest rated risks in the CRRs had been carried forward to the CDPF or Country Strategy documents. Country Directors and Managers stated that risk factors were important considerations in the design of the overall programming strategy within the country.

At the investment level, risk assessment and risk management is central to the planning phase of a project. All 19 projects reviewed had an IRR identifying risks and mitigation strategies. Eighteen of those IRRs are aligned with the CRRs and their respective IMRTs. Furthermore, in 18 of 19 projects reviewed, planning phase documentation included an assessment of the country environment, previous experience and risks related to the implementing organizations. In reviewing the sample projects with a FRET assessment completed, it was found that there are five projects with FRET assessment performed prior to approval. In four cases, the results of the FRET assessment were carried forward to the IRR.

Selection of Programming Modalities, Funding Instruments and Project Implementing Organizations

The selection of the appropriate programming modality, implementing organization and funding instrument is key to ensuring that desired development results are maximized.

The selection of the appropriate funding instrument is influenced by both policy and programming decisions, taking place at the planning and initiation stages.

From a policy perspective, CIDA's Terms and Conditions for International Development Assistance provide guidance to Agency staff in the selection of the appropriate funding instrument. In some cases, based on the Terms and Conditions, the instrument is predetermined by the type of recipient. For example, the Terms and Conditions state that grants are normally selected when the recipient is a multilateral organization.

From a programming perspective, the selection of the programming modality and delivery channel (bilateral or multilateral) is a strategic decision that requires the assessment of various factors including the country environment, the capacity and public financial management system of the recipient government, other bilateral donor involvement in the country, the capacity of local partners and other related considerations. CIDA's Policy on Program-Based Approaches (PBA) outlines the various considerations and assessments required before entering into a PBA arrangement. The decision to use a specific aid delivery channel and a PBA has a direct impact on the funding instruments available for implementation of programs and projects within the country.

The selection of the appropriate implementing organization in GPB is largely determined by factors such as nature and size of the project, work experience with the Agency, expertise available in certain development sectors, its track record and other related considerations. The selection of the implementing organization further influences the decision as to which funding instrument is most appropriate.

Interviews and sample project file reviews provided evidence that program managers considered project and recipient risks when making programming decisions. However, the audit found that there is no consistent documented rationale and/or analysis to support such decisions. The examination of Country Strategies and CDPFs revealed that a comprehensive rationale and/or a thorough analysis to support the selection of aid modalities and funding instruments was not present. These documents only describe, at a high level, institutional and civil society capacity, along with lessons learned, alignment with the Paris Declaration on Aid Effectiveness, and broad statements on aid modalities and funding instruments to be used, without an aggregated review.

A possible resolution to address this issue is currently being developed. Under the BMI, a Management Statement of Intent document is planned as part of the introduction of the APP in 2013. This document will require program staff to document an analysis and justification for the selection of the aid modality, business delivery model and programming class. The introduction of the RBAM for new projects in 2012-2013 will also formally link the project and recipient risks and value of the funding to the selection of the funding instrument.

Establishment of Administrative Requirements

Administrative requirements in funding agreements such as reporting, monitoring, cash management and audit are intended to ensure that the obligations and objectives set out in the funding agreement are met, and support the Agency's accountability and performance measurement requirements.

To ensure cost-effective oversight and internal control, the new Policy on Transfer Payments requires that monitoring and reporting activities should be proportionate to the level of risk. In other words, the administrative requirements in funding agreements should be established in a manner that balances the accountability and control requirements with the level of risk specific to the transfer payment program, the value of the funding, and the known capacity of the recipients.

The interviews conducted and documentation reviewed indicated that the project officers were aware of project and recipient risks but did not use risk information in the establishment of administrative requirements. The audit reviewed the reporting requirements for the 19 sample projects and found there was no correlation between the project risk rating and the reporting requirements. For example, 5 of 11 projects rated low risk required quarterly financial reports, which is a requirement more likely to be aligned with high risk projects.

As a result, there is the risk that administrative requirements may not be selected on a consistent basis or the level of administrative burden may be more than would be needed to meet the Agency's control, transparency and accountability requirements.

Management advises that with the implementation of RBAM, a more consistent management practice will be promoted and encouraged in establishing administrative requirements based on risk.

Financial compliance audits represent one of the administrative requirements, along with Financial Capacity Building Activities. Carried out by the Financial Compliance Unit within CFOB, these activities focus on the financial aspect of a recipient audit and play a vital role in providing CIDA management with assurance that payments comply with the terms and conditions of contribution agreements and contracts, in accordance with the Policy on Transfer Payments and section 34 of the Financial Administration Act.

Through interviews with Country Program Managers, it was found that the standard audit scope that focused solely on financial compliance did not meet the greater programming monitoring needs. The Directive on Transfer Payments and its guideline specifies that responsible departmental managers should determine when recipient audits are necessary to complement other departmental monitoring activities and to develop and execute a risk-based plan for these recipient audits accordingly. Thus, the scope, standards to be applied, and the nature of the report to be provided should be flexible in meeting overall compliance monitoring needs, as determined by program management. Consequently, the mechanics of recipient audits should be flexible to ensure diverse recipient monitoring needs are met in a cost-effective way, including an audit with reasonable assurance, a review with moderate assurance or specified auditing procedures with no assurance.

As the compliance audit, along with other administrative requirements, will be built upon FRET assessments, the Recipient Compliance Audit Plan will be integrated with other existing financial management tools.

Recommendation 1:

The CFO, in collaboration with the Senior Vice-President, Geographic Programs Branch (SVP GPB), should develop an appropriate process to ensure that risk-based audit scope of the recipient audit is broadened to include non-financial aspects, as needed, in order to complement other program monitoring activities. This new recipient audit approach should be reflected in the Agency's new Directive on Recipient Audit.

GPB Review and Oversight of Risk Management

Senior management review and oversight of risk management is important to ensure that risk assessments are well aligned and performed on a consistent and regular basis and appropriate risk responses have been identified and implemented.

In most cases, the oversight of risk management is well established and integrated into business and project planning processes in GPB. The GPB risk profile is established twice a year and reviewed by GPB senior management and SPPB. Country-level risk profiles are developed and integrated into the CDPF and the Country Strategy documents, which are reviewed and approved by senior management. The IRR and the FRET are developed by program staff and are reviewed and approved by GPB management as part of the project approval process. This is supported by sample testing showing all IRR and FRET assessments had received appropriate management approval. Additionally, CFOB performs a quality assurance review of FRET assessments to ensure consistency and alignment. Furthermore, it has been found that IMRTs prepared for projects totalling 70 percent of GPB's budget are also reviewed and approved by GPB senior management.

3.2 Recipient Consultation and Engagement, and Service Standards

The Policy on Transfer Payments requires that departmental managers are responsible for "engaging applicants and recipients, when appropriate, to achieve the objective and expected results of this policy through innovative, cost-effective, citizen- and recipient-focused transfer payment programs that are accessible, understandable and useable."

The Directive of the Policy on Transfer Payments states that departmental managers are responsible for "ensuring that potential recipients have ready access to information about transfer payment programs and that a description of each program is made public, including application and eligibility requirements and criteria against with which applications will be assessed." The Directive also requires that "departmental managers document a plan for the engagement of potential recipients and other interested parties, where deemed appropriate.''

Consultation and Engagement with Applicants and Recipients

Consistent with the Government of Canada's Open Government initiative and with Canada signing on to the Open Government Partnership, the Agency has become a member of the International Aid Transparency Initiative and has taken important steps to give Canadians improved access to open data and information. It has also committed to work with its partners in ways that do not impose an unwarranted reporting regime or duplicate existing reporting structures.

Consultations are an integral part of CIDA's operations. To comply with the Official Development Assistance Accountability Act, CIDA developed a Directive on Consultations to guide the Agency's consultative activities and facilitate subsequent reporting. It specifies the purpose and requirements for consultation, and outlines the roles and responsibilities of Agency staff in this regard.

Consultations in CIDA vary in formality and purposes and involve a broad range of stakeholders. CIDA's consultations can be categorized under three central classifications. Policy-oriented consultations take place when the Agency engages with outside parties to reflect on or to influence specific policy issues. In contrast, dialogue with partners and stakeholders are bilateral consultations aimed at developing and maintaining relationships with recipient government officials. Finally, consultations on programming occur when the Agency engages partners and stakeholders for the purposes of program/project planning and management.

The audit identified two important groups of applicants and recipients funded by GPB. They are host country recipients and Canadian implementing organizations.

Engaging Host Country Recipients

Engaging the host country recipient is important to ensure that GPB's aid projects align with the Paris Declaration on Aid Effectiveness and, more specifically, with the needs of the country, which is integral to country programming.

The audit found that a significant amount of dialogue, policy and program-oriented consultation occurs with recipient countries to ensure that CIDA programming addresses local needs.

At the country level, a number of guidelines and tools provide guidance to GPB staff in determining when and how to consult with host countries, more specifically, in developing the Country Strategy and CDPF. The review of sample country planning documents demonstrates that the consultation and engagement with recipient countries was discussed in these documents. For example, the Honduran CDPF states: "CIDA's strategic plan for engagement in Honduras was developed in alignment with the Honduras Poverty Reduction Strategy and was based on analysis of Honduras' poverty indicators and CIDA's results to date." Additionally, the Ukraine CDPF states: "Ukraine Program held consultations in Ukraine in August 2009 and in Canada in November 2009.

Interviews with Country Managers and Directors indicate that consultations with host countries occur on a regular and ongoing basis through a variety of different forums including official meetings, working and advisory groups, and bilateral and multi-lateral meetings; however, none of the countries in the sample had a documented consultation strategy or plan for the country. The Vietnam program is working to develop a Policy Engagement Strategy which will document and guide consultations on the ground. This is expected to be completed in the fall of 2012.

At the investment level, the audit found that, where applicable, all project concept papers included a plan to consult recipients and that 16 of 19 projects reviewed have documented evidence of consultations in their respective project files. Additionally, all Project Implementation Plans submitted by implementing organizations included a recipient engagement plan that fulfilled the requirements of the funding agreement. Overall, this showed that at the project level, program-oriented consultations are well planned and that required consultations are occurring.

In terms of feedback to recipients, there was evidence in only 11 of 19 project files that CIDA had responded to recipient input. PBA's represent the greatest proportion of this figure as out of the seven PBA projects in the sample, six projects showed evidence of responding to recipient input.

The Agency prepares a tracking report for all stakeholder-related consultation events undertaken by staff at the level of Director General or above. This report records the objective and location of the events, name and number of participants and the event's outcome. Through our review, a complete report for 2010-2011 and an unfinished report for 2011-2012 were found. This tracking report, created in accordance with the Directive on Consultation requirements, records the purpose and the type of consultation by GPB, the number of participants, the name of the CIDA official responsible for the event, the sectors of society/government, the partners or stakeholders' representatives and the follow-up required.

The decentralization of CIDA and GPB staff is a key tenet of the BMI. Under decentralization, GPB will strengthen field presence by moving program staff and operations from headquarters to countries of focus. The addition of field staff and expertise in recipient countries is intended to improve consultation and engagement by strengthening GPB's relationships with local partners and stakeholders.

Engaging Canadian Implementing Organizations

Although GPB is not the focal point for CIDA's relations with Canadian organizations, within the context of a country strategy, GPB supports development projects and programs that are designed and implemented by Canadian organizations. Based on GPB's grants and contributions disbursements in 2011-2012, nearly 20 percent of its bilateral programs were implemented by Canadian organizations.

The audit found that the country program planning guidelines outline the analysis required to develop the Country Strategy and CDPF and include guidance on consultations. For example, the CDPF Guidelines state that analysis should be informed "by consultations with relevant stakeholders including Canadian Civil Society Organizations".

At the country level, the audit found that CDPF and Country Strategy documents sometimes referred to the nature and type of engagement with Canadian implementing organizations. For example, the Honduras CDPF states that the CDPF "was also informed by consultations with donors, civil society both in Honduras and in Canada" and the Ukraine CDPF states that consultations were held with Canadian civil society "to provide Canadian stakeholders an opportunity to contribute to the development of the CDPF." However, the remaining CDPFs did not make reference to these consultations.

Interviews with GPB staff indicate that many consultations with Canadian NGOs had taken place during the period under review. For example, the Vietnam program and the Office of the Regional Director General of the Americas undertook formal consultations with Canadian stakeholders in 2010 and 2011 respectively, with additional evidence of consultations between other country programs and Canadian NGOs also found.

The audit found that consultations with Canadian implementing organizations occurred on an ad hoc basis and there were no documented plans at the branch or country level to guide the consultations.

Furthermore, a survey of Canadian NGOs performed by the audit team shows that NGOs acknowledged that there had been ongoing communication between the Agency and partner organizations, mostly at the individual desk officer level. Nevertheless, NGOs expected more frequent, structured and clearer communication. The survey also revealed that Country program strategies and the Agency's pipeline were the preferred communication tools.

As the Country Strategy and CDPF are for internal purposes only, the "Country Strategy Summary" and "Annual Country Reports" were developed to inform the public on CIDA's current strategic focus, expected and achieved results/outputs/targets and risks for each of the focus countries/regions. Our audit found all five country programs have a "Country Strategy Summary" posted on CIDA's website providing an overview, the thematic priorities, progress on aid effectiveness and achievements.

Recommendation 2:

The SVP GPB should review and determine the needs to consult and engage its stakeholders and develop plans at the branch and country level based on the results of the review.

Business Processes and Service Standards

The Policy on Transfer Payments states that Deputy Heads are responsible for "establishing reasonable and practical departmental service standards for transfer payment programs." Service standards can help grants and contributions program applicants and recipients build their expectations of what and how services could be provided in a transparent and consistent manner. However, the establishment of service standards requires streamlined, standardized and efficient business processes for grants and contributions administration and management.

Although the Honduras and Vietnam programs established internal service standards and protocols to respond to unsolicited proposal, there were no service standards noted for targeted projects and proposals in the reviewed sample country programs. For example, the Honduras program developed a protocol to process unsolicited proposals at headquarters. The protocol outlines who is responsible for dealing with the proposal and how to process it. It provides an overview of the type of required assessment and estimated timelines for response. With respect to the Vietnam program, standard operating procedures for processing unsolicited proposals were identified.

In our survey of Canadian NGOs, respondents indicated that while GPB desk officers responded to 60 percent of their requests within one week, response time exceeded one month in 24 percent of requests. As well, only 34 percent received an estimated response timeline, and 47 percent of those organizations found the estimated timeline was respected.

The Agency Action Plan—Grants and Contributions Reform, developed in May 2011, indicates that service standards are being considered, but the plan has not been updated since that time.

The potential automation of the new tools and Agency-wide expansion of platforms may significantly reduce the administrative burden on CIDA staff and applicants, as information will not need to be provided or reviewed repeatedly. Under the new transparent approach, partners and other stakeholders are intended to have a clear sense of the Agency's requirements, standards and evaluation processes, making it easier to work with CIDA.

Recommendation 3:

With the introduction of the new and streamlined Agency Programming Process, the SVP GPB should establish reasonable and practical service standards for business processes as well as appropriate measures for monitoring their implementation.

3.3 Internal Coordination

The Policy on Transfer Payments states that Deputy Heads are responsible for "ensuring, when appropriate, the harmonization of transfer payment programs within the department." To this end, when two or more transfer payment programs contribute to similar objectives or serve the same recipients, they should be aligned and integrated through internal coordination.

In the five countries selected for the audit, PWCB and Multilateral and Global Programs Branch (MGPB) branches accounted for 17.61 percent to 33.25 percent respectively of total disbursements over the last three years. In addition, program delivery through multilateral organizations represents as much as 80 percent of the total country investment.

Internal coordination, therefore, becomes important from two perspectives. First, harmonization of programming at the planning and initiation stages is required to identify the extent to which possible program links and synergies can be made across branches. Secondly, under the current organizational structure, only GPB has staff in the field on a permanent basis to monitor the country environment and progress of projects whether funded by GPB or the other CIDA programming branches. Consequently, appropriate internal coordination, taken into consideration of different operating modalities and scope of complementary programming across branches, is important to help maximize both programming harmonization and aid delivery efficiency across the Agency.

Agency and GPB guidance on the implementation of the whole-of-Agency approach is minimal. The CDPF guidelines on the approach includes the requirement to "provide an analysis of CIDA's corporate support through MGPB, PWCB, and any relevant regional programming in the partner country and identify the extent to which possible links and synergies between these and bilateral programming can be made." GPB's "How to Guide: Country Program Planning" focuses largely on consultation with external partners and key players whereas the guidance on internal consultation with other programming channels is extremely limited.

The audit found that in all countries sampled, the CDPF includes a whole-of-Agency analysis section. Where relevant, the analysis identifies, at a high level, the other branches and implementing organizations and institutions funded by the respective branches, the level of funding, the nature of the projects funded and the links to CIDA's aid objectives and focus in the country. Greater consideration on the whole-of-Agency approach was taken by the Mozambique and Honduras programs in their respective annual work plans.

The audit reviewed Terms of Reference and Records of Discussion for GPB senior management committees over the past year. CIDA's Program Committee was found to have a mandate that "strengthens whole-of-Agency coherence, alignment and consistency in program planning and delivery." With the exceptions of a whole-of- Agency approach put forward by the Program Committee for the Haiti country program and for the "Country Strategies Way Forward" where the needs were identified in putting a formal consultation process with MGPB and PWCB, the review found that there was insufficient information to demonstrate that internal coordination was on the agenda and discussed on a regular basis.

Interviews with country program managers indicated that the process of seeking input from PWCB has improved recently. For example, some country programs meet with PWCB twice a year to coordinate programming. PWCB often solicits comments from GPB country program staff for programming initiatives and appoints a country-specific contact point in the branch. However, interviews also indicate that there is no consistent approach to internal coordination for program planning or project monitoring and roles and responsibilities between program branches had not been documented.

The project files reviewed as part of this audit demonstrate a lack of documented coordination between GPB and other branches, with the exception of the Ethiopia program, which showed evidence of coordination with MGPB for all projects requiring such coordination.

To maximize the level of harmonization and alignment of the Agency's development efforts in the country, BMI recently introduced a Mandate Letter for a Head of Aid. Signed by the President, the letter clearly defines the roles and responsibilities for the Head of Aid who is mandated to assume various roles and responsibilities as the Agency's senior representative of all Agency programming channels for development cooperation in mission. Among other things, these roles and responsibilities are in the areas of official and representational duties, policy and program management, bilateral programming, reporting, communication and consultation, programming support and human resources management. The plan is to thus implement the Mandate Letter in all CIDA decentralized countries.

Recommendation 4:

To support the implementation of the Mandate Letter, the SVP GPB should further develop guidance for planning and monitoring its grants and contributions programs in coordination with other program branches.

Appendix A: List of Recommendations and Management Action Plan

| Recommendation | Responsibility | Proposed Management Measures | Target Date |

|---|---|---|---|

| 1. CFO, in collaboration with SVP GPB, should develop an appropriate process to ensure that risk-based audit scope of the recipient audit is broadened to include non-financial aspects as needed, in order to complement other program monitoring activities. This new recipient audit approach should be reflected in the Agency's new Directive on Recipient Audit. | CFO SVP GPB | CFOB will take a phased approach to broaden the audit scope of the recipient audits. Various pilots will be conducted. Desk and management audit pilots will be completed by the end of the 2013-14 fiscal year. CFOB will also subsequently develop associated procedures and guidelines. | March 31, 2014 |

| 2. The SVP GPB should review and determine the needs to consult and engage its stakeholders and develop plans at the branch and country level based on the results of the review | SVP GPB | GPB is currently working on a new country program analysis and planning framework for GPB programs, that will include guidance on engaging with stakeholders. | Dec. 31, 2013 |

| 3. With the introduction of the new and streamlined Agency Programming Process, the SVP GPB should establish reasonable and practical service standards for business processes as well as appropriate measures for monitoring their implementation. | SVP GPB | GPB transitioned to the one Agency Programming Process (APP) on January 29, 2013. GPB will monitor APP implementation through periodic consultations with GPB APP users and will develop a plan to establish Branch-specific service standards as required. | March 31, 2014 |

| 4. To support the implementation of the Mandate Letter, the SVP GPB should further develop guidance for planning and monitoring its grants and contributions programs in coordination with other program branches. | SVP GPB | GPB will provide additional guidance on internal coordination of programming with other branches through the GPB's Country Program Analysis and Planning Framework. Further guidance for increased or more standard coordination with other program branches is also being developed with GPB's active involvement in the Agency's APP and Decentralization initiatives. | Dec. 31, 2013 |

Appendix B: Recipient Profile by Disbursements in GPB ($ thousands)

| Recipient Type | # of Recipients | Aid Disbursements | ||||

|---|---|---|---|---|---|---|

| 2009-10 | 2010-11 | 2011-12 | Total | |||

| Amount | % | |||||

| Multilateral organizations | 69 | 585,940 | 742,717 | 603,278 | 1,931,935 | 43% |

| Local governments | 44 | 332,033 | 340,414 | 302,004 | 974,451 | 22% |

| Canadian organizations | 177 | 314,134 | 346,912 | 271,134 | 932,180 | 21% |

| Local organizations | 99 | 100,998 | 89,869 | 75,902 | 266,769 | 6% |

| Other organizations* | 94 | 141,430 | 126,516 | 89,429 | 357,375 | 8% |

| Total | 483 | 1,474,535 | 1,646,428 | 1,341,747 | 4,462,710 | 100% |

Total GPB Aid Disbursements from Fiscal Year 2010 to 2012

Chart description:

Multilateral organization - 43 percent

Local government - 22 percent

Canadian organization - 21 percent

Local organization - 6 percent

Other organization - 8 percent

*Other organizations include other government departments, field offices, embassies and uncoded vendors

Appendix C: Sample Project List ($ thousands)

| No. | Project Name | Country | Start Date | Total Budget | FY 2012 Disbursements |

|---|---|---|---|---|---|

| 1 | LAND - Livelihoods, Ag & National Dev't | Ethiopia | March 1, 2012 | 19,750 | 1,500 |

| 2 | LIVES Livestock & Irrigation Value Chain | Ethiopia | March 1, 2012 | 19,858 | 518 |

| 3 | Improved Food Security through Nutrition | Ethiopia | February 1, 2011 | 50,000 | 9,675 |

| 4 | Benishangul-Gumuz Food Security | Ethiopia | January 7, 2010 | 20,000 | 4,426 |

| 5 | Nutritious Maize for Ethiopia | Ethiopia | March 12, 2012 | 11,557 | 507 |

| 6 | Promoting Food Security (PROSADE) | Honduras | March 1, 2010 | 13,000 | 1,589 |

| 7 | Prevention and Control of Chagas and Lei | Honduras | April 29, 2011 | 18,800 | 1,500 |

| 8 | FHIA / Promoting High-Value Cacao Agroforestry Systems | Honduras | April 13, 2010 | 7,000 | 949 |

| 9 | Supp WFP Honduras Country Prog 2012-2016 | Honduras | February 28, 2012 | 20,000 | 10,000 |

| 10 | Enhancing Food Security and Increasing I | Mozambique | June 29, 2010 | 13,200 | 2,140 |

| 11 | Common Fund for Education (FASE) | Mozambique | August 25, 2009 | 123,000 | 34,500 |

| 12 | General Budget Support | Mozambique | March 22, 2010 | 67,389 | 15,000 |

| 13 | Health Service Delivery Program | Mozambique | March 18, 2010 | 17,500 | 5,000 |

| 14 | Municipal Local Economic Development | Ukraine | January 15, 2010 | 14,147 | 2,668 |

| 15 | Judicial Educ for Econ Growth in Ukraine | Ukraine | March 30, 2012 | 6,622 | 300 |

| 16 | EBED / Evidence Based Economic Development Plan | Ukraine | February 25, 2010 | 10,013 | 1,955 |

| 17 | Ha Tinh Agricultural Development | Vietnam | March 18, 2011 | 10,000 | 1,006 |

| 18 | SocTrang (SME)Dev. | Vietnam | March 18, 2011 | 10,000 | 1,507 |

| 19 | Poverty Reduction Support Credit / PRSC 9-10 | Vietnam | March 22, 2011 | 6,000 | 3,000 |

| Total | 457,836 | 97,741 |